[upbeat music]

Tal Reback, Global credit & markets investment strategist at KKR

Interest in private credit is growing, and that’s no surprise. Private credit has the potential to provide higher yields and a useful source of diversification when compared to traditional fixed income assets.

[upbeat music]

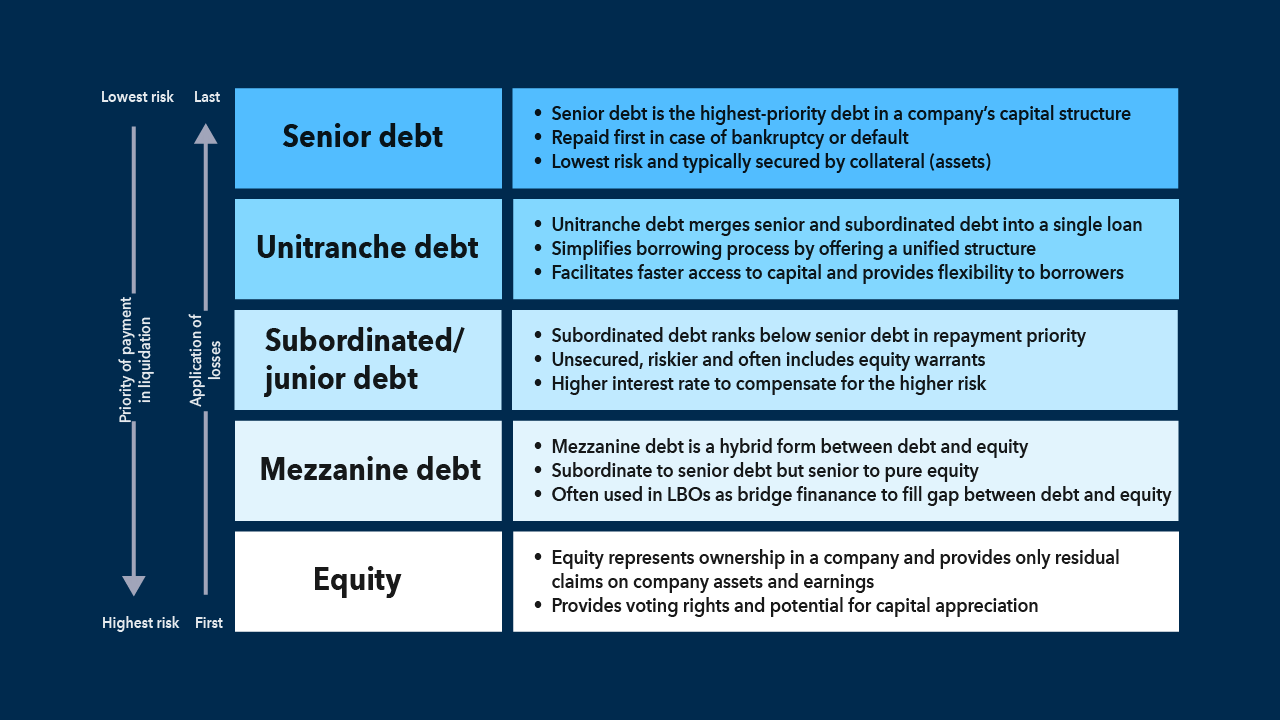

There are several asset classes within private credit, broadly classified into five major categories: secured direct lending, asset-based finance, junior and mezzanine debt, venture debt and distressed debt.

Two largest segments of the private credit market in terms of AUM are secured direct lending and asset-based finance. These investments, while certainly not without risk, tend to be lower on the risk spectrum than other categories of private credit.

These are the kinds of investments likely to appeal to some investors due to their potential, stable income and modest overall risk compared to mezzanine, venture and distressed debt. Direct lending and asset-based finance are areas of focus as Capital Group and KKR partner to bring private market investments to investment funds. Now, let’s take a look at these types of investments.

