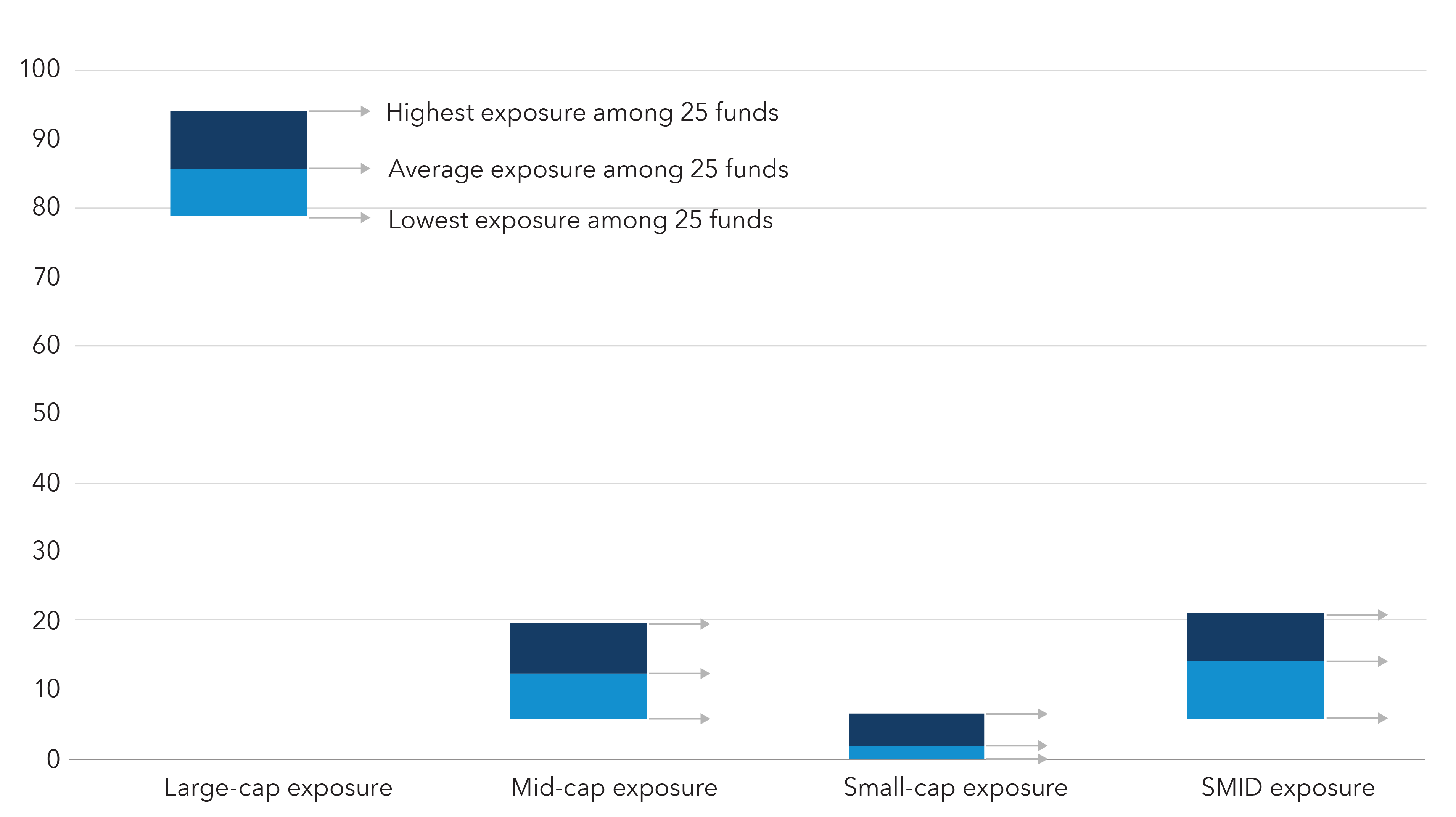

Small- and mid-cap stocks (SMID) can be a valuable part of a portfolio, offering the opportunity for enhanced return and diversification. But it's important to carefully size SMID exposure in a portfolio because the asset classes may have higher volatility. In our reviews of advisor portfolios, we have found that SMID exposure can pop up in unexpected places — creating an unintended level of risk.

