Interest Rates

Categories

Municipal Bonds

Muni mania: Why municipal bonds are breaking records in 2019

Mark Marinella

Mark Marinella

September 24, 2019

Municipal bonds have soared in popularity over the past year. A wave of investor money has flowed into the asset class — prompting some in the financial media to crown municipal bonds “2019’s hottest asset.”

Municipal bond funds raked in more investor money in the first four months of 2019 than they typically do in a “good“ year. And by mid-2019, year-to-date inflows had exceeded $45 billion — more than 10 times the amount of new investor money gathered over the whole of 2018.

In recent months, muni bond yields (which move inversely to bond prices) tumbled — setting records as trade tensions and faltering global growth bolstered the appeal of safe-haven assets.

Despite the asset class’s rising popularity, question marks hover over the market. Whether you’re new to the nearly $4 trillion municipal bond market — or are revisiting an existing tax-exempt bond allocation — here are answers to today’s key questions.

1. Following tax reform, are munis just for high net worth investors?

The asset class is certainly enjoying a season in the sun. And yet, despite increased demand, the myth that a permanent muni allocation only really makes sense for the very wealthiest persists.

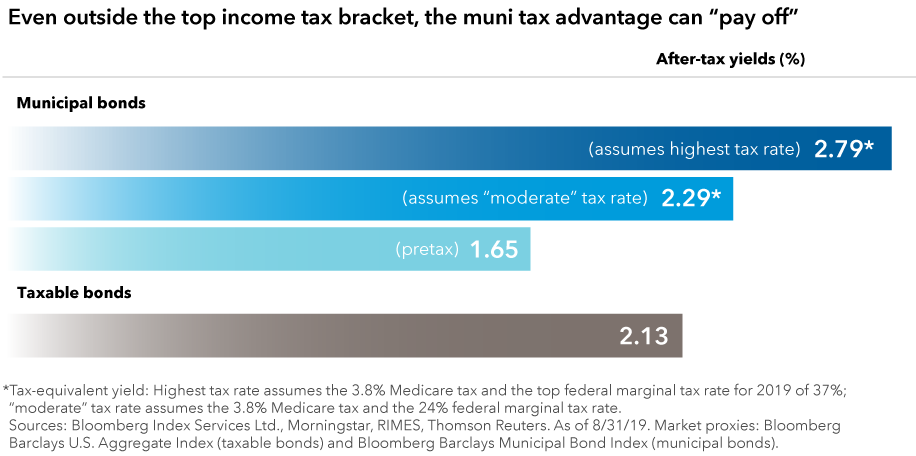

Truth is, this perception is seldom correct: Historically, munis have often been a relatively attractive source of after-tax income for any investor outside the lowest tax brackets.

What’s the current situation? Even with muni yields near multiyear lows, after-tax yields have continued to exceed those of taxable bonds for anyone whose marginal tax rate is 24% or higher — well below the top tax rate of 37%.

2. Where do municipal bonds fit in a portfolio?

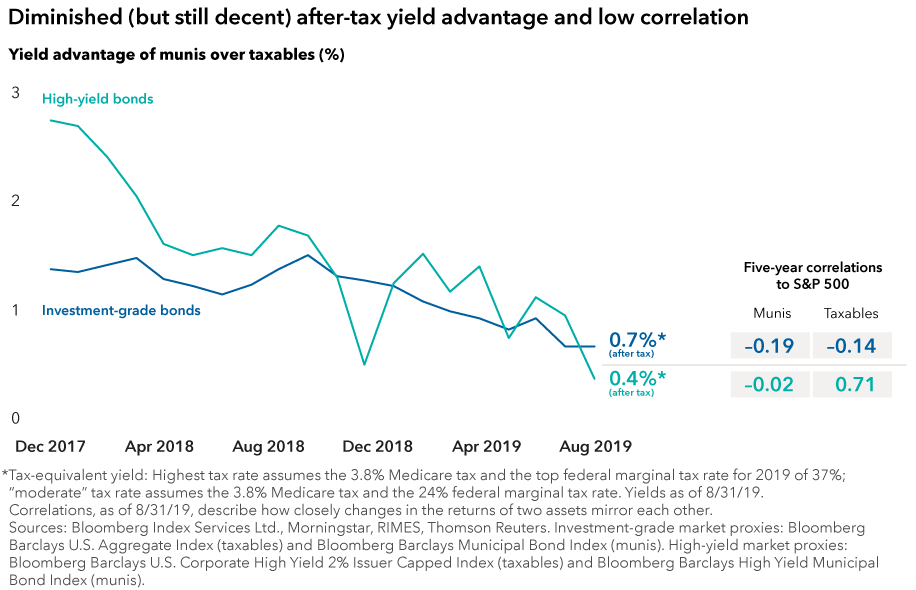

There’s no escaping it: The after-tax income offered by municipal bonds isn’t what it used to be. Strong investor demand at a time of relatively modest issuance has seen yields trend lower.

