Past results are not predictive of results in future periods.

Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor's, Moody's and/or Fitch, as an indication of an issuer's creditworthiness.

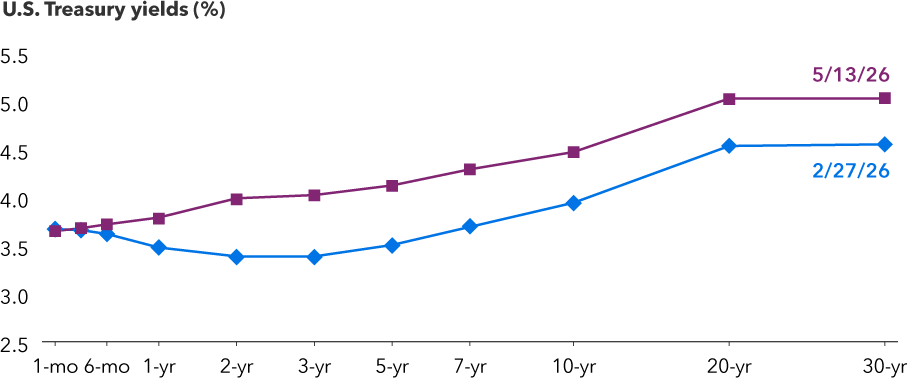

Duration measures a bond’s sensitivity to changes in interest rates. Generally speaking, a bond's price will go up 1% for every year of duration if interest rates fall by 1% or down 1% for every year of duration if interest rates rise by 1%.

A range bound rate environment refers to periods when interest rates move up and down within a relatively narrow band, rather than trending steadily higher or lower.

The indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

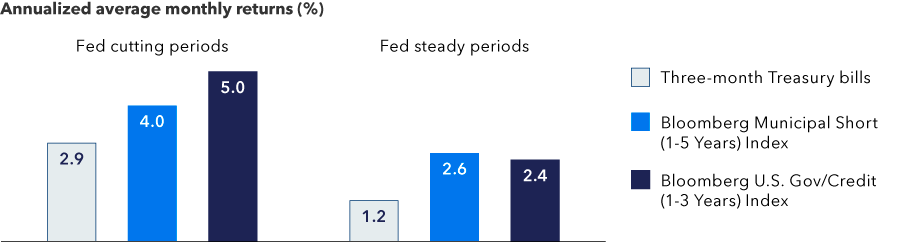

Bloomberg U.S. Government/Credit (1-3 Years) Index is a market-value weighted index that tracks the total return results of fixed-rate, publicly placed, dollar-denominated obligations issued by the U.S. Treasury, U.S. government agencies, quasi-federal corporations, corporate or foreign debt guaranteed by the U.S. government, and U.S. corporate and foreign debentures and secured notes that meet specified maturity, liquidity and quality requirements, with maturities of one to three years.

Bloomberg Municipal Short 1-5 Years Index is a market-value-weighted index that includes investment-grade tax-exempt bonds with maturities of one to five years.

