Americans are expected to live into their 80s and 90s, and yet, as noted by the American College of Financial Services, 52% do not consider just how long they may live when making savings and investment decisions. It is critical we help investors understand their life expectancy and the implications for retirement income planning. Although the uncertainty of longevity cannot be eliminated, we can plan and manage for it. Let’s discuss why longevity and life expectancy should be brought to the forefront of retirement income planning conversations.

April 21, 2026

KEY TAKEAWAYS

- Life expectancy trends and retirement savings are not well aligned.

- A simplistic approach to longevity planning may overlook a client’s health and lifestyle choices.

- Investors may need a more complete view of their life expectancy probabilities and the implications for retirement income planning.

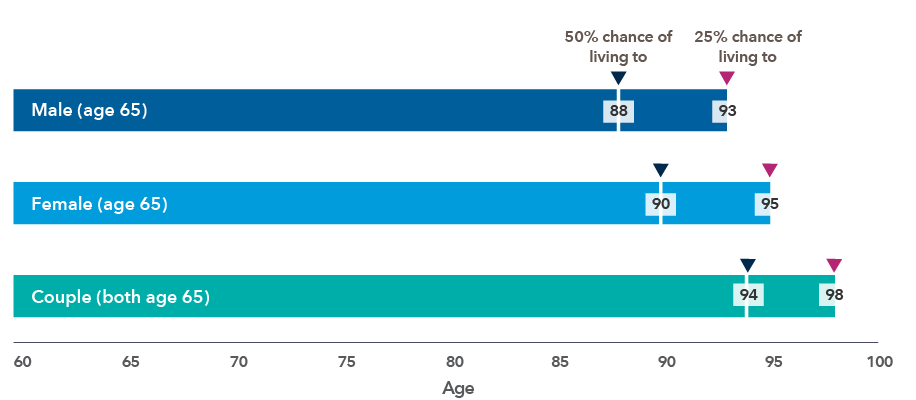

Life expectancy of a 65-year-old non-smoking married couple in excellent health

American Academy of Actuaries and Society of Actuaries, Actuaries Longevity Illustrator, www.longevityillustrator.org, (Accessed January 28, 2026.)

What is life expectancy?

While the term lifespan refers to the maximum number of years an individual can live, life expectancy refers to an estimate or an average number of years a person can expect to live. Life expectancy from birth tends to be the statistic we hear most often: A man or woman born in a certain year has an average life expectancy of X. This information has little relevance for someone reaching retirement age. For example, it makes no sense for a female who has reached age 84 to base her retirement-planning horizon using the Social Security Administration’s statistical average that, when she was born, predicted she would live around 80.1 years.

For the purposes of retirement income planning, a more relevant statistic is life expectancy at attained age. In fact, an 84-year-old non-smoking woman in excellent health has a 50% chance of living about eight years, as calculated by the American Academy of Actuaries and Society of Actuaries’ Longevity Illustrator. This same prediction indicates there is a 10% probability that she could live to 100. It also shows the median life expectancy probability (50%) for both males and females at age 65 is at least into their late 80s. And for couples, one spouse is expected to live into their mid-to-late 90s.

But this picture can also mislead planning for a retirement income horizon because these statistics are based on the median probability of the entire population. Many of your investors may have a survival probability that is much longer than the median, as there are large differences in life expectancy depending on various economic and demographic factors.

Planning horizon from attained age 65

Source: American Academy of Actuaries and Society of Actuaries, Actuaries Longevity Illustrator, www.longevityillustrator.org , (Accessed January 28, 2026.)

