We are living through an extraordinary market environment. The level of concentration in many equity benchmarks has increased significantly.

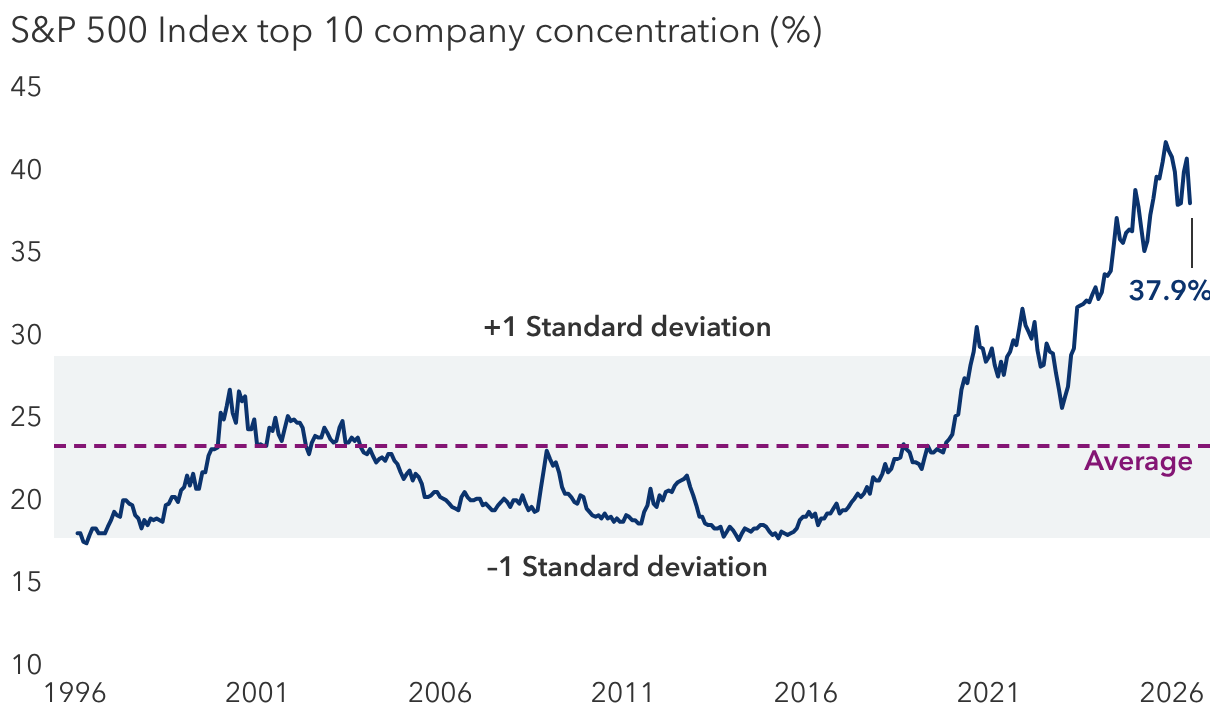

The evidence is striking. The 10 largest companies in the S&P 500 represent nearly 40% of the index, a level not seen since the mid-1960s. Semiconductor-related companies are approaching one-fifth of the S&P 500. In emerging markets, the exposure is even more acute: Three companies alone — TSMC, Samsung and SK hynix — represent 29% of the MSCI EM Index.

As this concentration grows amid investor euphoria, I felt it appropriate to remind Capital’s investment group of our responsibilities, which I did in collaboration with Capital Group Vice Chair Jody Jonsson and CEO Mike Gitlin. I want to share those same thoughts with you now.

As I told my colleagues, Capital Group’s mission to improve people’s lives through successful investing carries a deep obligation. We are entrusted with the savings of individuals, families and institutions who rely on us to grow their wealth, generate income, fund retirements, support beneficiaries and leave enduring legacies.

That requires us to pursue superior long-term outcomes on a risk-adjusted basis with the discipline to help protect, to the best of our abilities, our clients’ savings during market extremes. We should not simply mirror the risk profile of an index when that index becomes unusually concentrated or extended, as is increasingly the case in markets around the world today.