And yet, as discussed, the asset class remains a relatively attractive option for income seekers. In the past year or so, the yield advantage of municipals over taxables has mostly been greatest among high-yield bonds (for those willing to assume the increased risk associated with high-yield bonds) — averaging about 1.5 percentage points since tax reform was passed at the end of 2017.

In addition to income, municipal bonds can provide another potential benefit for balanced portfolios: equity diversification. Indeed, both investment-grade and high-yield municipals have often shown modest correlation to U.S. equities, an attribute that is especially attractive in unsettled times.

Munis can help balanced portfolios in three possible ways:

- If you’re looking to move cash off the sidelines. Cash gives investors liquidity and can also offer refuge amid volatility. But holding too much cash (or cash equivalents) can mean forgoing potential investment gains. As the Federal Reserve forges ahead with rate cuts, investors who feel it’s time to reallocate cash — and are comfortable taking on some investment risk — may view shorter term higher quality muni strategies as an attractive option.

- By upgrading your core bond allocation. Higher quality munis can provide ballast in an equity-heavy portfolio, serving three of the four roles of fixed income — income, equity diversification and capital preservation.

- By diversifying portfolio income. High-yield corporates are a popular portfolio choice for greater income (for investors willing to assume the higher risk, compared to investment-grade debt, of those investments). However, they aren’t a good diversifier because they have tended to rise and fall with equities. Complementing traditional high yield with comparably rated munis can be a double win for investors. Doing so offers a different source of higher income and, critically, can enhance equity diversification potential. That said, it’s worth noting that lower rated bonds can be quite volatile. Furthermore, the flipside of increased popularity is that lower muni yields provide less compensation for the risks entailed. These considerations underscore that it’s prudent to limit allocations to high-yield munis (and other riskier corners of the bond market).

3. Should I choose a state-specific or national municipal bond strategy?

How someone answers this question will hinge on their ZIP code as well as their financial circumstances. That said, the decision really does boil down to weighing the potential tradeoff between tax benefit and market opportunity.

In simple terms, residents of states with higher taxes stand to gain a greater tax advantage from strategies focused solely on in-state municipal bonds (because that investment income is typically exempt from state, as well as federal, income tax).

Assessing in-state muni opportunities is a little more involved. The market landscape varies from state to state as much as the actual terrain. California and New York, for example, each include diverse issuers and many thousands of municipal bonds. In contrast, the number of in-state bonds in less populous places may only amount to several hundred or fewer. Yields also vary quite meaningfully from state to state.

We put these considerations into a simplified framework, illustrated below. The conclusion is clear: State-specific strategies may offer some compelling potential advantages for residents of New York and California. Elsewhere, the potential tradeoff between tax benefit and market opportunity makes a strong argument for taking a closer look at national strategies.

4. With talk of recession growing louder, how safe are municipal bonds?

Recent market developments — including the inversion of the yield curve — have left some investors wondering if a recession is near. At times like these, it’s natural to revisit the level of risk in portfolios.

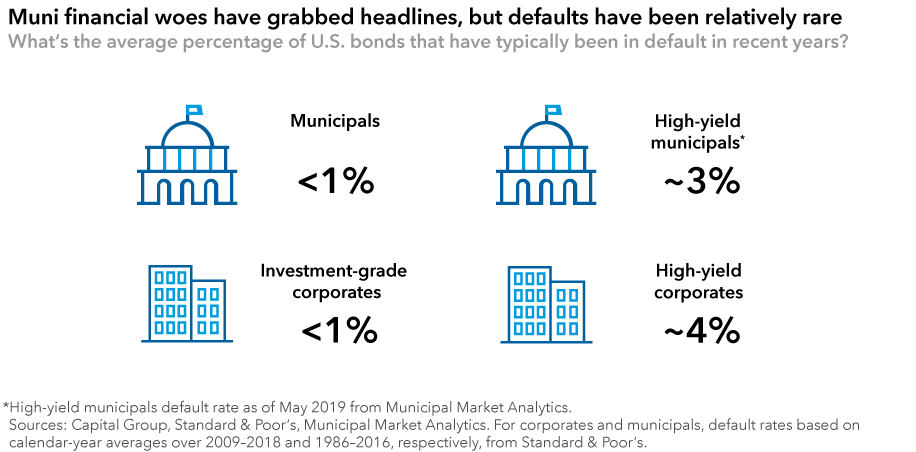

To the uninitiated, municipal bonds may seem like a risky asset class. After all, munis have often made headlines for the wrong reasons. Notable examples include Detroit’s 2013 bankruptcy and the debt crisis that erupted in Puerto Rico in 2015.

