Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility.

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

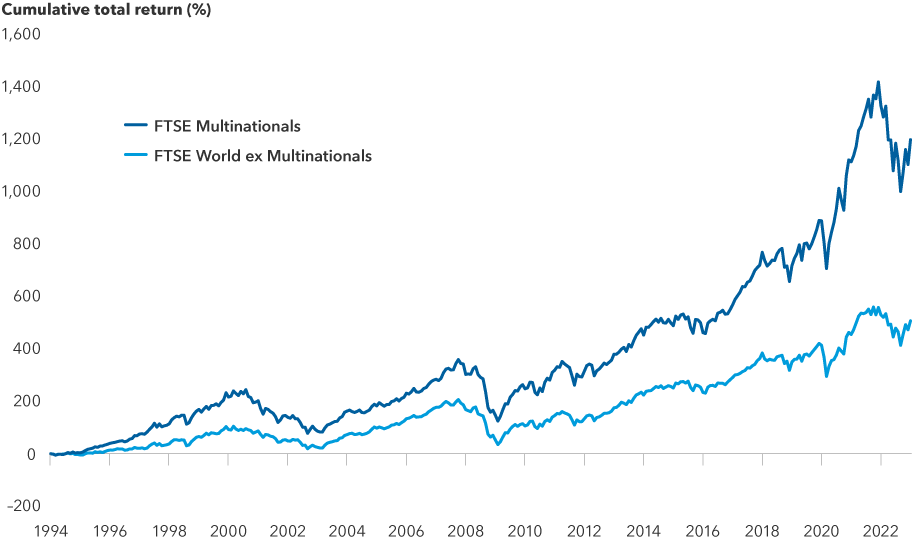

The FTSE Multinationals Index comprises companies which derive more than 30% of their revenue from outside their domestic region.

The FTSE World ex Multinationals Index comprises companies which derive 70% or more of their revenue from inside their domestic region.

MSCI Emerging Markets Investable Markets Index (IMI) is a free float-adjusted market capitalization-weighted index designed to measure results of the large-, mid- and small-capitalization segments of more than 20 emerging equity markets.

London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2023. FTSE Russell is a trading name of certain of the LSE Group companies. FTSE® and Russell® indexes are trademarks of the relevant LSE Group companies and are used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.