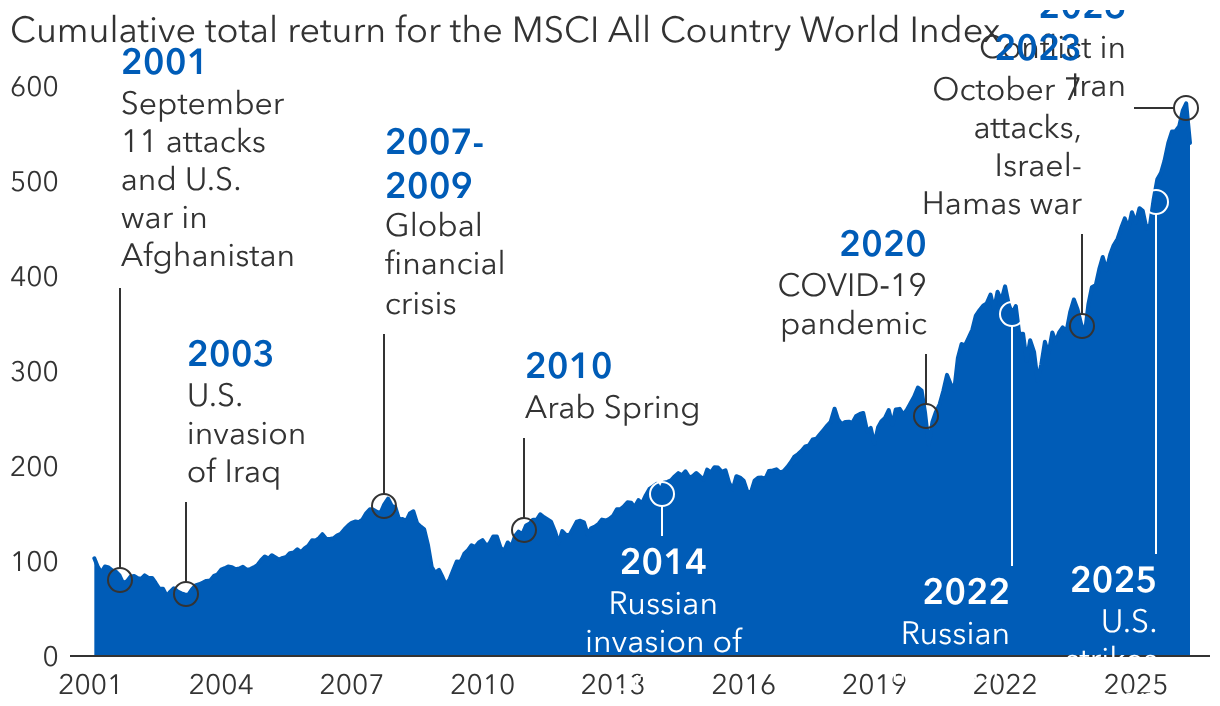

Investors are climbing a high wall of worries in 2026. With wars in the Middle East and Ukraine, messy trade disputes in the world’s major economic regions, growing fears over the impact of artificial intelligence, and deep political divisions in the United States and elsewhere, it can be difficult to remove emotions from practical investment decisions.

The war in Iran is the latest example. Each day brings a new distressing headline about a fragile ceasefire, elevated oil prices and the threat of renewed military action. The world looks terrible right now. It often looks terrible. But at times like these, I always try to remember that difficult times can also bring compelling investment opportunities for patient, long-term investors.

I’ve been in this business now for nearly 40 years, and I have counted the number of market disruptions I’ve experienced. It’s about 25, which means there has been a major event in the market, on average, every 18 months during my career. So I’m not saying be happy about bad times; I’m saying remember what they represent. Remember that they can present opportunities as share prices go on sale. And, perhaps most importantly, remember that a better day is coming.