[upbeat music]

Patrick Nelson, Principal of private equity strategies at KKR

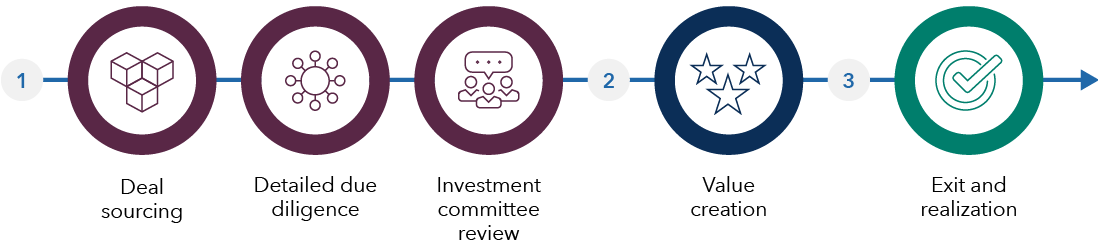

Welcome. In this lesson, we’ll go deeper into how private equity works. We’ll cover the lifecycle of a private equity investment from acquisition to exit and talk about some of the strategies managers can use to create value within a portfolio company.

[upbeat music]

Company acquisitions are at the end of the first stage of the investment lifecycle, which starts with deal sourcing and due diligence. This is a process that can often span multiple years. Depending on their size, scale and investment focus, a private equity firm might consider hundreds, even upwards of a thousand potential target companies every year and end up investing in only a small percentage of them.

While acquisitions can follow different transaction types, including purchasing a company from its founder, three of the more commonly discussed transactions are corporate carveouts, public to privates and acquiring companies from an existing private equity owner, otherwise known as a sponsor-to-sponsor transaction.

A corporate carve out is a transaction where a private equity firm purchases a specific business unit, division or subsidiary from a larger parent company. The classic carve-out thesis is that a private equity firm can help unlock significantly more value from a non-core business unit than the parent company could. However, these transactions require knowledge and resources, as they are complex, involving significant operational disentanglement from the parent company and requiring careful structuring around legal, IT and operational integration issues.

A public to private transaction is a process where a private equity manager takes a controlling interest in a publicly listed company and delists it from a stock exchange. A sponsor-to-sponsor transaction occurs when one private equity firm sells its portfolio company investment to another private equity firm. Sponsor-to-sponsor deals have become a significant component of the private equity market where, for example, a growth focused private equity manager may sell its portfolio company to a manager that is more focused on companies that have reached the next phase of maturity in their lifecycle. We’ll talk more about that in a moment when we touch on exit strategies.

[upbeat music]

Ultimately, the goal for a private equity firm is to exit its investments and realize the value that was created on behalf of its investors. There are several ways private equity managers can directly influence a company's strategy and help create that value.

One way is by strengthening the management team. Private equity managers might work with the existing management team to enhance their capabilities or bring in new talent. This ensures that the company's leadership is aligned with the strategic goals.

Another way is through acquiring other companies which could open up new product offerings, exposure to new markets and perhaps a new area of specialized knowledge or technology that can be integrated with the goal of creating synergies.

Streamlining and improving operations is yet another value creation lever. Working with management teams to identify and implement operational improvements is essential to ensuring there is alignment with the desired outcome.

Lastly, private equity firms may use financial strategies to help enhance returns. This could include refinancing existing debt at lower interest rates, restructuring the company's balance sheet or implementing a tax-efficient approach to help improve cash flow and potential profitability.

[upbeat music]

Finally, let’s turn our attention to exit strategies. Selecting investments that could pursue multiple exit routes and then building the value that makes them desirable to potential buyers during the holding period can enable a successful exit down the road. Planning for exits early, taking a creative and flexible approach to the exit plan and trying to make good companies great, makes even the most difficult environments navigable.

Exits typically come in three routes: strategic sales to a company within the same industry, sponsor-to-sponsor sales in which a company is sold to another financial sponsor, whether that be another private equity manager, a sovereign wealth fund or a pension plan and finally, the public market route, which would refer to an IPO in which the company lists on a public exchange.

To have multiple exit routes available in a variety of market environments, it helps to own companies that many buyers also want to own. That starts with selecting the right companies and continues with making those companies more valuable through repeatable playbooks. An approach that balances flexibility and discipline, along with getting the fundamentals of operational improvement right, is key for private equity managers.

We hope this lesson has helped deepen your understanding of how private equity funds operate. Thanks for watching.

[upbeat music]