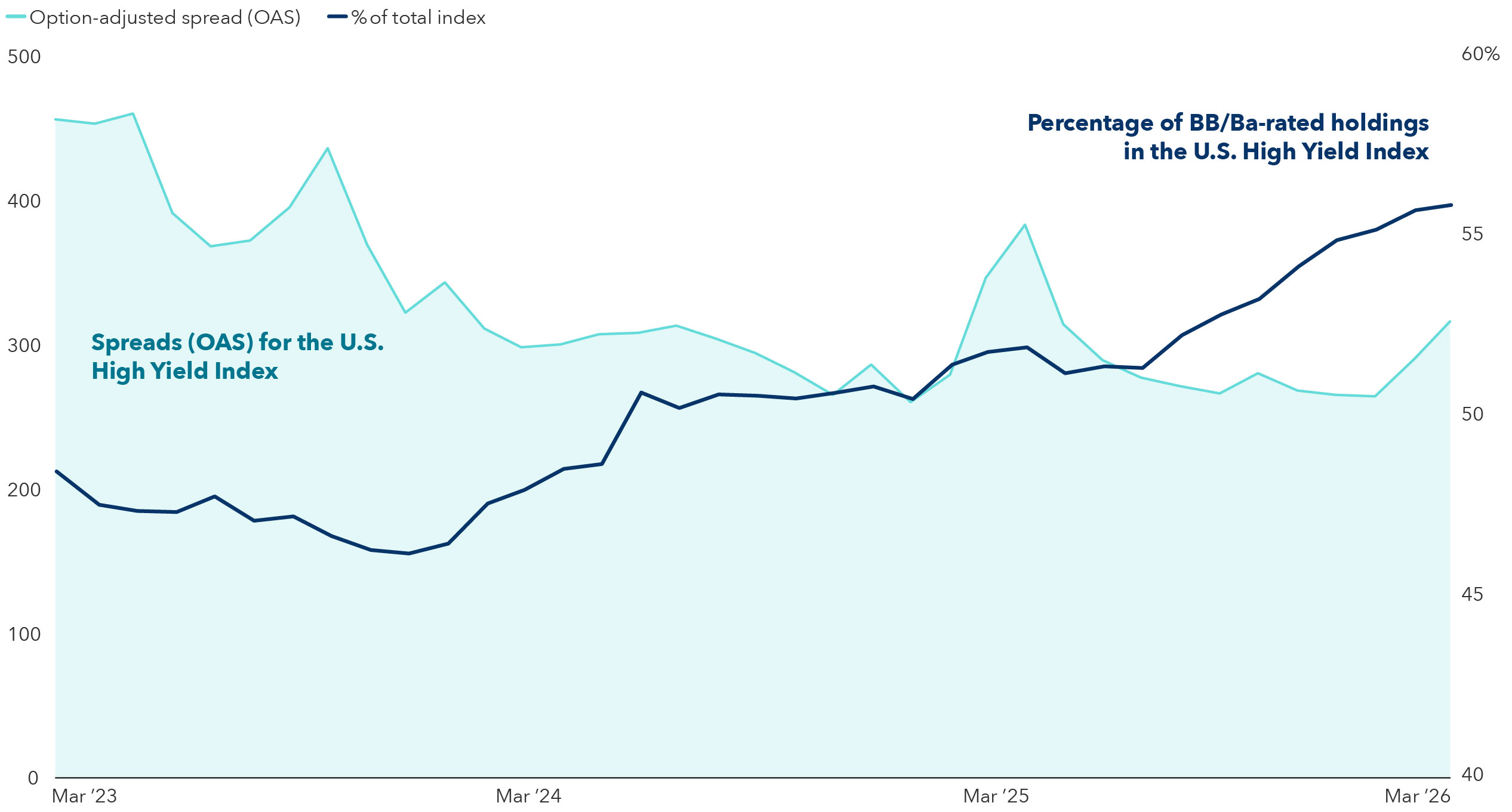

The historically tight high-yield bond spreads seen in the past few years may seem like a red flag to investors worried about volatility. After all, if difference between the risk-free rate and yield earned due to credit and other risks shrinks, that means less risk premium paid. But what if tighter spreads signal a green flag? The high-yield bond universe has evolved materially since before the 2008 global financial crisis (GFC) and in the years surrounding the pandemic.

