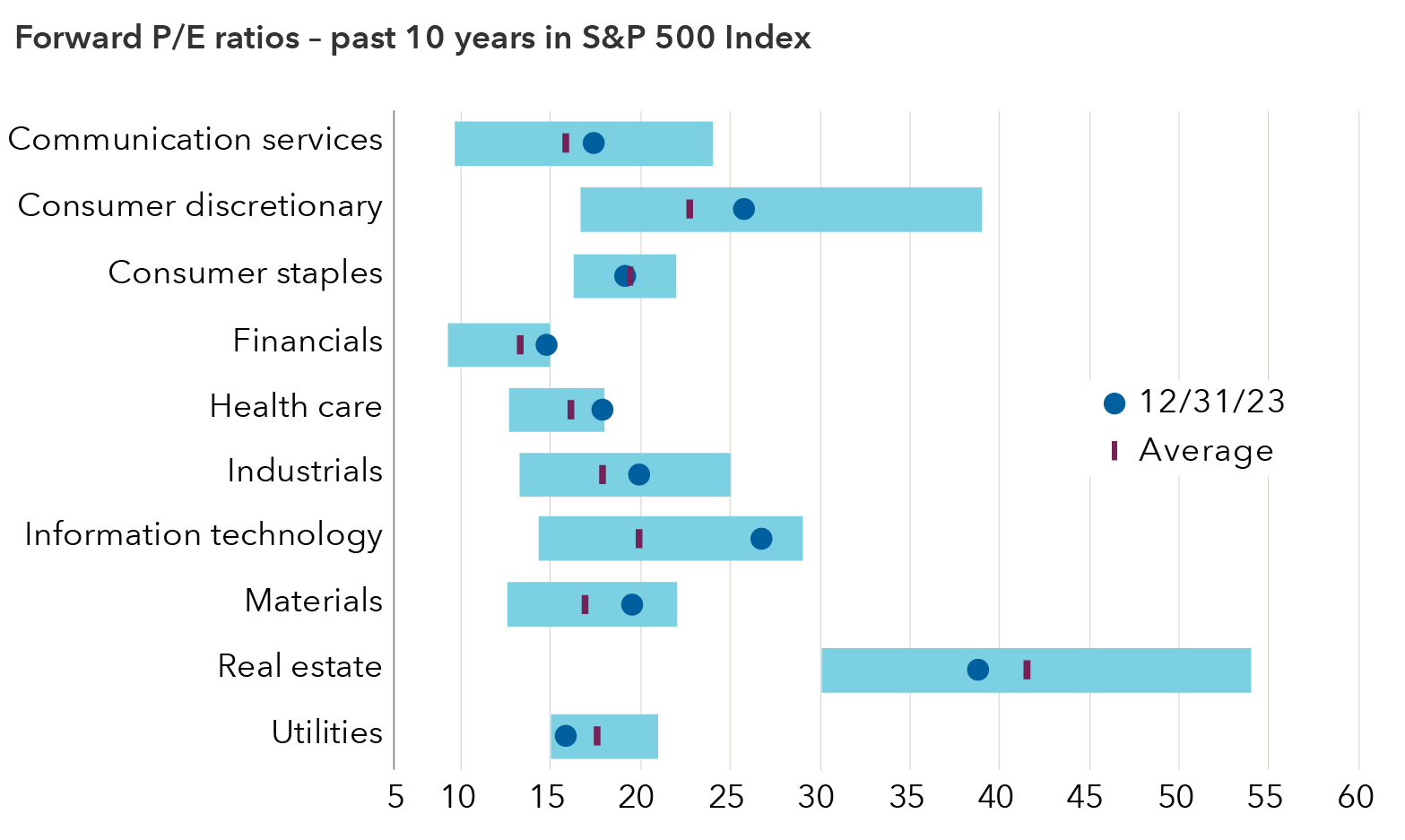

The S&P 500 Index is a market-capitalization-weighted index based on the results of approximately 500 widely held common stocks.

The S&P 500 Information Technology Index comprises those companies included in the S&P 500 that are classified as members of the GICS® information technology sector.

