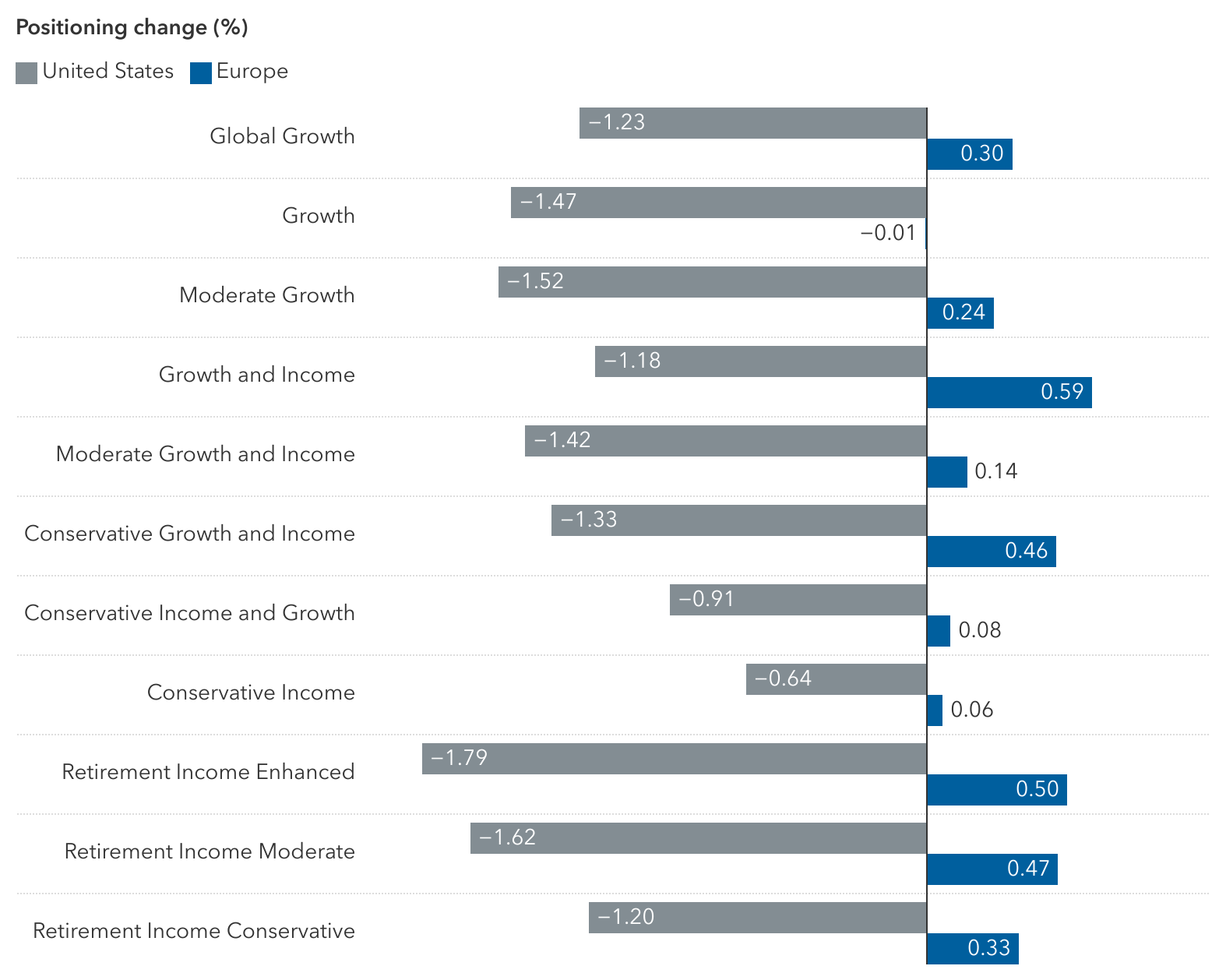

Facing volatility and uncertainty across the board — in financial markets, government policy and the direction of the economy — you may encounter a barrage of investor questions: What’s next for the markets? Will rates go up or down? Will tariffs spark inflation? A recession? How are my investments holding up? Do we need to make changes to my portfolio?

At the core, these questions go to managing risk and volatility. Capital Group’s Capital Solutions Group, which helps oversee $495 billion in multi-asset portfolios, takes an “always-on” approach to managing risk: it’s always a priority, whether markets are rallying, declining or fluctuating wildly. Capital Group's multi-asset portfolios include target date and college target date portfolio series, retirement income series and model portfolios.

“The most effective form of risk management is proactive – it’s always on, it’s embedded throughout the investment process and it’s not reactive,” says CSG’s Glenn Cagan. “Reacting to turbulent markets can lead to emotional decision-making and less than optimal long-term investment outcomes.”