What makes this current wave of mega IPOs unique is that some index providers have altered their inclusion rules to accommodate large IPOs to join more quickly, such as Nasdaq and Russell 1000.

Near-term, we expect SpaceX’s index inclusion will generate some sustained buying interest in the days following the company’s addition. At the same time, some existing index constituents may face modest selling pressure to create room for a new entrant. These effects are likely to be relatively mild and short-lived.

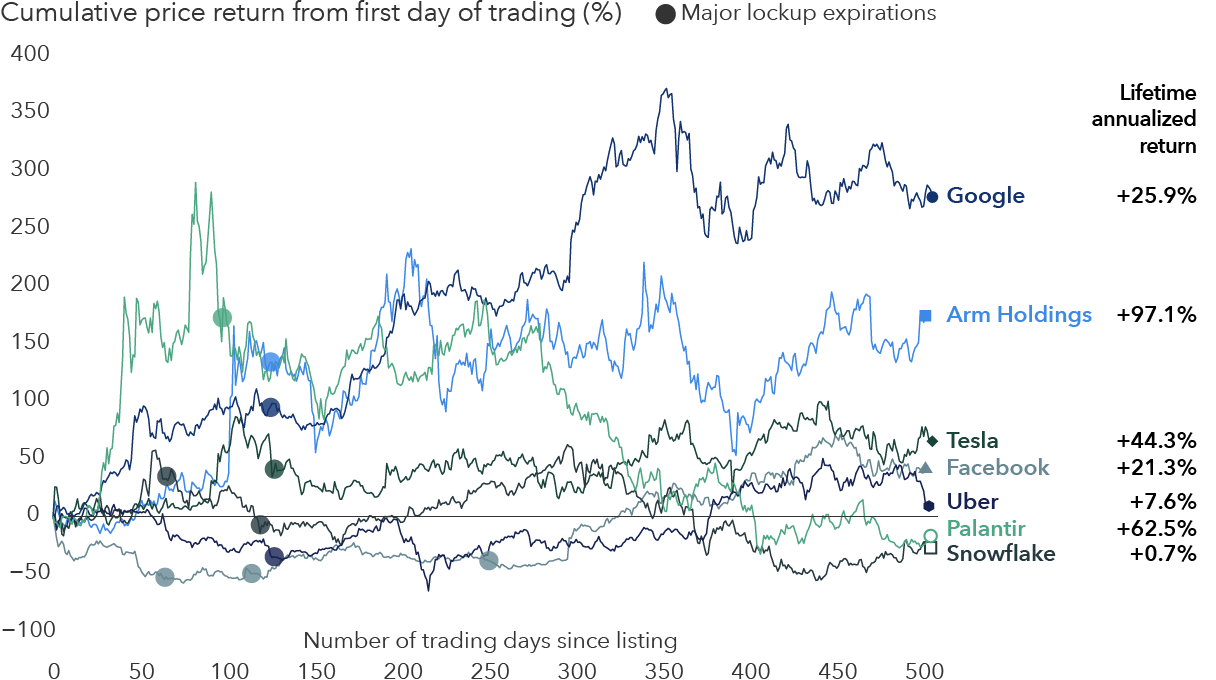

Evaluating a vast range of IPOs relies on thorough research that assesses the long-term fundamental case for a stock affecting various industries. That framework does not change because an index does.

The AI boom has generated widespread retail and institutional interest, which is expected to increase further as large IPOs come to market. At the same time, companies have experienced rapid valuation gains, bringing market concentration into sharper focus. While the long-term earnings trajectory remains uncertain, periods of valuation adjustment and volatility are a natural part of aligning expectations with realized outcomes.

AI can support long-term return potential and represent a credible allocation within portfolios. However, exposure should be balanced, with no single theme dominating overall risk.

Recent dispersion within the Magnificent Seven highlights this dynamic. Despite strong interest in AI, stock performance has diverged this year, reinforcing the need for selective exposure, particularly as new IPOs come to market.