The market’s first instinct when oil prices rise and geopolitics deteriorate is usually straightforward: higher inflation should mean higher yields. That reaction is understandable, especially after the inflation shock of 2022. The more important question for bond investors is whether an energy spike creates lasting, broad-based inflation pressure or instead acts as a tax on households and businesses, weakening growth even as headline prices rise.

Our latest work on U.S. rates suggests that the second possibility deserves more attention. We believe the current backdrop looks less like a replay of 2022 and more like a classic stagflation scare: Inflation risk remains visible, but growth becomes the more important medium-term driver for fixed income.

Before the recent Iran conflict, the U.S. economy looked reasonably healthy. It was an economy with healthy growth, inflation that was moderating after tariff effects and a labor market that had already cooled materially below the surface.

That cooling is important because oil shocks do not hit a vacuum. When energy prices rise, headline inflation usually responds quickly, but the impact on core inflation (which strips out food and energy) is often more muted. By contrast, the hit to purchasing power can be immediate. Households pay more at the gas pump and have less room to spend elsewhere. Businesses face higher input costs. Financial conditions can tighten as risk appetite weakens. The result is a mix that can look inflationary in the near term while becoming more growth-negative over time.

The drag does not come only from oil itself. Tighter financial conditions, weaker investment and softer foreign growth are also meaningful. Investors should be careful about treating an energy shock as a simple “higher-for-longer” rates story.

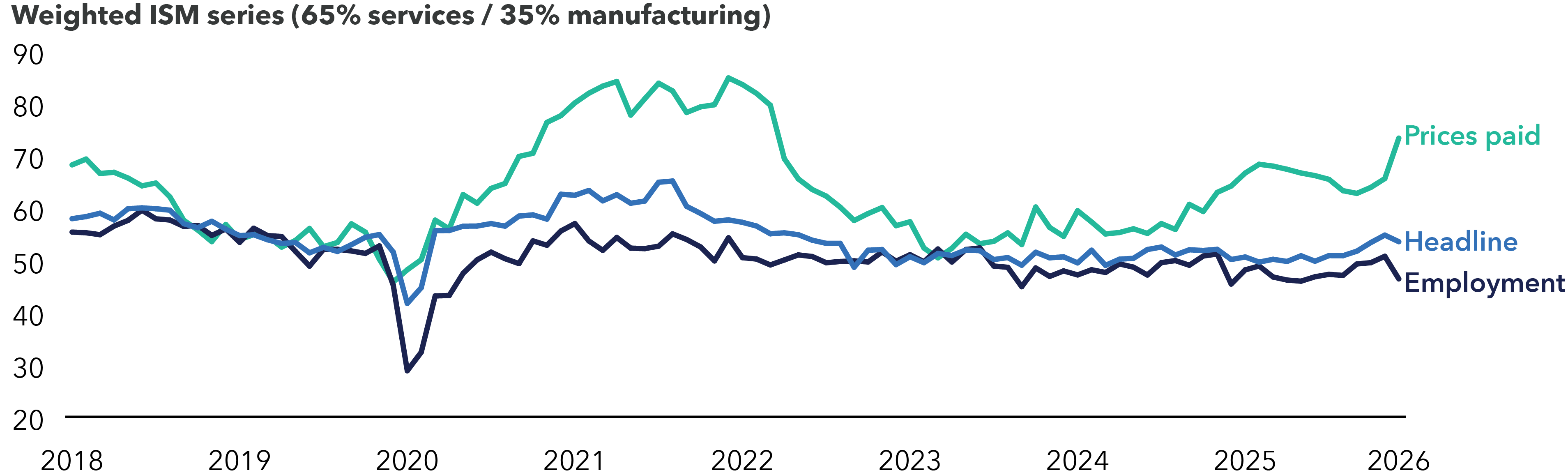

The data releases are also beginning to show prices paid by companies moved higher while employment components have weakened. Additionally, nominal consumer activity looks relatively firm while inflation-adjusted activity looks weaker. That divergence is important. It suggests the economy can appear resilient in dollar terms even as real demand softens. For bond markets, that usually argues against extrapolating higher nominal growth too far.