The facts, however, paint a different picture. In 2017, for example, Standard & Poor’s counted 64 defaults from U.S. companies and 20 from municipals. Recent history suggests that, over time, the percentage of rated municipal bonds that typically default is comparable to what has been observed among similarly rated U.S. corporates. Of course, default rates vary across market cycles. It’s also important to note: Historical data may underestimate actual default rates due to unrated bonds being excluded from the analysis.

5. What are the differences between general obligation and revenue bonds?

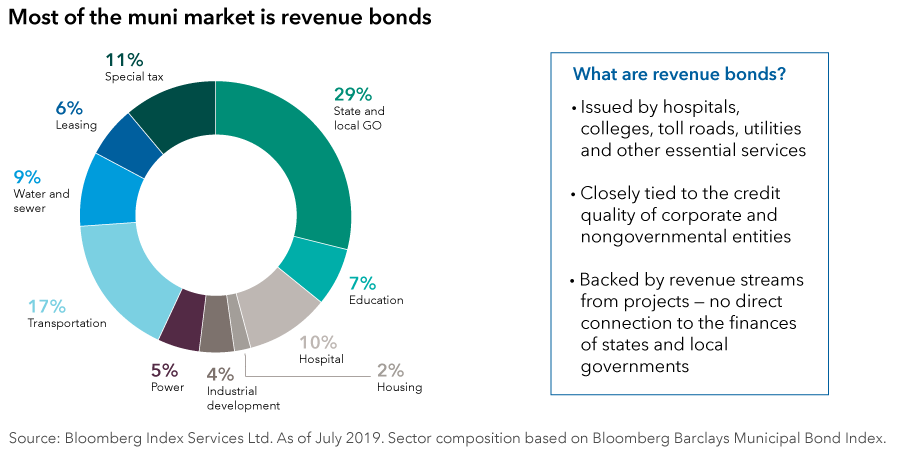

Often, when investors think about munis they have general obligation (GO) bonds in mind. By far, California and New York are the most frequent issuers of GOs. Typically, GOs are backed by the credit and taxing power of a state or local authority.

Some investors are, therefore, surprised to learn that most munis are revenue bonds, not GOs. Revenue bonds account for about 70% of investment-grade munis; hospitals, colleges and other providers of essential services issue these bonds. Each bond is backed by a dedicated revenue stream from a specific project, and therefore has very little connection to state and local government finances.

Fundamental research can provide a clear assessment of credit risk in revenue bonds, which have typically offered higher yields than GOs. In contrast, local government issuers face practical constraints on raising revenue. Politics and pensions are frequently significant factors. There can, therefore, be a lot more nuance and judgment involved in assessing whether GO bonds offer investors adequate compensation for the risks entailed.

Final thoughts

Municipal bonds can play an important role in the core and enhanced fixed income allocations of portfolios. Amid high valuations, emphasizing higher quality municipal bonds may make sense. Investors looking to add exposure may also want to consider waiting for market setbacks to offer more attractive entry points.

That being said, the municipal bond market is vast. With nearly $4 trillion in bonds outstanding, there will continue to be areas that are not as closely researched by investors.

“It’s a great time to be an active muni investor,” says Mark Marinella, a portfolio manager for several funds and separately managed accounts, including Limited Term Tax-Exempt Bond Fund of America® and The Tax-Exempt Fund of California®. “From the shape of the municipal bond yield curve, to opportunities in healthcare and relative value in housing sector munis, research is helping us uncover truly varied opportunities.”

Learn more about

Bloomberg Barclays Municipal Bond Index is a market value-weighted index designed to represent the long-term investment-grade tax-exempt bond market.

Bloomberg Barclays U.S. Aggregate Index represents the U.S. investment-grade fixed-rate bond market.

Bloomberg Barclays High Yield Municipal Bond Index is a market value-weighted index composed of municipal bonds rated below BBB/Baa.

Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index covers the universe of fixed-rate, non-investment-grade debt. The index limits the maximum exposure of any one issuer to 2%.

Bloomberg Barclays Source: Bloomberg Index Services Ltd.

Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

The S&P 500 is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2019 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

© 2019 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The indexes are unmanaged, and results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

The return of principal for bond funds and funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Lower rated bonds are subject to greater fluctuations in value and risk of loss of income and principal than higher rated bonds.

State-specific tax-exempt funds are more susceptible to factors adversely affecting issuers of their states' tax-exempt securities than more widely diversified municipal bond funds. Income from municipal bonds may be subject to state or local income taxes and/or the federal alternative minimum tax. Certain other income, as well as capital gain distributions, may be taxable.

Our latest insights

-

-

-

Municipal Bonds

-

Artificial Intelligence

-

Target Date

This is the headline for the Newsletter promo. Customize the message.

Related Insights

-

Asset Allocation

-

Global Equities

-

Tax & Estate Planning

Never miss an insight

The Capital Ideas newsletter delivers weekly investment insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

American Funds Distributors, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.