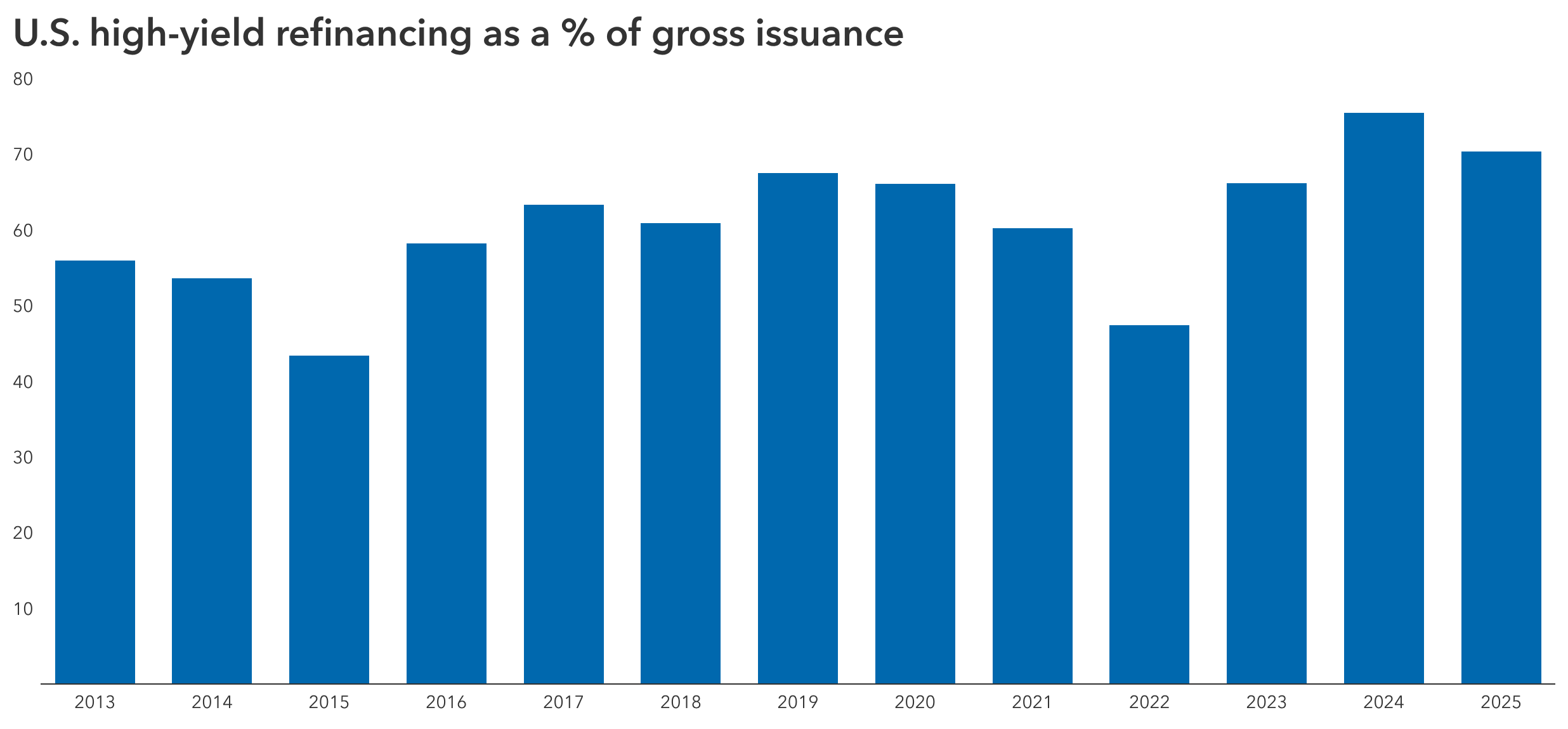

Today’s spread levels reflect a changed high-yield market. Several trends have fundamentally altered the market’s risk profile, including improvements in average credit quality, an issuance cycle dominated by refinancing and the migration of incremental risk to loans and private credit. Moreover, the rise of secured high yield, the sector’s shorter duration and more flexible call structures further challenge traditional assumptions. Together these comparisons provide a clearer framework for evaluating high yield today.