Investors looking at their portfolio’s year-to-date results through March may be concerned with weak results in both stock and bond allocations. Impacts from the Iran conflict shook markets, increasing uncertainty around inflation and prompting a reassessment of interest rate expectations globally. As equities fell in March, bond yields moved higher. This relationship may induce flashbacks to 2022, when the two markets endured a period of correlated losses. However, we do not see the March energy price spike or its broader impact as likely to lead to a similar outcome.*

April 9, 2026

KEY TAKEAWAYS

- Fixed income markets turned negative in March, as oil prices spiked amid the Iran conflict.

- Yields rose when investors priced in a higher probability of stagflation.

- History and models imply markets may be overestimating inflationary pressures.

- Managers see more opportunity in positioning for lower yields.

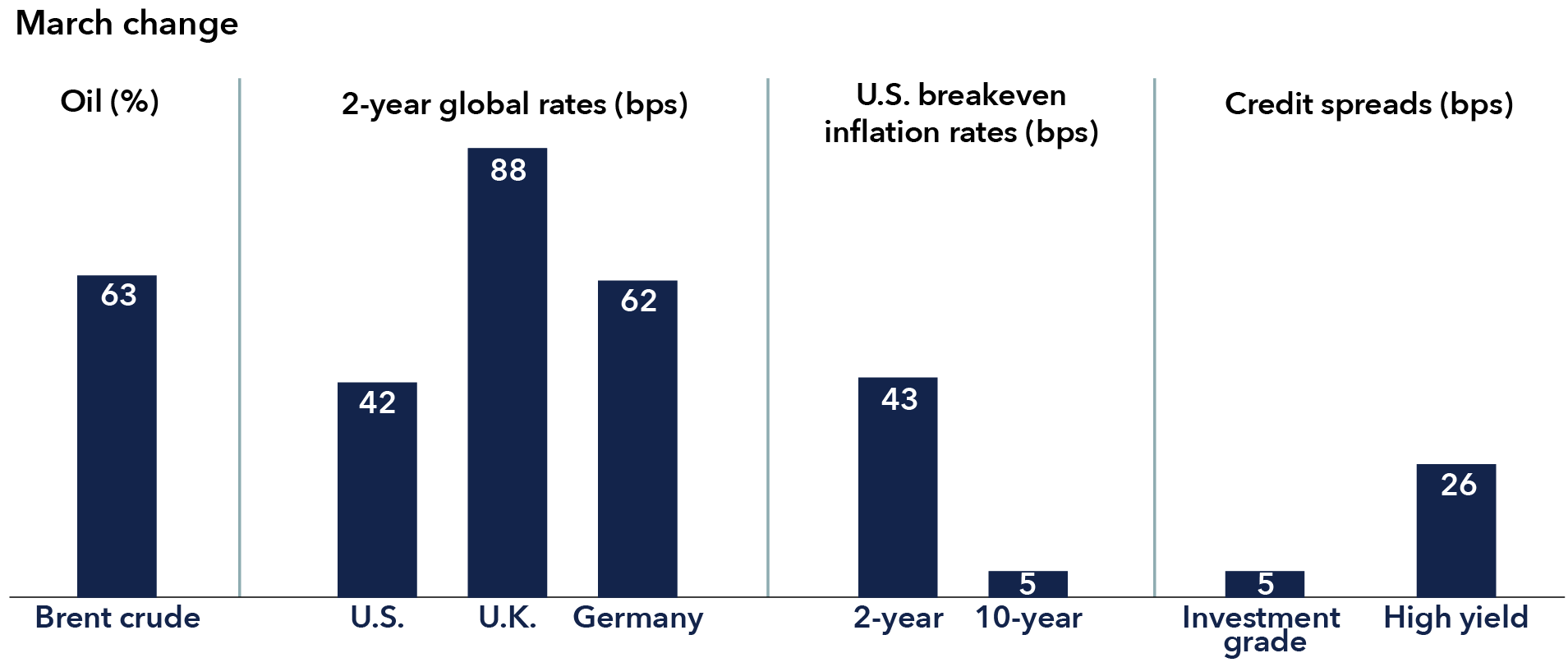

Some markets slipped on the oil-driven disruption

Energy-related inflation risk tied to the conflict involving Iran raised concerns about the greater likelihood of a stagflation. Thus far, bond investors appear more focused on the inflationary impact than macro implications.

