[upbeat music]

Justin Park, Managing director of global client solutions at KKR

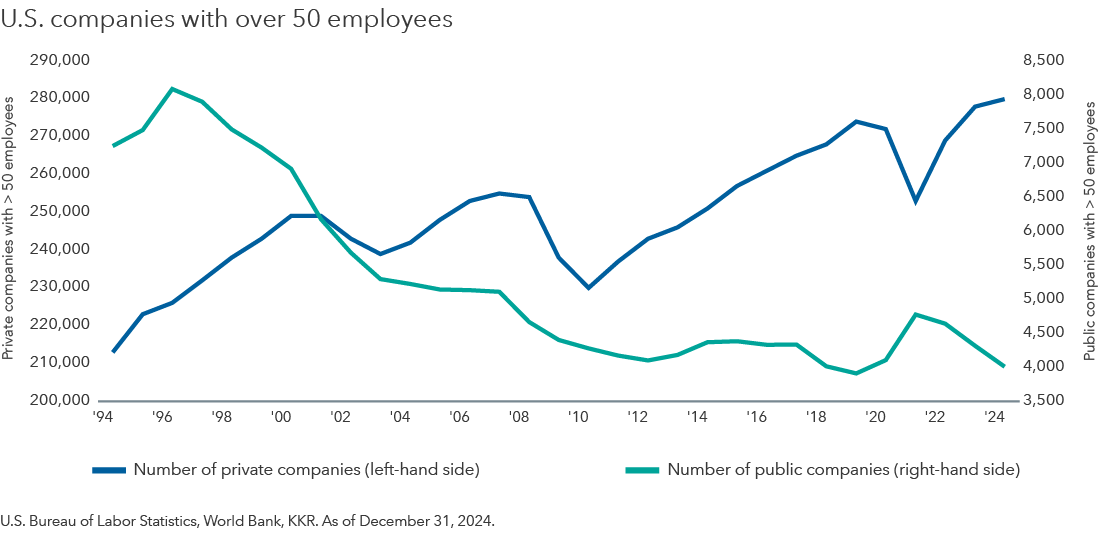

The majority of us know about the stock market, it’s in the news every day. But behind the scenes, private equity powers many of the businesses, products and services people rely on daily. There are many more privately held companies than public ones in the U.S. today.

In this video, we’ll talk about what private equity is, what some of the most common strategies are, and what are some of the risks and potential benefits. Let’s dive in.

In the public equity market, investors buy and sell shares in companies through stock exchanges, but privately held companies do not trade on these stock markets. Private equity is a form of investment in which equity is pooled from various sources, such as wealthy individuals, institutional investors or pension funds, and then used to acquire privately held companies or to purchase publicly held companies and take them private.

In private equity, the investors typically acquire a significant ownership stake in the company, often a controlling interest. This allows private equity firms to directly influence the company's management, operations and strategic decisions, with the goal of improving performance. Investors in traditional public equity strategies usually hold a smaller ownership stake and typically do not have direct control over management decisions.

One of the most common ways investors get exposure to private companies is through a private equity fund, where the private equity firm acts as the general partner or GP and the investors act as Limited Partners or LPs.

The GP’s role includes fundraising, deal sourcing, portfolio management, value creation and formulating the exit strategy, among other things.

The role of an LP is usually passive and revolves around providing capital, sharing in investment returns and relying on the GP to make decisions that align with the fund's strategy and objectives.

It is important to note that private equity investments are less liquid than public equity investments. Unlike public equities that can be traded daily, to allow time for the GP to execute on its value creation plan, private equity typically holds a portfolio company for multiple years.

Historically, private equity funds have not been open to everyone. Many private equity funds tend to have high investment minimums and high investor qualifications. We’ll talk about how the strategic partnership between Capital Group and KKR aims to broaden access to private equity.

Let’s take a closer look at some of the most common types of private equity strategies.

