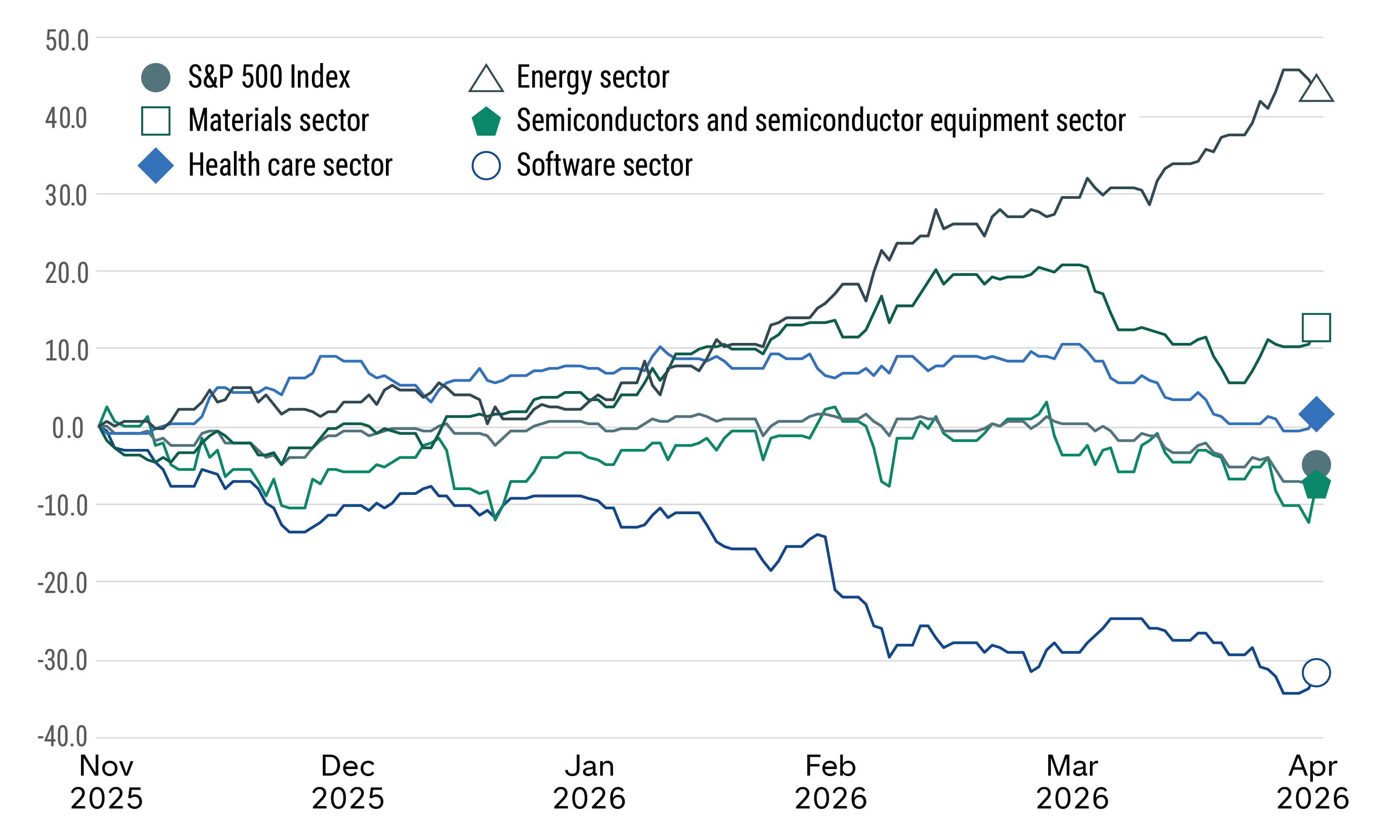

It’s challenging to determine where markets are headed in the current environment. Record-high domestic equity markets, elevated oil prices and economic uncertainty — all impacted by rapidly evolving and unstable geopolitical conflicts — have created a volatile investment climate. Are advisors’ portfolios positioned to protect against potential downside while also being able to take advantage of new opportunities?

