After more than a decade of growth style dominance and megacap‑driven returns, the U.S. equity market is changing — stretched valuations, widening dispersion and indexes increasingly reliant on a handful of companies. Beneath the surface, value investing is quietly regaining momentum.

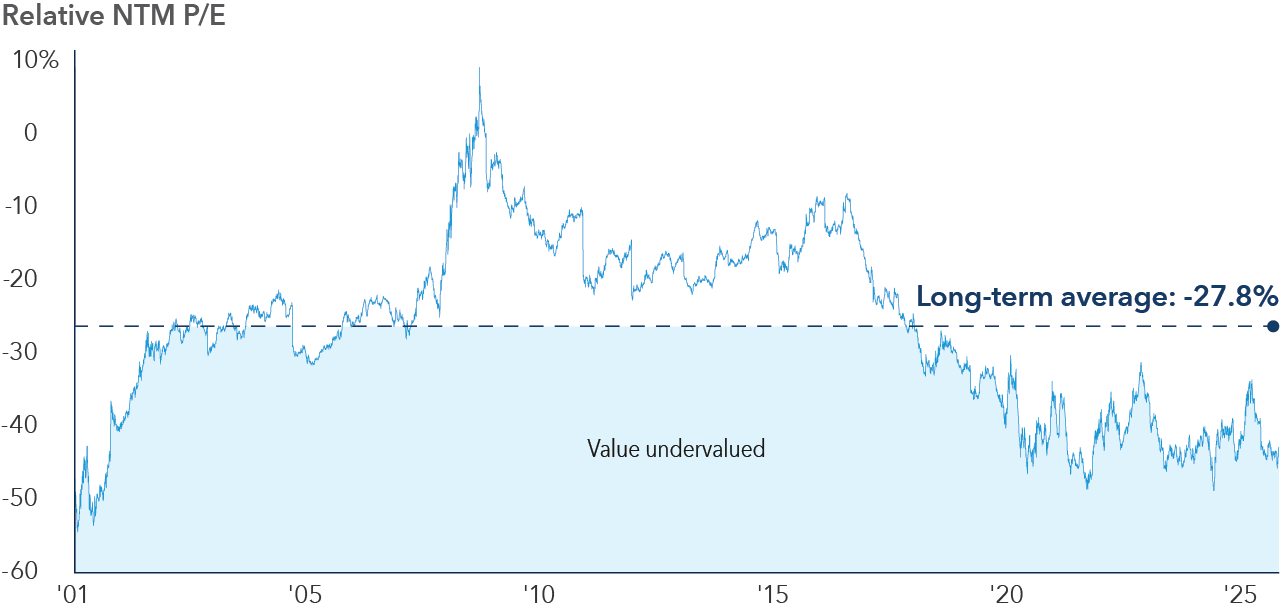

Recent performance underscores that shift. In the fourth quarter of 2025, the Russell 1000 Value Index outpaced its growth counterpart by 270 basis points (3.8% compared with 1.1%), cutting the Russell 1000 Growth Index’s full‑year advantage nearly in half. Valuations tell a similar story: While the S&P 500 Index cyclically adjusted price-to-earnings (CAPE) ratio nears 40 times earnings — levels historically linked to weaker forward returns — U.S. value equities continue to trade well below their average 27.8% discount to growth.