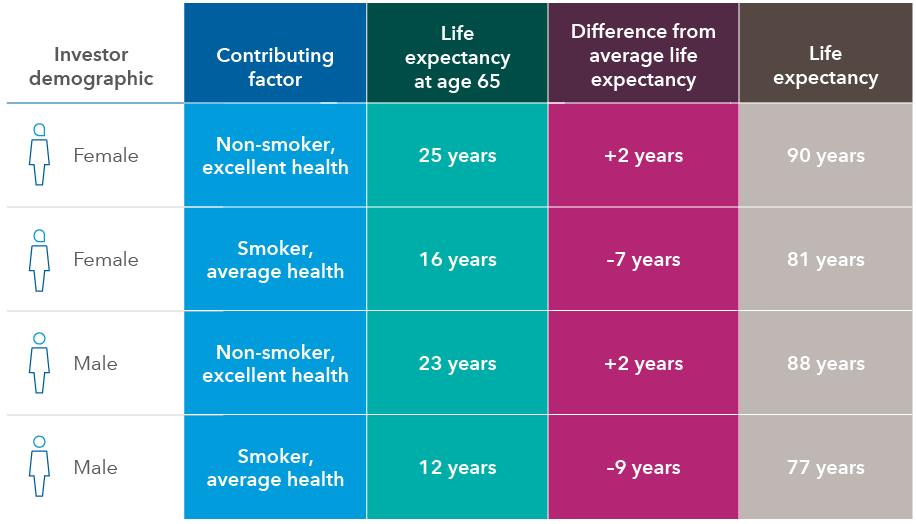

Contributing factors: OK if I smoke?

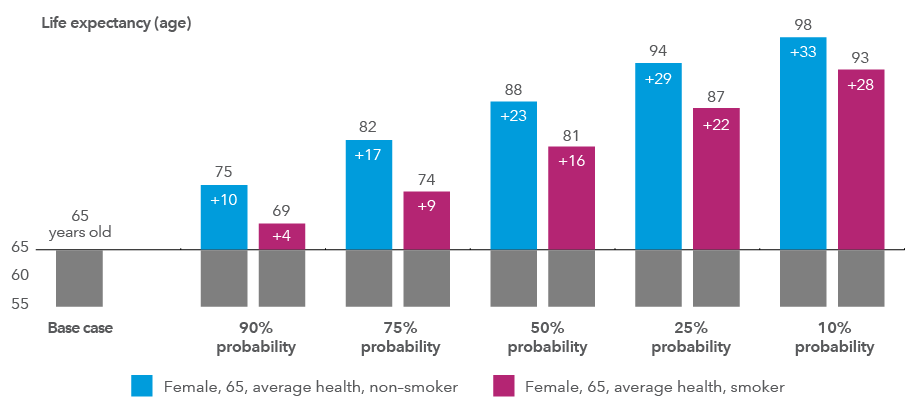

To provide more perspective for clients, consider utilizing individual mortality factors such as gender, smoking choices and general state of health to sharpen the life expectancy probability. This will help ensure the planning horizon matches up with their actual financial longevity risk and provide a more accurate picture of their retirement income horizon. For instance, suppose your investor is a 65-year-old woman who smokes and self-reports average health. Based on the Longevity Illustrator, she has a 50/50 chance of living at least another 16 years, to age 81, compared to age 90 if she were a non-smoker. But, as a smoker, she also has a 25% probability of living at least another 22 years to age 87. And if she were a non-smoker in average health, she would be likely to live another 29 years to age 94! This range illustrates the uncertainty surrounding how long someone might live; longevity shouldn’t be viewed as a single point in time. Underestimating life expectancy, together with having too short a planning horizon, can result in inadequate planning for retirement income needs.

Probability of living past age 65

Source: American Academy of Actuaries and Society of Actuaries, Actuaries Longevity Illustrator, www.longevityillustrator.org, (Accessed January 28, 2026.)

Reframing longevity with your clients

Although the uncertainty of how long someone may live cannot be eliminated, you can help investors better understand their own unique probabilities and develop plans to reduce the likelihood they will outlive their financial resources.

Kate Beattie is a senior retirement income strategist with 19 years of experience in the industry as of 12/31/2025. She holds a bachelor’s degree in economics with a business administration minor from Colorado State University. She also holds the Certified Financial Planner™ and Retirement Income Certified Professional® designations.