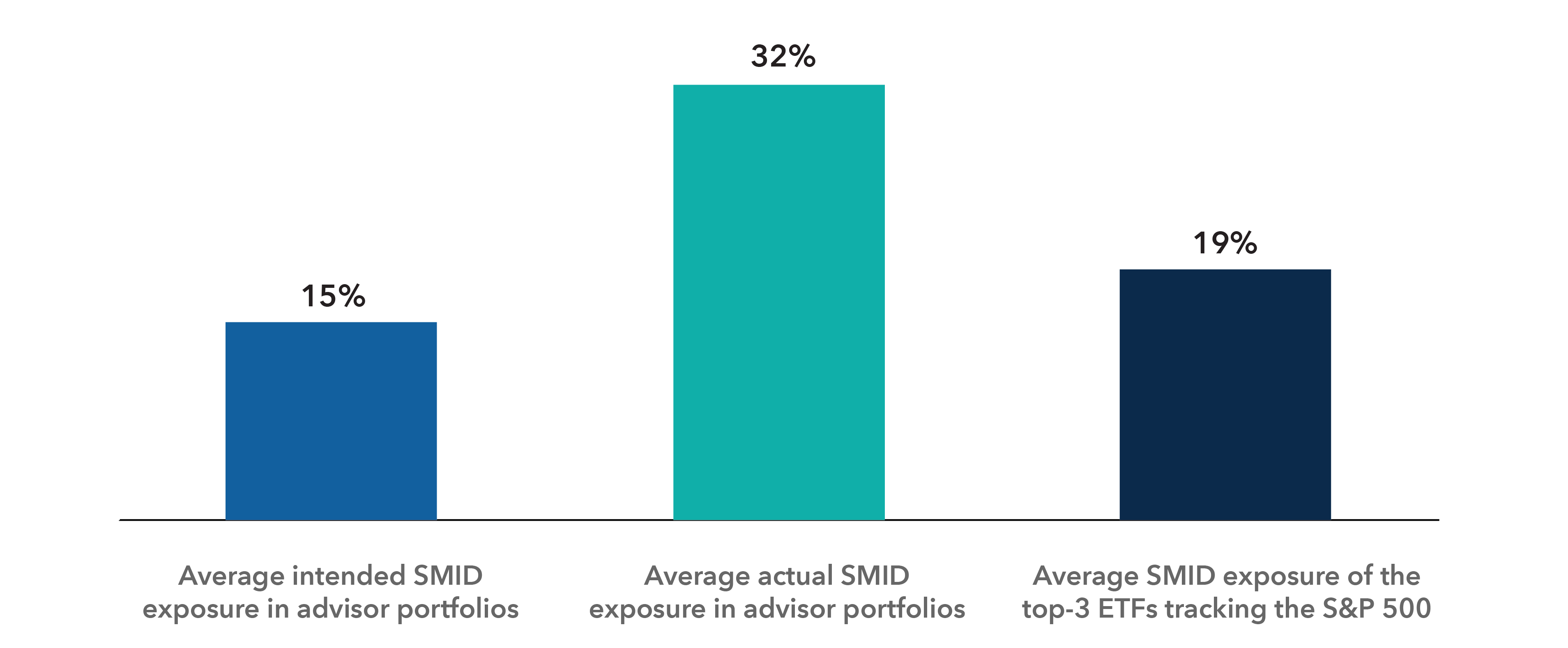

This year alone, more than 1,755 financial professionals have asked Capital Group to analyze their portfolios and provide suggestions on how allocations can help meet their clients’ financial objectives. During these reviews, we have found that many portfolios contain more exposure to SMID stocks than advisors intended. The average advisor portfolio we examined allocated 15% of its equity to SMID-dedicated strategies. But after we accounted for SMID exposure elsewhere in the portfolio, the actual average SMID exposure was more than double that — around 32% of the portfolio.