The Federal Reserve — which has a dual employment/inflation policy mandate unlike some of its developed peers with a singular inflation focus — held rates steady in March. It emphasized a data-dependent approach amid elevated inflation uncertainty, signaling a willingness to wait for greater clarity rather than react to short-term fluctuations.

Yield curves flattened, with short-term yields rising faster than long-term yields, as inflation concerns prompted the market to price in greater monetary policy uncertainty. Rather than a typical risk-off episode that affects credit markets and interest rates, impacts have been more prominent in interest rate spot and forward markets. Credit has remained mostly insulated from concerns about either growth or rising prices.

Spiking oil prices impacted rates and inflation expectations more than credit

Source: Bloomberg. As of March 31, 2026. Global rates based on U.S. Treasuries, U.K. gilts and German Bunds. Breakeven inflation rates are based on U.S. Treasury Inflation-Protected Securities. Investment grade (BBB/Baa and above) represents the Bloomberg U.S. Corporate Investment Grade Index. High yield represents the Bloomberg U.S. Corporate High Yield 2% Issuer Cap Index.

Why we remain bullish on bonds

Despite energy prices driving inflation higher, several factors should keep it grounded over the longer term. Savings are much lower today than in 2022, as consumers had saved money during the pandemic. This should lead to less demand-driven price increases. U.S. fiscal policy stimulus is also much weaker now than what was implemented following the 2020 recession. Finally, labor markets are in a weaker place, with the impacts of artificial intelligence weighing on job creation. This should keep wage growth – a major driver of inflation – at more modest levels.

If non-energy price inflation remains tame, the Fed is more likely to focus on the full employment side of its mandate and follow through with its plan for gradually lower rates. Fed actions support this likelihood, as the board raised its forecast for core personal consumption expenditures (PCE) inflation, its preferred policy metric, but left its projection for a cut in 2026 intact. Energy-related disruptions to the broader economy could also lower growth, which could potentially accelerate that path. This outcome could have a positive impact on duration and fixed income returns.

How we’re tackling uncertainty

In terms of global growth more broadly, our outlook remains positive, but more fragile than at the start of the year. Geopolitical developments have increased uncertainty and skewed risks toward more stagflationary outcomes if elevated energy prices persist. In the U.S., large-scale investment in areas such as AI continue to support growth, even as labor market conditions has shown signs of cooling.

In this environment, Capital Group fixed income portfolio managers are emphasizing diversification, quality and resilience. While higher yields have improved income potential and long-term return prospects, valuations across many risk assets remain tight and may not yet fully reflect the range of both macro and geopolitical risks. The potential for higher inflation has been the market’s focus so far. However, a shift toward the potential for a negative impact on growth could drive a reversal— moving rates lower and credit spreads wider.