[upbeat music]

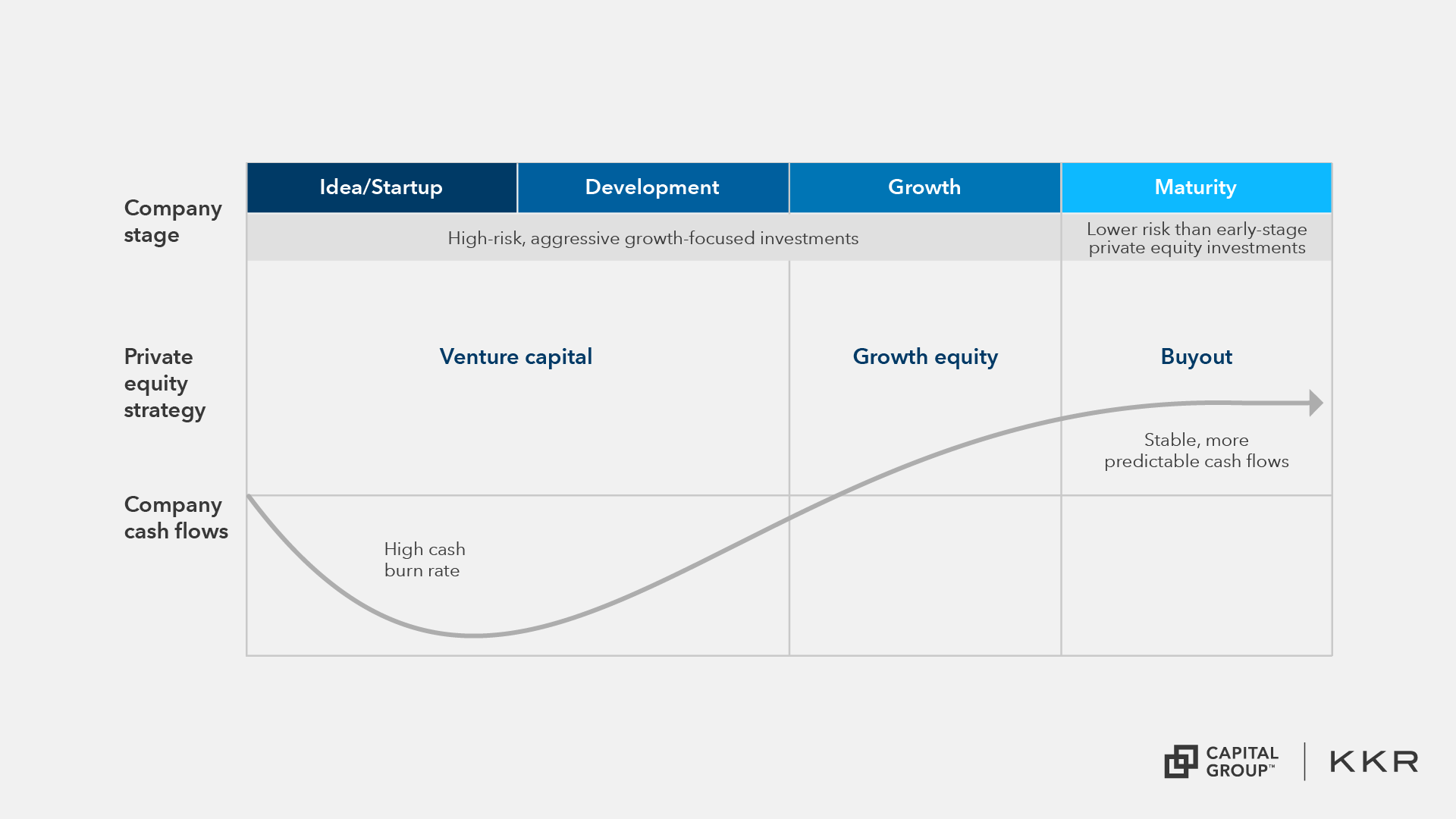

At a high level, private equity strategies often fall into one of three buckets: venture capital, growth equity or buyout. The main differences among these strategies lie in the stage of the company's lifecycle, the level of risk involved and the investment objectives.