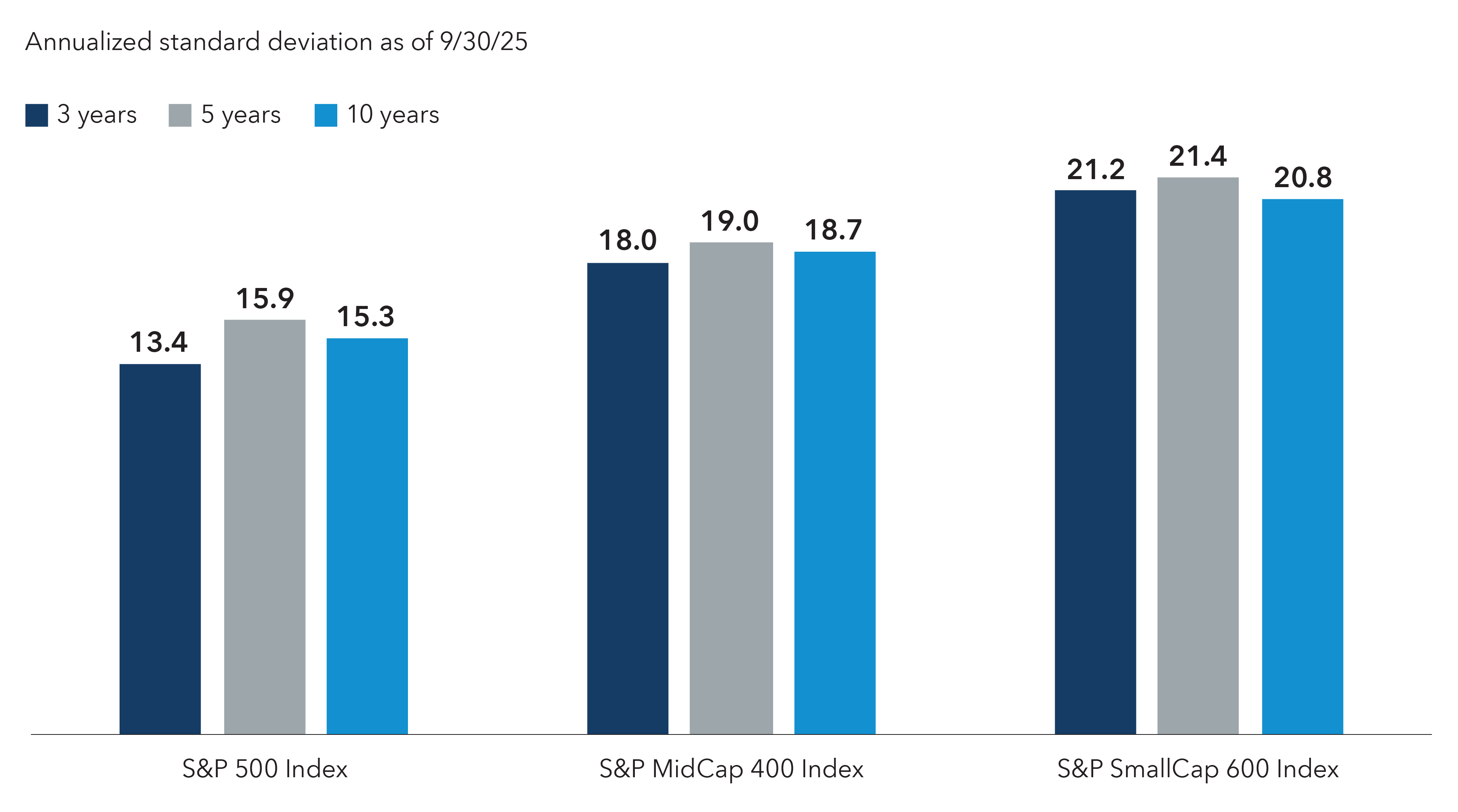

Why is that important? Small- and mid-cap equities can play a key role in a portfolio, providing diversification, growth potential and exposure to younger companies with more innovative products and business models. However, SMID stocks may also be more volatile and less liquid than their large-cap counterparts. Because of this, financial professionals need to ensure a portfolio’s SMID exposure is sized appropriately for the investor’s objectives and risk tolerance. While there is no single “right” level of SMID in a portfolio, it’s vital that financial professionals know what they own and be deliberate about SMID exposure.