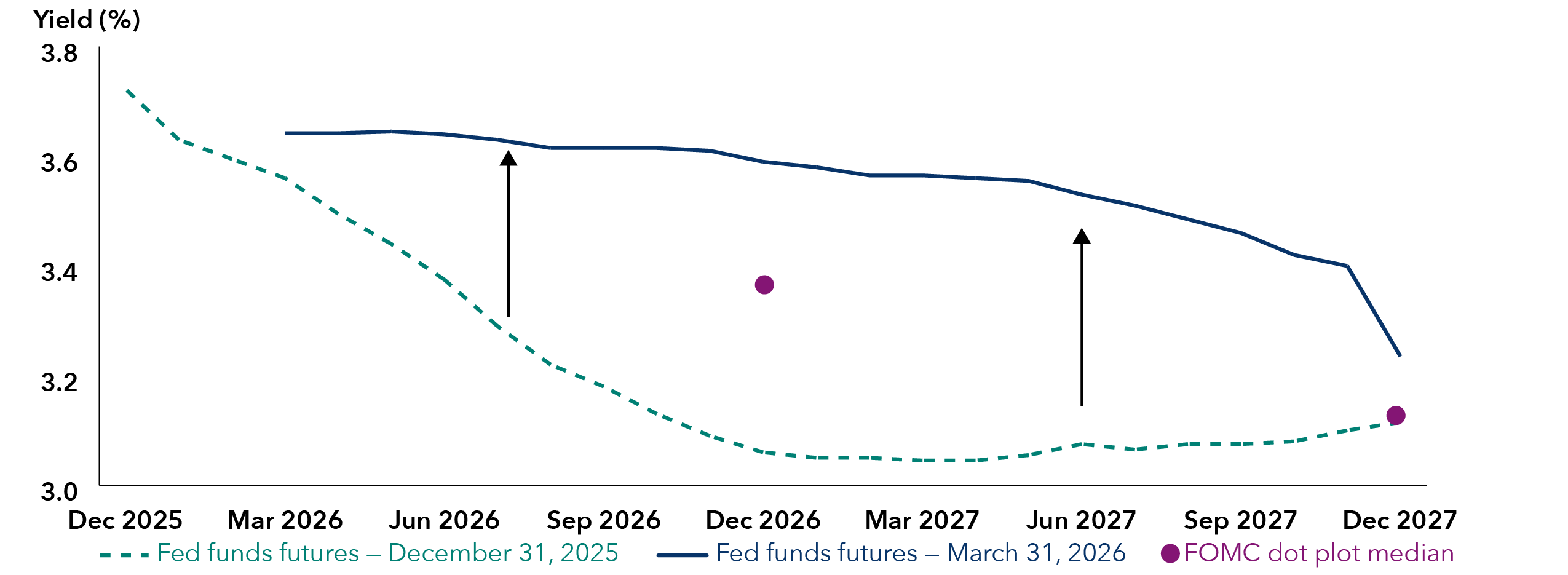

As rates have repriced, our portfolio managers have found duration more attractive, considering the fundamental backdrop of slowing growth, a weak labor market and a Fed that can look beyond energy-related inflation, given its dual mandate. Although the Fed sounded more hawkish in March, it also forecast a rate cut in 2026, with the unemployment rate where it is today at 4.4% and higher inflation expected this year.

Our analysis suggests the market reaction may be pricing a larger and more persistent impact on core inflation than history or models imply. Historical episodes of sharp oil price increases over the past two decades indicate while yields often rose in the short term, there was no consistent relationship between the initial oil shock and longer term Treasury yield levels, underscoring the variability of outcomes. Model-based work, including our internal analyses and Fed research, also suggest oil price shocks tend to have a limited pass-through to core inflation. A longer energy price shock, however, could magnify downside risks to growth via lower consumer spending in the face of higher energy prices and/or uncertainty reducing corporate hiring and investment.

Futures imply no 2026 easing, with rates above most Fed dots through 2027

Sources: Capital Group, Bloomberg, U.S. Federal Reserve. The fed funds target rate shown is the midpoint of the 50 basis-point range the Federal Reserve aims for in setting its policy interest rate. Market-implied effective rates are a measure of what the fed funds rate could be in the future and are calculated using fed funds rate futures market data. Median Fed projections are based on the Summary of Economic Projections released by the Federal Open Market Committee on March 17, 2026.

Market pricing, therefore, may be placing too much weight on sustained inflation pressure while underappreciating the probability of economic softening. In addition to adding duration exposure, curve positioning designed to benefit from short-term yields outperforming intermediate maturities remains attractive.

Managers are approaching spread exposure selectively, with a focus on structures and sectors that can better withstand periods of elevated volatility. Rather than positioning portfolios for a single macroeconomic outcome, they are focused on balancing risks across return drivers and preserving liquidity and flexibility as valuations and fundamentals evolve. With a muted reaction and little dispersion of impacts across credit markets so far, risk-reward analysis has favored moving spread exposure up in quality to build resilience. A sustained conflict could drive spreads wider, with higher risk areas of the market likely underperforming in that scenario.

As markets adjust to a more uncertain macro backdrop, managers remain focused on fundamentals and disciplined portfolio construction rather than reacting to short-term volatility.

Margaret Steinbach is the asset class lead for fixed income and oversees the team of investment directors in North America. She has 18 years of investment industry experience (as of 12/31/2024). She holds a bachelor’s degree in commerce from the University of Virginia.