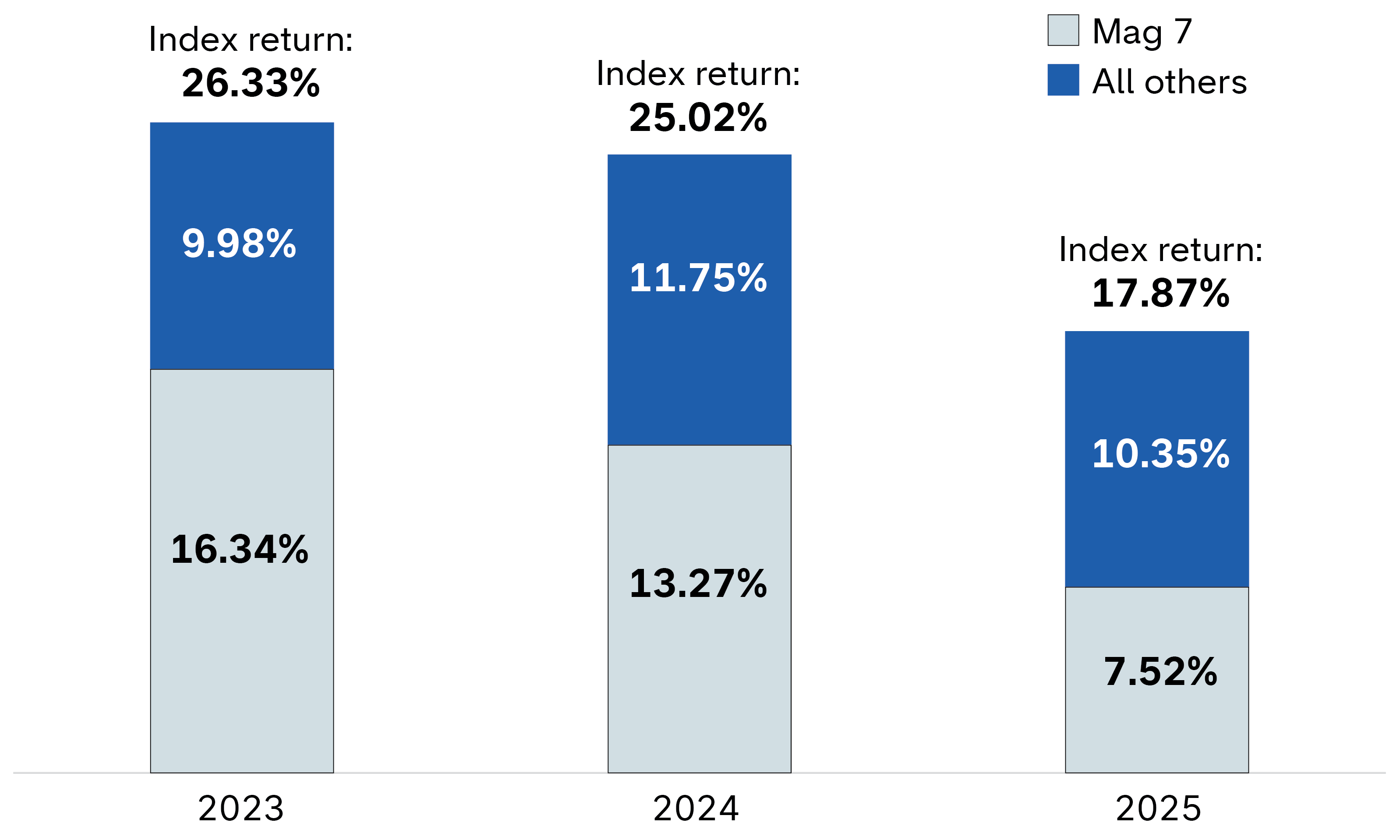

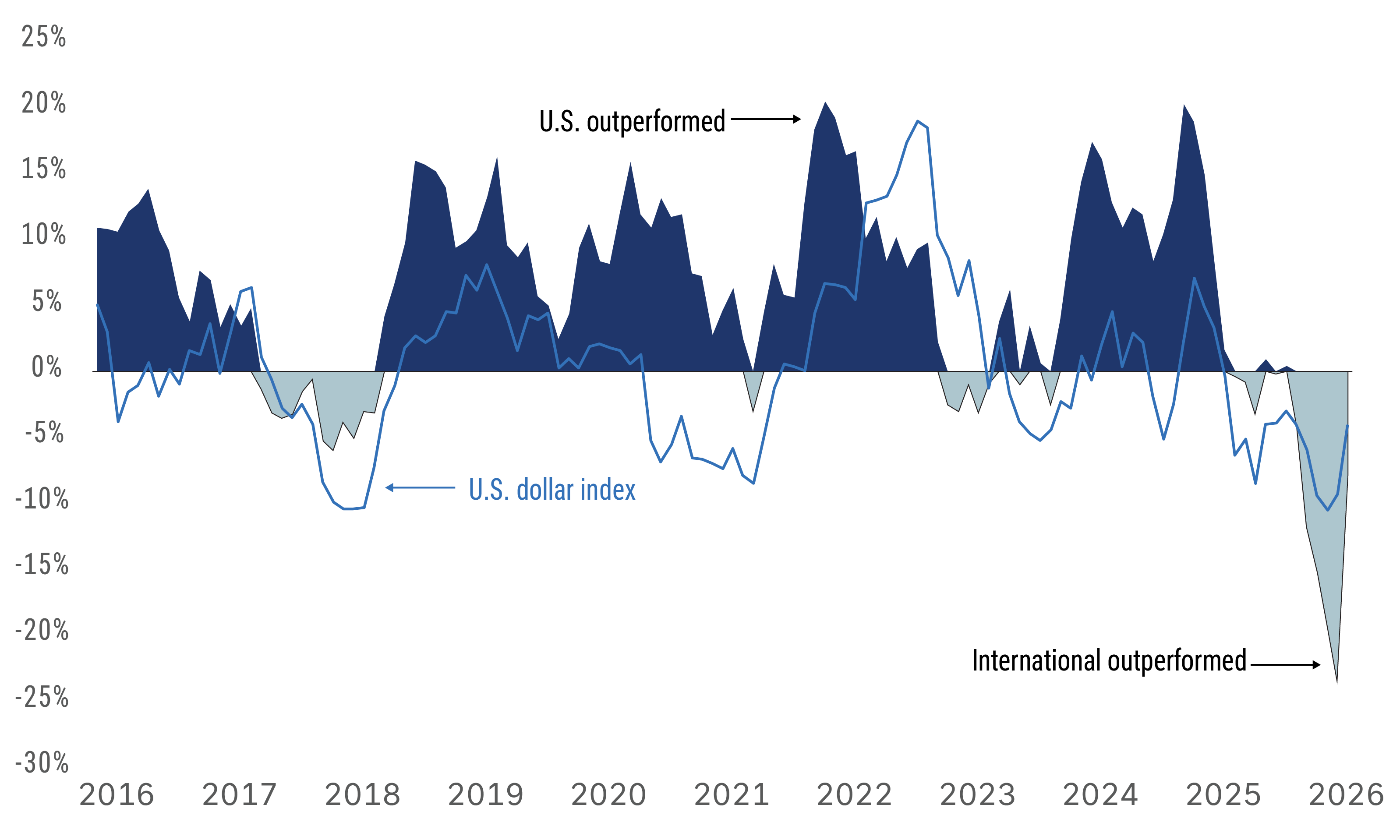

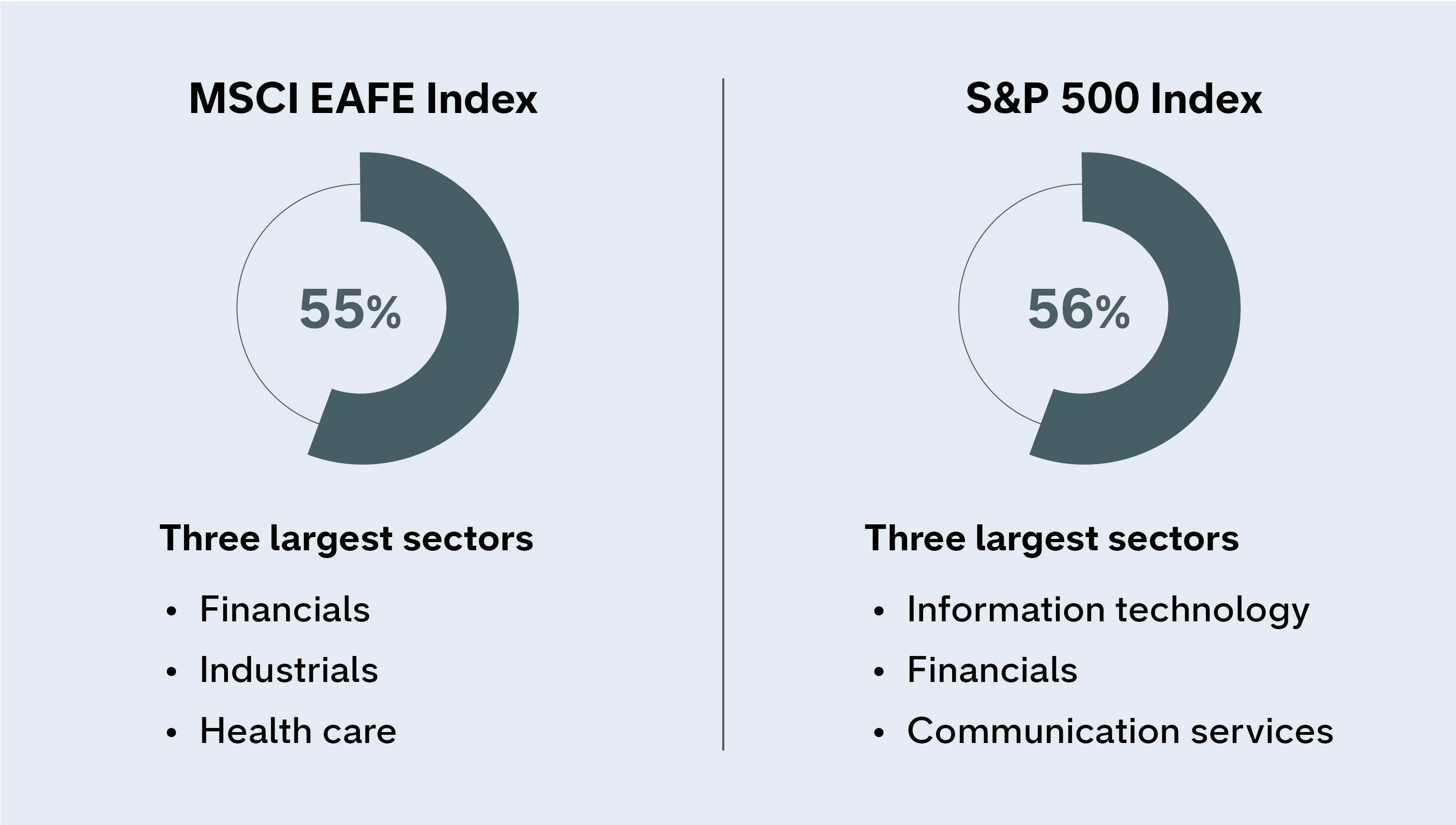

Our analysis of nearly 2,400 advisor portfolios as of March 31, 2026, suggests that investors with large weightings in U.S. passive indexes may not be sufficiently diversified to withstand increasing market volatility. However, this may be reduced by the continued broadening of S&P 500 returns beyond the Magnificent Seven and opportunities for investors to diversify their portfolios through international equities and core and municipal bonds. Advisors should consider a more active approach to capitalize on these opportunities.

Here are four trends that make the case for taking a stronger active approach in portfolios: