Advisors and registered investment advisor (RIA) firms across the U.S. are navigating one of the most dynamic and challenging periods the wealth management industry has seen in decades.

Macro forces — namely the expected transfer of over $80T of assets1 to younger generations, as well as private equity-fueled RIA industry consolidation — are reshaping the competitive landscape.

Today, 77% of RIA assets are held by just 7% of firms, according to Stephen Caruso, associate director of wealth management and lead RIA analyst at Cerulli Associates. These RIAs, each managing at least $1B in assets, are increasingly dominated by a handful of “mega RIAs” with over $50B in AUM, he says. And those with $5B or more are growing faster and attracting more talent than any other segment in the industry.

However, their dominant AUM share is largely because of acquisitions and market appreciation, according to Cerulli. Antonio Bass, senior vice president and enterprise growth manager at Capital Group, believes that many of the largest firms must also confront the same chronic challenges facing all advisors in the year ahead: Stagnant organic growth and a shortage of next-generation talent willing to prospect for new clients.

“If you can’t demonstrate organic growth, your valuation will suffer in the mergers and acquisitions (M&A) market — and acquirers may not even consider you,” says Bass. “That’s a serious issue in an industry that is consolidating, where succession planning is limited, and where many firms are keeping their options open for mergers or external exits.”

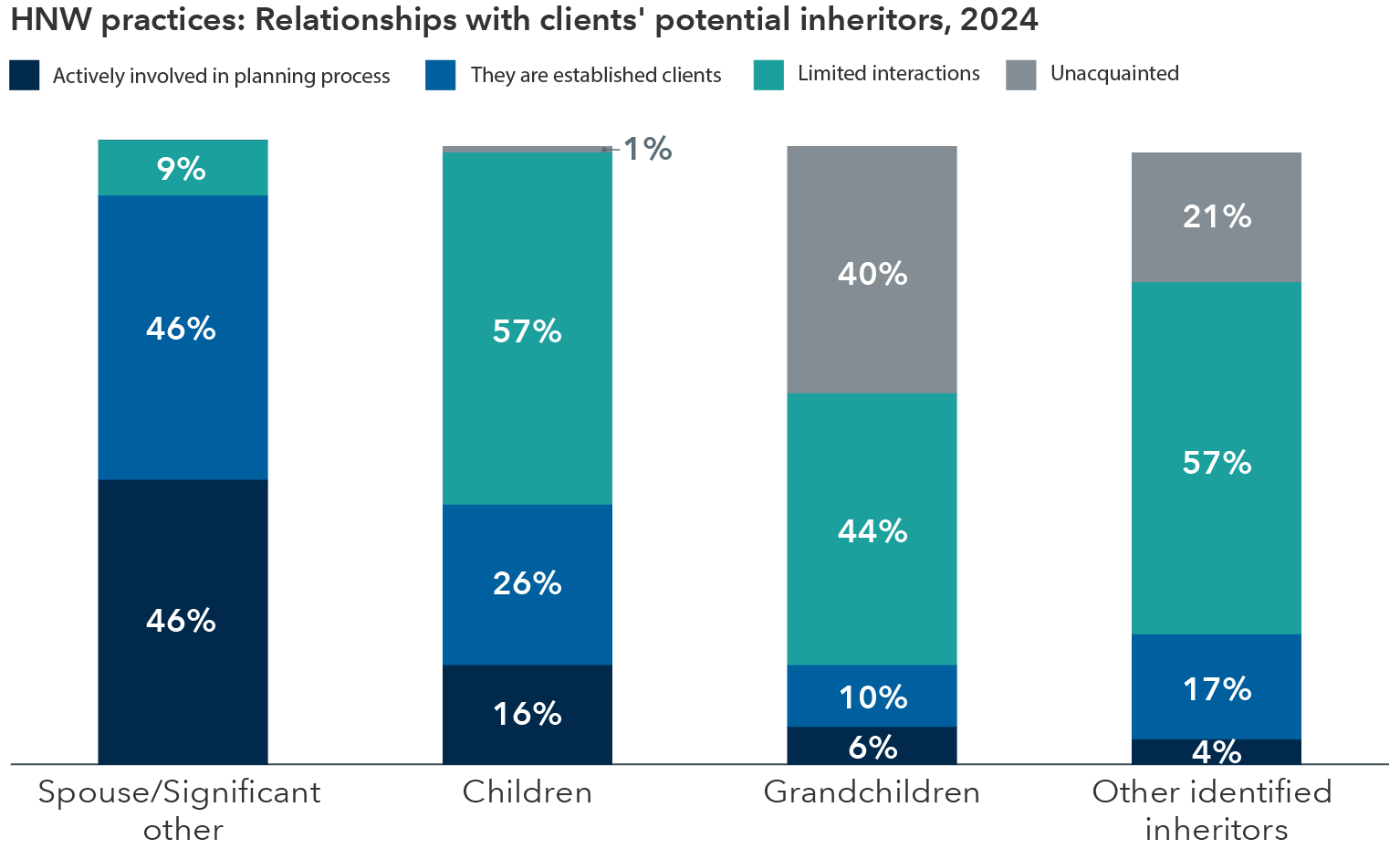

To understand what’s at stake and how firms can respond, examine these four key trends facing advisors and RIAs in the year ahead, starting with the root of all business: the client.