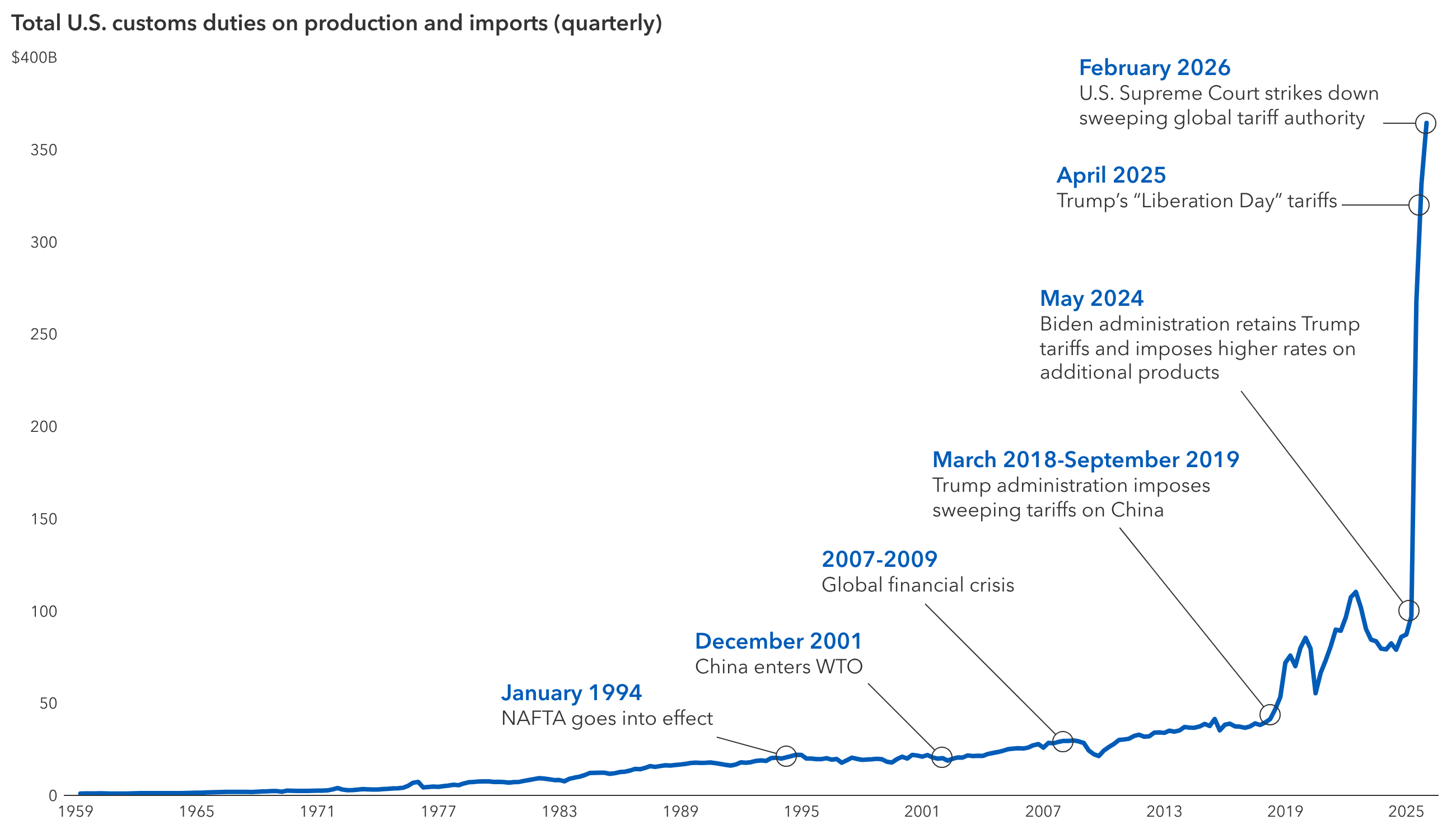

The U.S. Supreme Court has knocked down some of the pillars of President Trump’s global tariff structure, but over the next few months it is likely to be rebuilt. The wall will simply have a different look, in my view, as it is reconstructed with alternative materials.

The court on Friday struck down all the tariffs Trump implemented under the International Emergency Economic Powers Act (IEEPA), including the so-called “Liberation Day” tariffs. While that decision was undoubtedly a major setback for the White House, the administration retains several alternative and far more legally durable statutory authorities through which it can reestablish most of the existing tariffs.

The president immediately announced his intention to begin using those authorities. The first step is a 15% blanket global tariff to be imposed for the next five months under Section 122 of the Trade Act of 1974. This tariff will serve as a temporary placeholder, ensuring that revenue continues to flow while giving the Office of the U.S. Trade Representative time to pursue a series of country-by-country investigations under Section 301 of the act, addressing alleged unfair trade practices.