[upbeat music]

Wesley Phoa, Solutions portfolio manager at Capital Group

One key aspect of private credit is that it isn’t as liquid as more traditional public fixed income. Even if those private loans are accessed through a semi-liquid interval fund, investors need to be comfortable with the fact that they are restricted in their ability to immediately withdraw funds. That’s because interval funds are vehicles that typically contain less liquid assets which makes them better suited for investors with a long-term investment horizon. This is consistent with Capital Group’s core belief in long-term investing.

In this video, we’ll take a look at how interval funds are structured, and we’ll give you pointers on how to talk to your clients about them. Let’s get started.

[upbeat music]

First and foremost, you’ll need to gauge your clients’ liquidity needs.

You likely have a sense of this already, as understanding those needs is a central part of comprehensive financial planning. Since needs change over time, it’s good practice to periodically check in with clients to understand where they currently stand.

You’ll want to know when they’ll need funds, how much they’ll spend, and at what rate, and their overall capacity for risk. Let’s dig a little deeper on that last point. How big a liquidity risk does any given investment within a portfolio represent?

As you can see on the chart, we believe there are three key liquidity considerations: the size of an asset’s position, how quickly it might need to be sold and the markdown incurred in the event of a sale. The question isn’t whether an asset can be liquidated, because in most situations it can, albeit at a cost.

The primary challenge is how to liquidate assets while minimizing costs and maintaining an acceptable level of portfolio risk. We believe it’s all about finding the right balance between these trade-offs.

Liquidity plays a critical role in portfolio construction by offering flexibility and risk management. The more liquid an asset, the more easily it can be sold if needed, or converted into other assets.

It's important to have a framework that aligns an investment’s liquidity to your client’s broader portfolio risk and return objective and their investment horizon.

In this waterfall chart, you will see a liquidity spectrum at an asset and vehicle level. Cash and cash equivalents are most liquid, with publicly traded assets next. We believe active management should be done with a long-term perspective; therefore, it’s our view that investors should liquidate passive before active. If you liquidate active first, you can lose the benefit of the investment strategies and active management. The remaining categories are semi-liquid, which include interval funds, and finally highly illiquid assets.

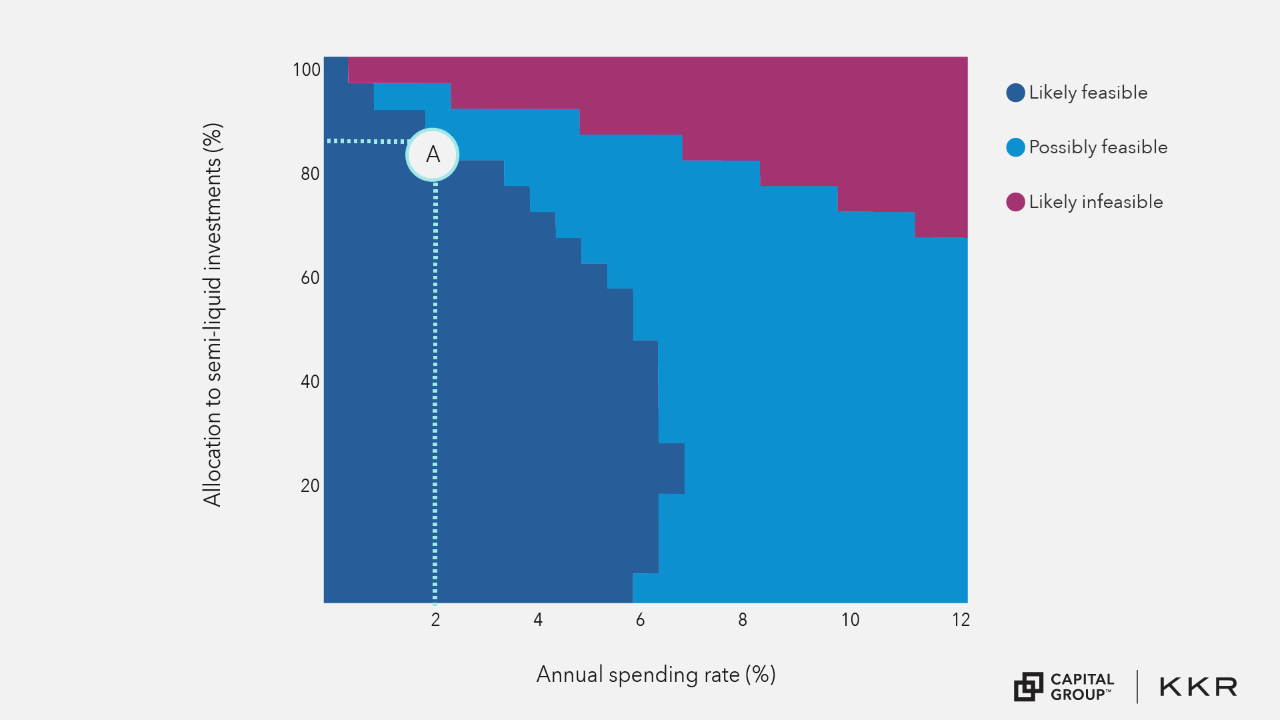

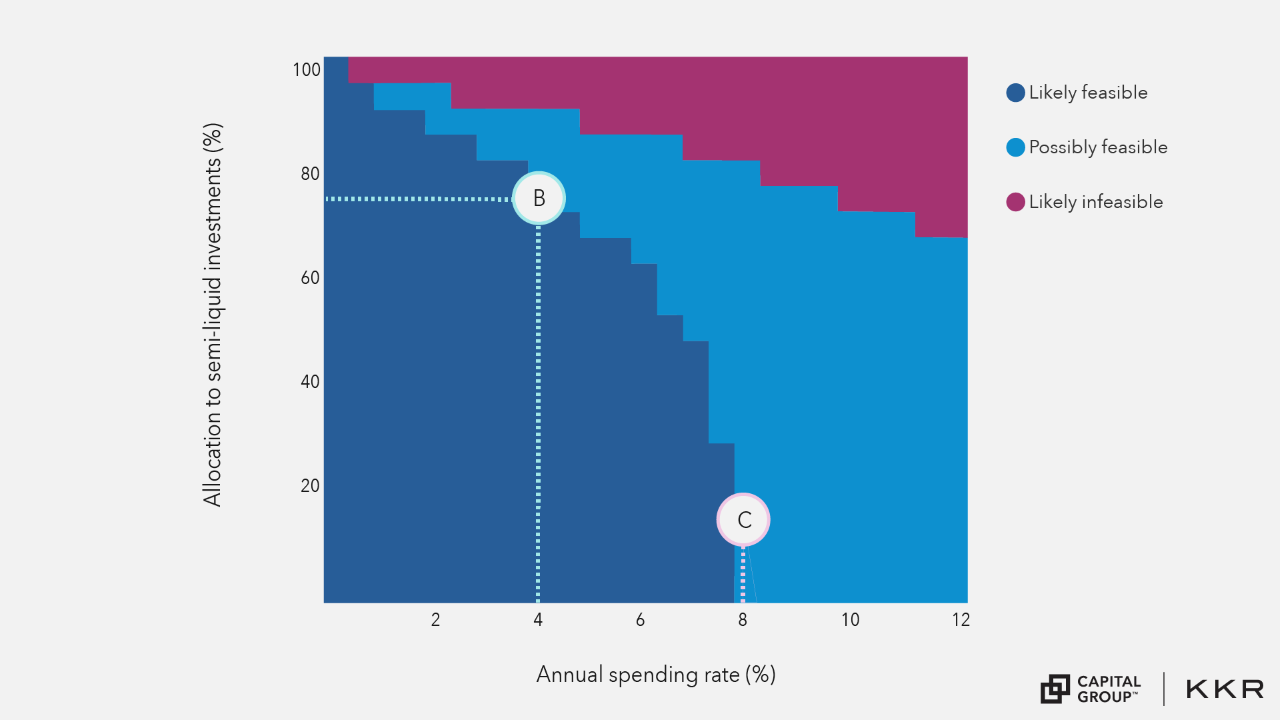

What’s the right proportion of less liquid assets in a portfolio? You’ll need to consider your client’s capacity for risk, time horizon and cash flow needs. If they have multiple short-term commitments, semi-liquid investments like interval funds, might not be for them. Keep in mind the inverse relationship between your client's annual spending rate and the allocation to semi-liquid assets.

Investors with a longer time horizon are typically in the accumulation phase, likely making them a more suitable for a higher proportion of semi-liquid investments within their portfolio. Conversely, those needing cash in the near term are in the distribution phase and may require more liquid assets. Additionally, liquidating portions of a portfolio can disrupt its overall balance. Therefore, we believe it is essential to consider rebalancing the overall portfolio to maintain its intended asset allocation when sourcing liquidity.

[upbeat music]

Your clients will likely have legitimate concerns about the trade-offs that come with semi-liquid investments. First, make sure your clients understand that the semi-liquidity conversation is about both the vehicle type and the assets it holds. Capital Group’s public-private funds combine traditional public assets, such as fixed income, and private credit in interval funds, a less liquid vehicle than mutual funds or ETFs.

You can think of the interval funds as a liquidity compromise: one that allows clients access to typically more liquid assets but with a restricted ability to manage their redemptions compared to traditional mutual funds or ETFs.

Next, you should gauge their liquidity needs, as we discussed earlier in this video. Doing so will help identify those clients who can tolerate a less liquid investment in exchange for potentially higher returns and diversified risk exposures.

As we know, when working with investments with limited liquidity like those found in interval funds, reminding investors of the long-term nature of these assets is important. Realizing the value of these investments, and the potential positive impact on their long-term financial plan, requires holding these investments through a full market cycle.

Riding out market turbulence can often produce better long-term results and interval funds have that “hold tight” mentality already baked into them. Many investors already have a “buy and hold” mindset. If yours do as well, it may be worth noting how these funds complement that idea of being in it for the long haul.

That concludes this video on portfolio considerations for allocating to semi-liquid interval funds. As a next step, you may want to think about who among your investors might be a fit for investing in less liquid products. Until next time.

[upbeat music]