[upbeat music]

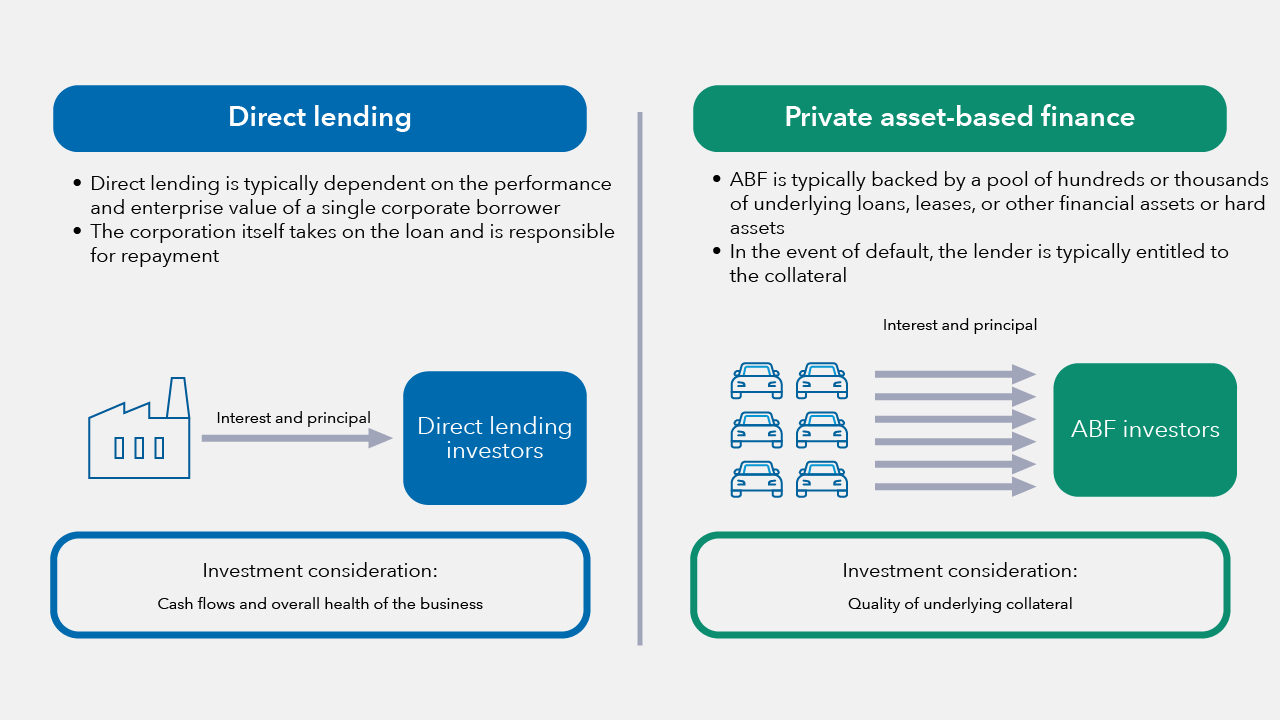

Secured direct lending, also known just as “direct lending”, consists of senior secured loans made directly to companies. Direct lending can serve business needs like buyouts, refinancing, recapitalization or growth initiatives.

Their senior secured status means that if there were a problem at the borrower company, this would typically be the first debt repaid and is backed by collateral in the event of a default. That’s not to say that the senior loans are without risk, but they are generally less risky than loans further down a company’s capital structure.

So, what makes direct lending an appealing investment? Private direct lending typically has had a higher interest payment advantage relative to certain comparable credit investments, due to cash flows generated from repayments dictated by contractual loan terms.

Part of this return advantage has been due to the illiquidity premium or additional yield often received for this type of loan as a part of the compensation for the illiquidity risk.

We’ll talk about this aspect of private credit a lot throughout these materials because it’s a key concept with your clients. Basically, these loans are less liquid than public credit so, they command higher yields. That suggests potentially greater returns, as well as risks, for investors that can hold them to maturity, which may be over a medium or long term.

Direct loans are typically held to maturity or refinanced rather than traded. Their value lies in the investment manager’s skill at originating, underwriting and managing the loans. Selecting private credit investments from established, experienced and well-resourced managers may help investors feel more confident in the potential these types of investments could provide in an investment portfolio. In addition, direct loans can offer floating rates that help adapt to changes in interest rates, which offers a hedge against interest rate risks.

[upbeat music]

Now, let’s turn to asset-based finance, or ABF. ABF can encompass a diverse array of assets: leased aircraft and rail cars, mortgages and auto loans, rental equipment and even royalties from intellectual property. ABF has tended to have less exposure to the corporate credit cycle, since it derives its value from diversified collateral.

As next steps, you might want to start thinking about which of your clients might be a good fit for these investments. Think about who might be interested in taking on some illiquidity and risk, in exchange for the potential long-term returns. Until next time.

[upbeat music]