Everyone seems to want to help workers save for retirement. Employers encourage participants to use automatic payroll deductions to save as much as they can. Investment managers and the financial media stress the importance of retirement planning. The government has created a whole set of tools – from auto-enrollment to default investments – to increase the nation’s retirement plan savings.

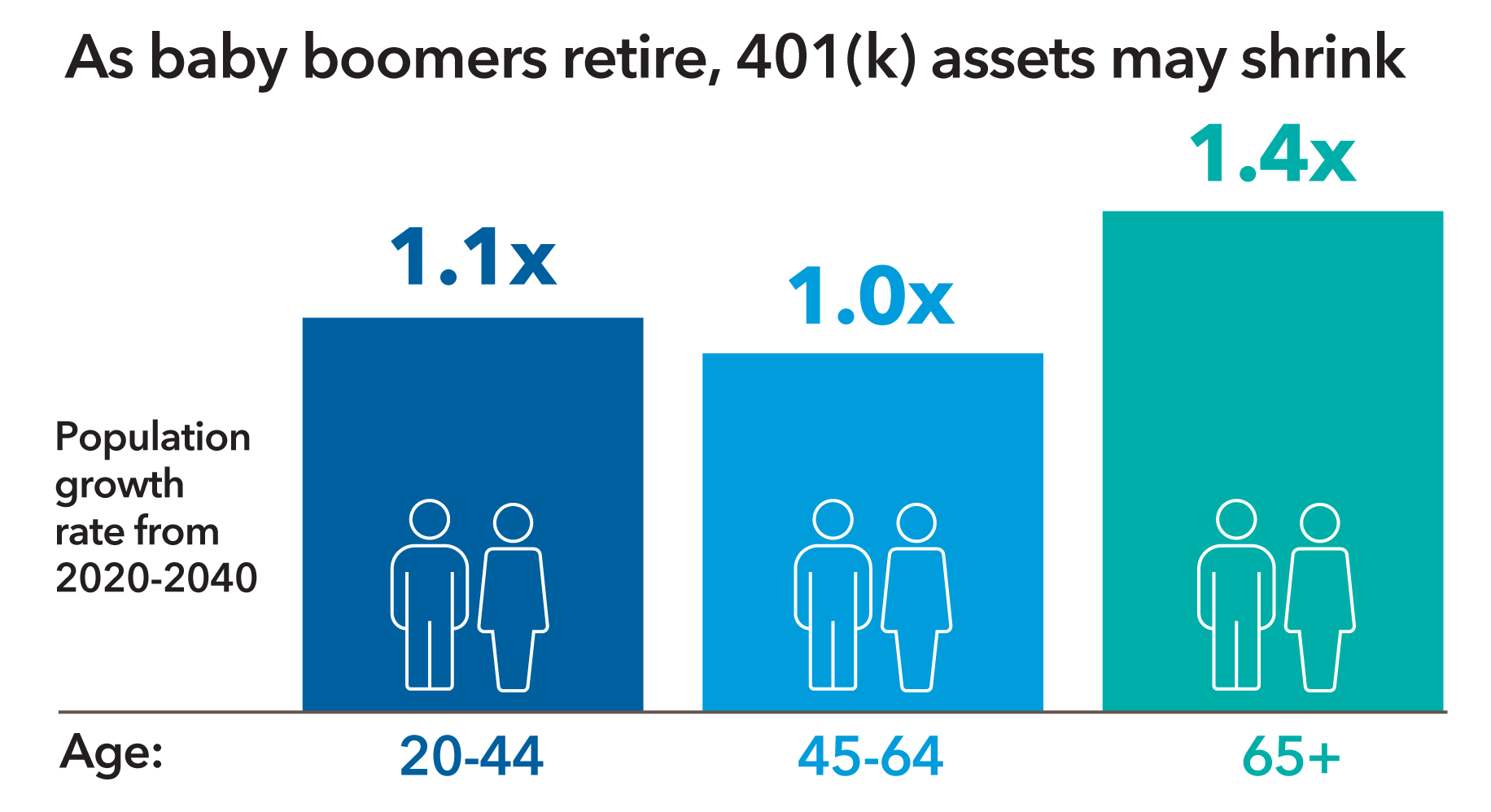

Far less attention is paid to what happens when people actually retire. How do they draw out their funds? What investment changes should they make?

Today, retirees are often on their own to answer these questions – but that could be changing. Both employers and employees are starting to see the value of keeping participants in the plan after they retire.