[upbeat music]

John Queen, Fixed income portfolio manager at Capital Group

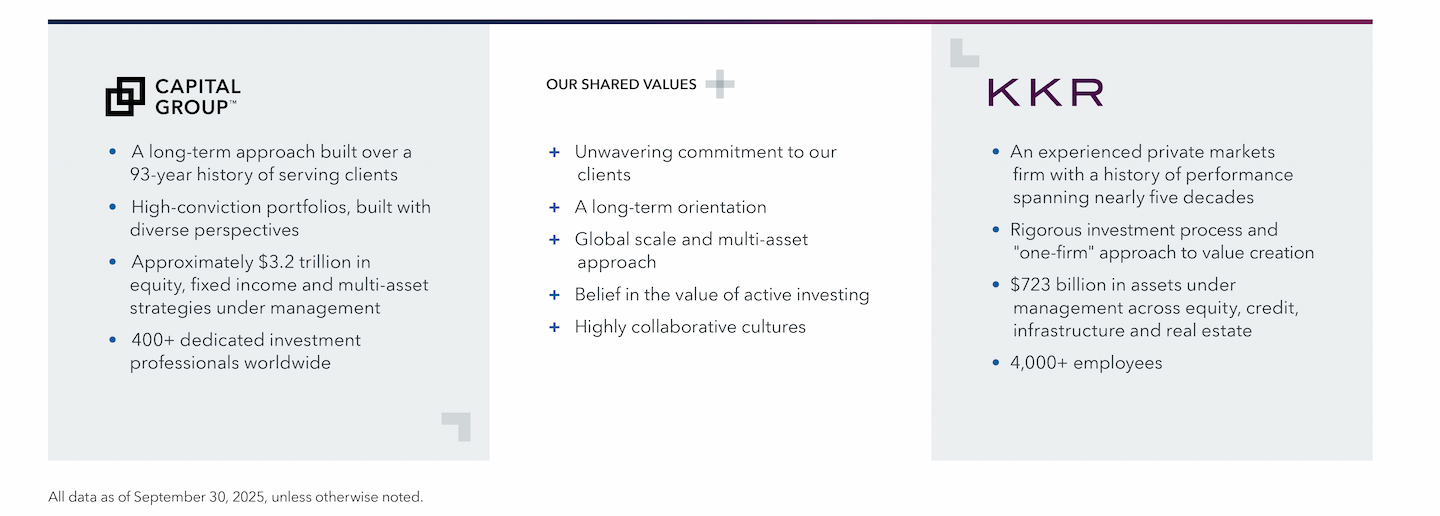

What makes a successful partnership? Aligned goals, strategic vision, trust, transparency, complementary strengths and capabilities. Capital Group found all of that with KKR, and we’re excited to tell you about the Public-Private+ Solutions we’ve created and how it may help your clients.

We know that to be the partner of choice for our clients and shareholders, everything we do needs to be in their best interest. That means ensuring their portfolios, whether on the public or the private side, are being sourced, overseen, underwritten and risk managed.

We wanted to partner with somebody who was as good with private markets as we are with public markets. KKR was the natural fit. They're one of the most recognized leaders in multiple areas of private markets.

Private credit, real estate, private equity. It takes that kind of breadth to really bring the best thinking to bear for our clients’ portfolios. KKR has decades of experience in private markets, hundreds of billions in assets under management and investments across the world. That level of knowledge and familiarity with the marketplace is hard to replicate.

KKR and Capital are also culturally aligned. If we think about our mission statement and our five core values, they’re very similar. KKR believes strongly in investing alongside their clients, focusing on long-term strategies and making every effort to ensure the best outcome. That's certainly the way we've always thought about investing.

Historically, private markets have been inaccessible to many investors. We believe in broadening opportunities for our clients and this partnership allows us to do that. By combining private market assets with public markets, we’re able to lower some of the barriers to entry.

Illiquidity, complexity and high investment minimums have all traditionally been seen as hurdles. The specific products we’ve built together are designed to mitigate some of those concerns.

Our goal has always been to help improve people’s lives through successful investing. In KKR, we’ve found a partner who is not only aligned with that mission, but who has the resources, the knowledge and the skills to help us see it through.

[upbeat music]