[upbeat music]

Jan Gundersen, Head of wealth solutions at Capital Group

Hello and welcome. In this video, we’ll start thinking about what role private equity might play in a client’s portfolio, particularly when blended with public equity.

For a long time, private equity was principally the domain of institutional investors and ultra high net worth individuals due to high investment minimums and strict investor eligibility requirements. But as private equity has matured as an asset class, the landscape has shifted.

New products have come to market that make private equity potentially more accessible to a broader swath of investors. One example of these new products is solutions that combine public and private equity into one integrated strategy that may allow more investors to include private markets exposure in their core portfolio.

[upbeat music]

There are multiple reasons why someone might be interested in private equity, including the potential for enhanced returns and added portfolio diversification. If you’ve decided to add some private equity exposure, your first question might be: how should I think of where this sits in my portfolio?

Historically, private equity and other private market asset classes have been thought of as “alternatives” – not stocks, not bonds, but something different. In our view, that may no longer be the case. Instead, we view private equity as part of the larger equity continuum. When thinking of where to source funding for your private equity allocation, we believe it could sit at the core of a client’s portfolio, as an extension of their overall equities’ exposure.

That might help you think of where to consider this exposure fitting in. But how much exposure is appropriate? As with any exercise in portfolio construction, you have to consider a client’s objectives, risk capacity and a host of other factors in order to make the most appropriate decisions for them. Let’s explore some possible scenarios.

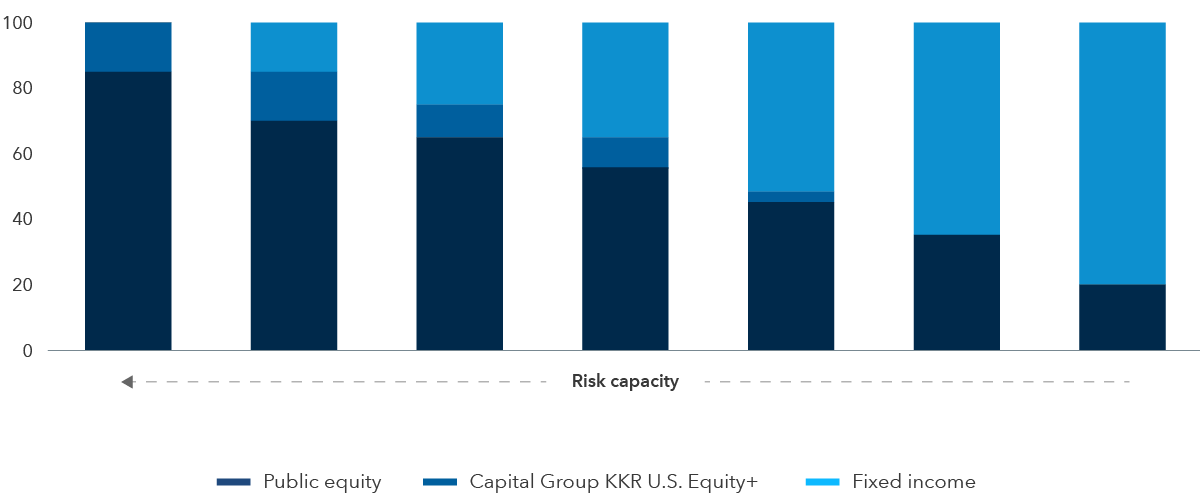

Imagine a client who is early in their career. They have a long time horizon, a high tolerance for illiquidity and a sizable appetite for risk. Perhaps their current portfolio is 100% public equities.

For an investor like that, whose primary objective is long-term growth of capital, a 15% allocation to a blended public-private equity solution could be considered. That level aims to balance capital appreciation potential with concentration risk to any specific private equity investment. For the purposes of these examples, we’ll use Capital Group KKR U.S. Equity+ for that semi-liquid private equity exposure.

Consider another example: A hypothetical client who is a little further in their career, maybe a little closer to retirement, but still with an interest in long-term growth. This investor might be willing to take on illiquidity but is more risk-averse than the previous example and a bit more interested in managing volatility.

Instead of a portfolio entirely composed of equities, that kind of investor may be closer to a 65/35 stock-to-bonds allocation. There’s still room there to add some private markets exposure. Carving out 9% for Capital Group KKR U.S. Equity+ might offer potential benefits in the form of higher total return potential and diversification of portfolio growth drivers.

There is no one-size-fits-all approach when it comes to building client portfolios. Private markets exposure may not be appropriate for every client, and if you do feel an allocation is appropriate, the exact amount can vary notably from client to client.

In the accompanying lesson materials, we’ll share a few more ideas about how a potential portfolio could look. We hope you’ll find that helpful, and we thank you for watching.

[upbeat music]