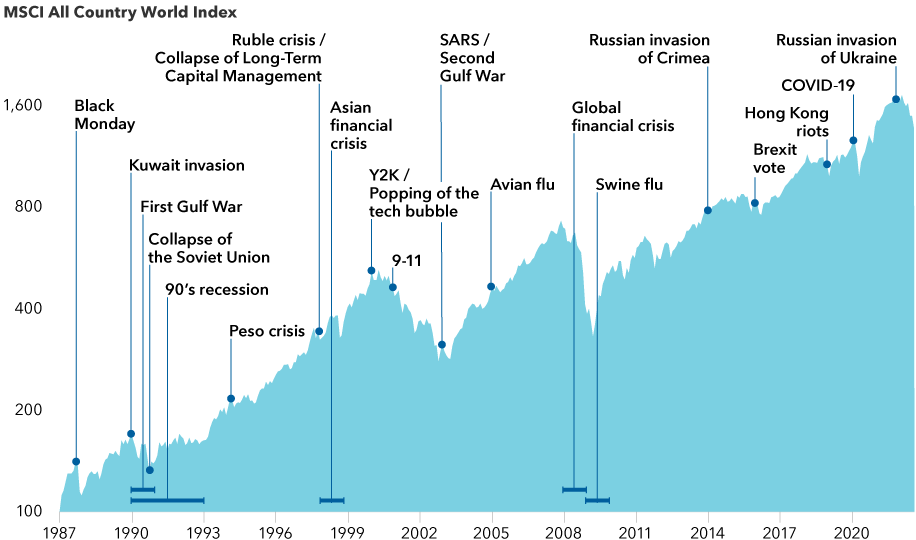

This past winter I celebrated my 35th anniversary in the fund management business, and that milestone prompted me to start jotting down lessons I’ve learned along the way. I thought it might also be useful to share some perspective on how I’ve come to accept market crises as both inevitable and frequent, and how I’ve learned to manage through them.

I stumbled into this industry in 1987 because the China‐focused consulting boutique I worked for was going bust and my wife was pregnant with our first child. I talked to a headhunter who asked if I had considered equity research. Given my somewhat unconventional background, she said the only fund management firm in New York that might consider hiring me was Sanford Bernstein. It didn’t hurt that like Bernstein’s then-president, Lew Sanders, I had once driven a taxicab. Amazingly enough, it worked.