Kevin Warsh is stepping into the top spot at the Federal Reserve at a challenging moment. Inflation has risen amid the U.S.-Iran conflict, labor markets are uneven and signs of growing internal dissent within the Fed are emerging. Against this backdrop, the path to lower interest rates has become less clear, raising the stakes for both policy decisions and market expectations.

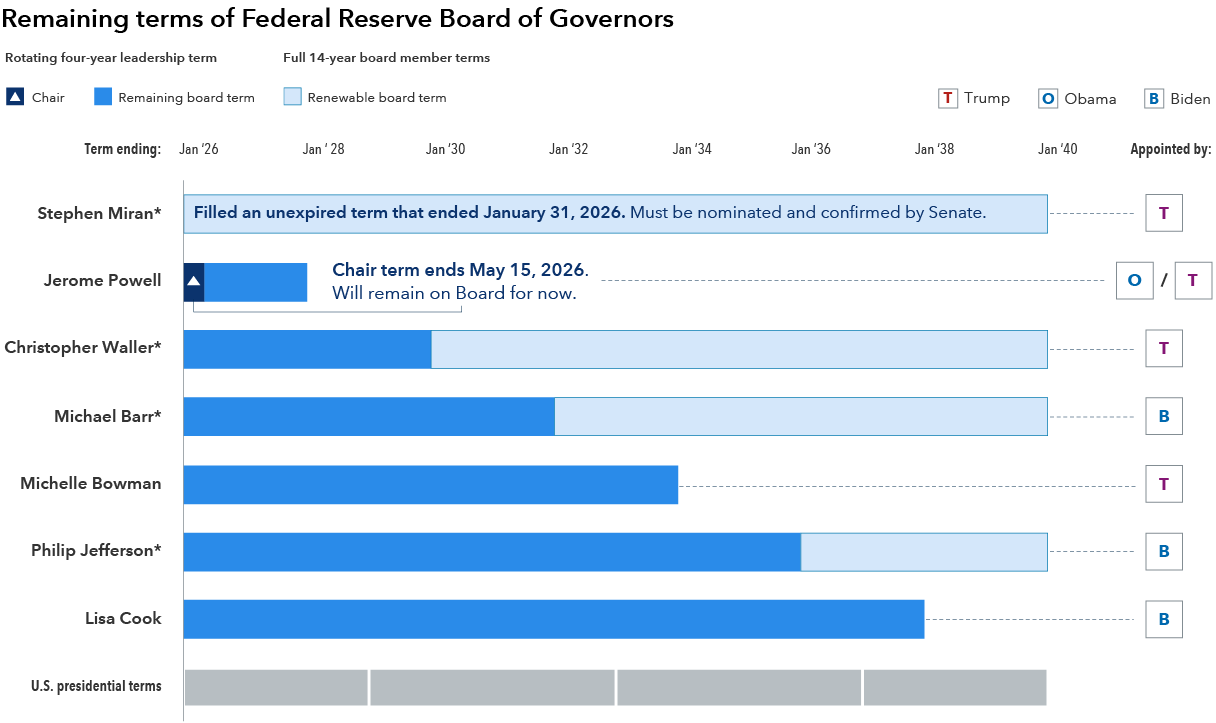

Importantly, Jerome Powell indicated he’ll remain on the Fed’s Board of Governors until the investigation of the Fed building renovation is complete. Members of our fixed income investment team continue to expect institutional continuity at the Fed, which should limit political influence over the central bank.

The collective judgment of the Federal Open Market Committee (FOMC) and the Board of Governors remains central to policymaking. Governors serve staggered 14-year terms that deliberately extend across multiple presidential administrations, providing insulation from short-term political pressures and limiting the extent to which any single chair can unilaterally redirect policy.