Venture capital refers to investments in early-stage companies with high growth potential. Venture capital firms are typically minority investors providing capital to companies that are often in their very early stages and have innovative ideas or technologies.

Growth equity investments are typically made in established companies that have already demonstrated a certain level of success and are looking to expand further. These companies might need additional capital to fund their growth initiatives, such as entering new markets, launching new products or making acquisitions.

In contrast to the previous two strategies, buyout investments involve acquiring a controlling stake or full ownership of a company. Buyout investors often target more mature businesses aiming to improve the company's operations, increase efficiency and enhance profitability during their ownership period. Expected returns might be lower than with a venture capital investment, but the perceived risk is also generally considered lower.

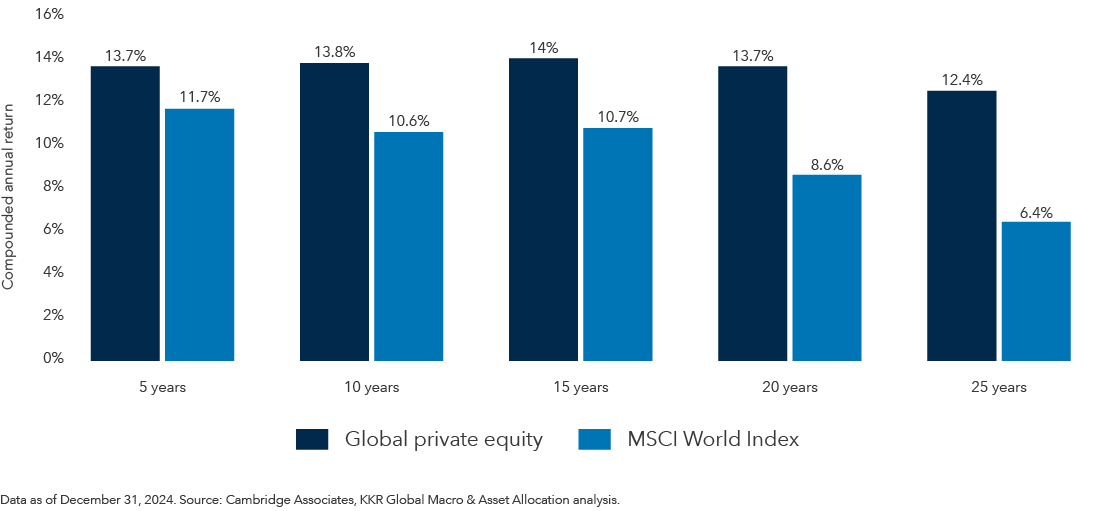

So, why might someone want to invest in private equity? Private equity has historically outpaced public markets due to the illiquidity premium and the ability to take a long-term, hands-on approach to value creation. While public equities offer more liquidity and transparency, private equity can help complement portfolios by tapping into different return drivers over extended time horizons. And while past performance is not indicative of future returns, the strong return potential has been a main driver of interest in private markets.

Private markets are also important for anyone looking to build a more complete equity portfolio. While public companies are often much larger and may command a larger share of any equity sleeve, there is a vast opportunity set of private companies that offer different investment opportunities that often can't be found in public markets. As we mentioned earlier in the video, there are more private companies than there are public ones, and the gap is widening.

An additional consideration is diversification. Private equity sector exposures often differ from public equity indices, making them a strong portfolio diversifier. For example, many innovative, fast-growing tech companies are staying private longer or going public much later in their lifecycle, which leads to less representation in small cap indices.

You’ll learn more about Capital Group and KKR’s approach to private equity investing, and why we think this is an area worth considering. We hope you’ve enjoyed this lesson. Thank you for watching.

[upbeat music]