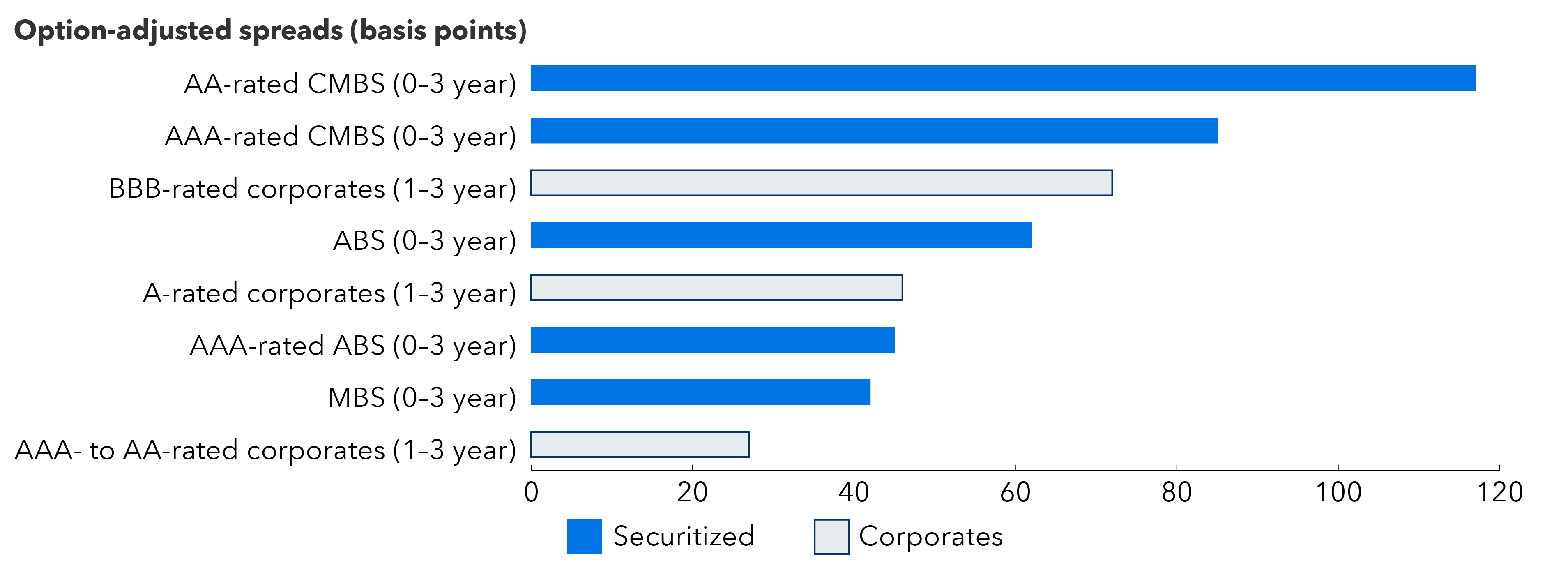

The ICE BofA U.S. Fixed Rate CMBS Index tracks the performance of U.S. dollar denominated investment-grade fixed-rate commercial mortgage-backed securities publicly issued in the U.S. domestic market.

The ICE BofA U.S. Fixed Rate Asset Backed Securities Index tracks the performance of U.S. dollar denominated investment-grade fixed-rate asset-backed securities publicly issued in the U.S. domestic market.

The ICE BofA U.S. Mortgage Backed Securities Index tracks the performance of U.S. dollar denominated fixed-rate residential mortgage pass-through securities publicly issued by U.S. agencies Fannie Mae, Freddie Mac and Ginnie Mae in the U.S. domestic market.

The ICE BofA U.S. Corporate Index tracks the performance of U.S. dollar denominated investment-grade corporate debt publicly issued and settled in the U.S. domestic market.

The ICE BofA 3-month U.S. Treasury Bill Index measures the performance of a single issue of outstanding treasury bill which matures closest to, but not beyond, three months from the rebalancing date. The issue is purchased at the beginning of the month and held for a full month; at the end of the month that issue is sold and rolled into a newly selected issue.

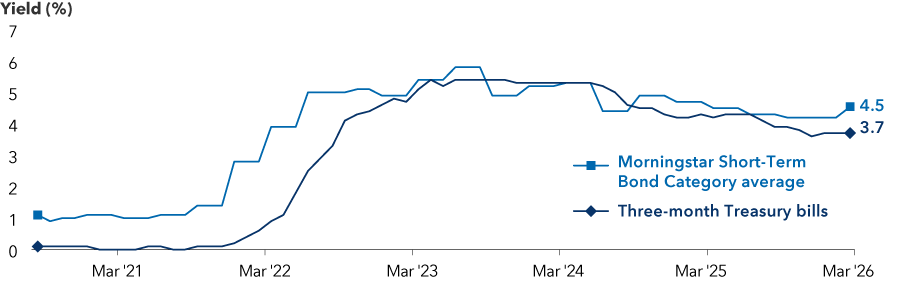

The Morningstar Short-Term Bond Category includes bond portfolios that invest primarily in corporate and other investment-grade U.S. fixed-income issues and typically have durations of 1.0 to 3.5 years. Morningstar calculates monthly breakpoints using the effective duration of the Morningstar Core Bond Index (MCBI) in determining duration assignment. Short-term is defined as 25% to 75% of the three-year average effective duration of the MCBI.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

© 2026 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar, its content providers nor Capital Group are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Information is calculated by Morningstar. When applicable, due to differing calculation methods, the figures shown here may differ from those calculated by Capital Group.

ICE Data Indexes are a product of ICE Data Indices, LLC (“ICE Data”) and is used with permission. ICE® is a registered trademark of ICE Data or its affiliates. BOFA® is a registered trademark of Bank of America Corporation licensed by Bank of America Corporation and its affiliates (“BOFA”) and may not be used without BOFA's prior written approval. ICE Data, its affiliates, and their respective third party suppliers disclaim any and all warranties and representations, express and/or implied, including any warranties of merchantability or fitness for a particular purpose or use, including the indices, index data and any data included in, related to, or derived therefrom. Neither ICE Data, its affiliates nor their respective third party suppliers shall be subject to any damages or liability with respect to the adequacy, accuracy, timeliness or completeness of the indices or the index data or any component thereof, and the indices and index data and all components thereof are provided on an “as is” basis and your use is at your own risk. Inclusion of a security within an index is not a recommendation by ICE Data to buy, sell, or hold such security, nor is it considered to be investment advice. ICE Data, its affiliates and their respective third party suppliers do not sponsor, endorse, or recommend Capital Group, or any of its products or services.