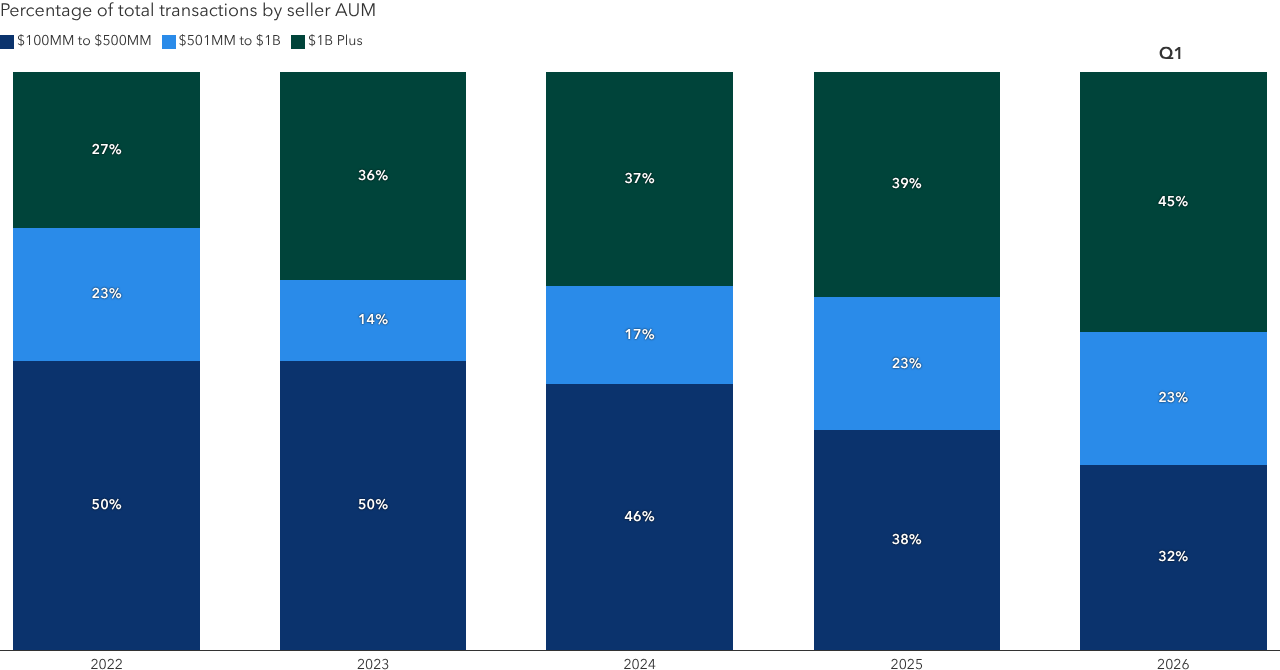

Judging by recent mergers and acquisitions (M&A) activity, it seems founders of registered investment advisory (RIA) firms have more opportunities than ever to sell externally. DeVoe & Company’s first-quarter Deal Book shows that 2026 is off to the fastest start of any year on record — building on the record-breaking deal volume of 2025. New private equity (PE) capital keeps flowing into RIAs, lured by the recurring revenue streams and high margins that often characterize the independent wealth management industry.

Yet for most sellers, the market has rarely been more exacting.

Private equity-backed RIAs and a growing cohort of PE minority investors are competing fiercely for prime acquisitions. But size alone is no longer enough to generate interest from PE-backed buyers paying the highest valuations — usually expressed as a multiple of a firm’s earnings before interest, taxes, depreciation and amortization (EBITDA). After a decade of bulking up, these buyers tend to be hyper-focused on bolstering the durability and organic growth of their platforms, rather than simply aggregating assets.