The recent U.S. intervention in Venezuela has raised major questions in the oil market. With the future governance of the country still largely uncertain, will more Venezuelan oil eventually come online? If so, how long will that take, who will manage the process and how will these dynamics affect short- and long-term oil prices? More specifically, what impact will these factors have on oil bonds across the delivery chain?

At about 300 billion barrels, Venezuela’s proven oil reserves are the largest on earth. For reference, its oil production peaked at about 3.5 million barrels per day (BPD) in the late 1990s before sliding to about 900,000 BPD today. Although its delivery chain infrastructure now appears to be in very poor shape, we think it’s likely that an additional few hundred thousand BPD of Venezuelan oil will come to market over the next several months. If the country eventually benefits from sanctions relief, the return of diluent supply1, pipeline repairs and power restoration, this figure may increase to 300,000 to 500,000 BPD over the next 12 to 18 months.

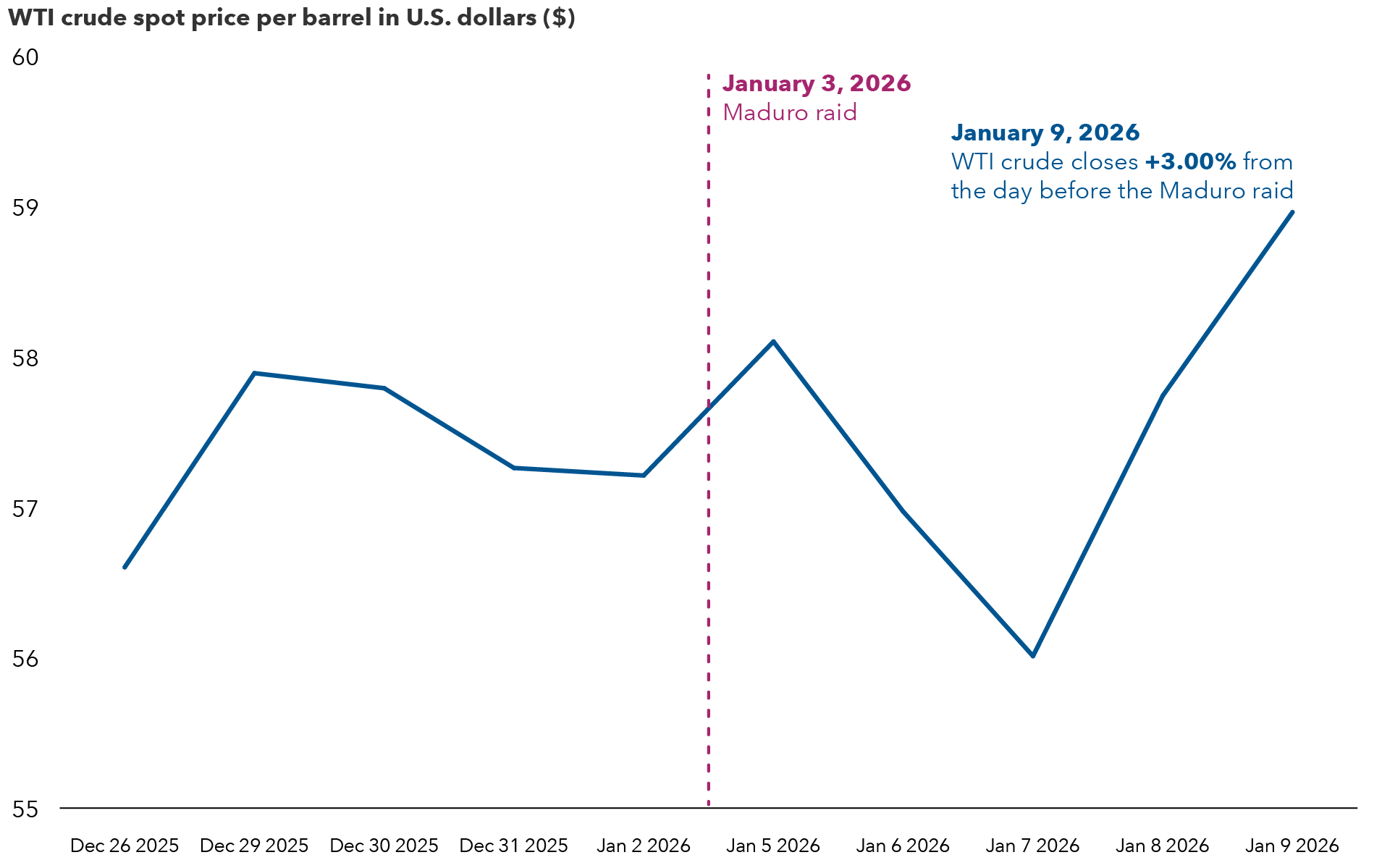

However, adding more than one million BPD of new production may take years and tens of billions of dollars in new investments in infrastructure and other aspects of the delivery chain. This tension between the likely short- and long-term outcomes in Venezuela may account for why West Texas Intermediate (WTI) crude oil prices didn’t move significantly in the immediate aftermath of the U.S. raid to capture former president Nicolas Maduro and his wife on January 3.