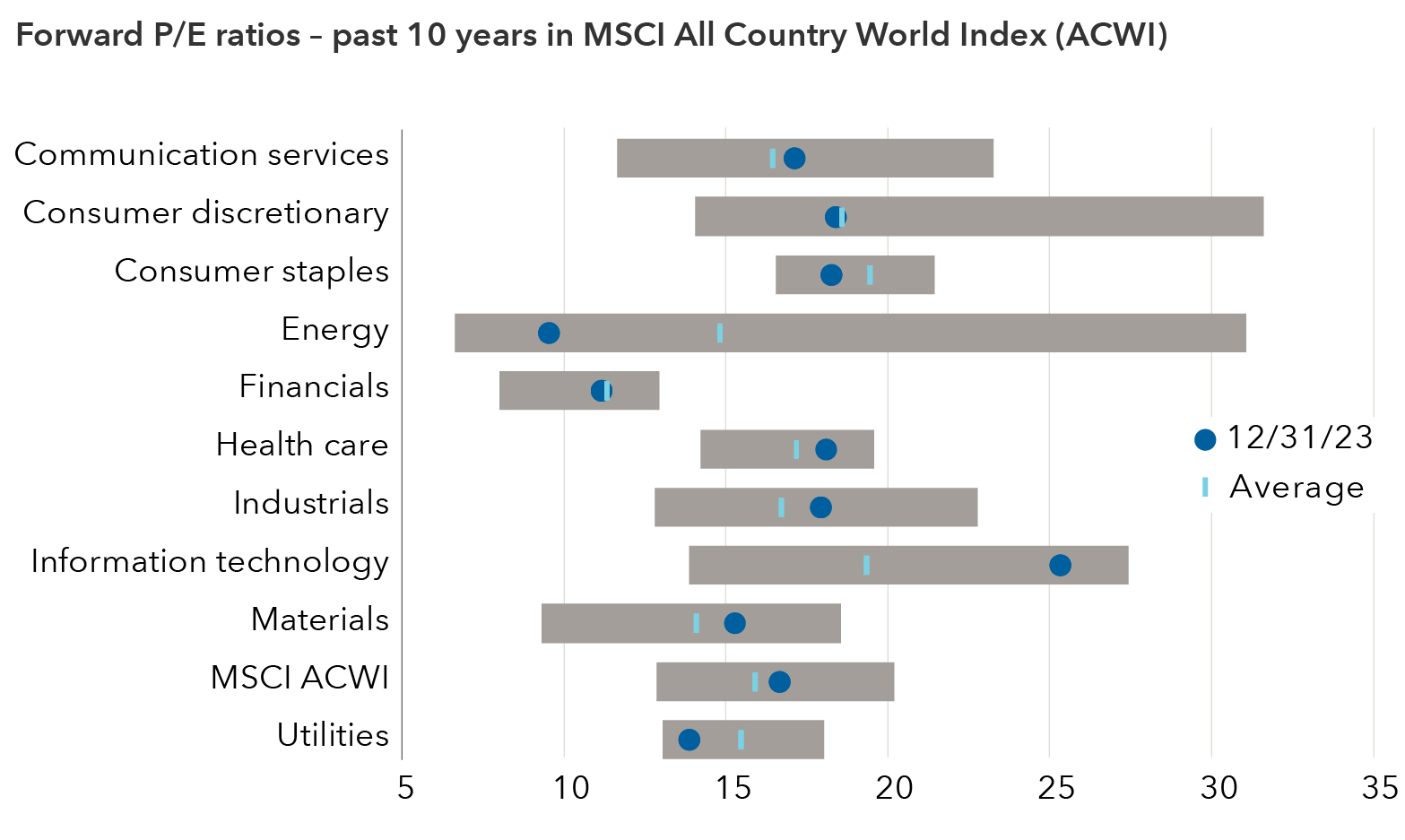

MSCI All Country World Index (ACWI) is a free-float-adjusted market-capitalization-weighted index that is designed to measure equity market results in the global developed and emerging markets, consisting of more than 40 developed and emerging market country indexes.

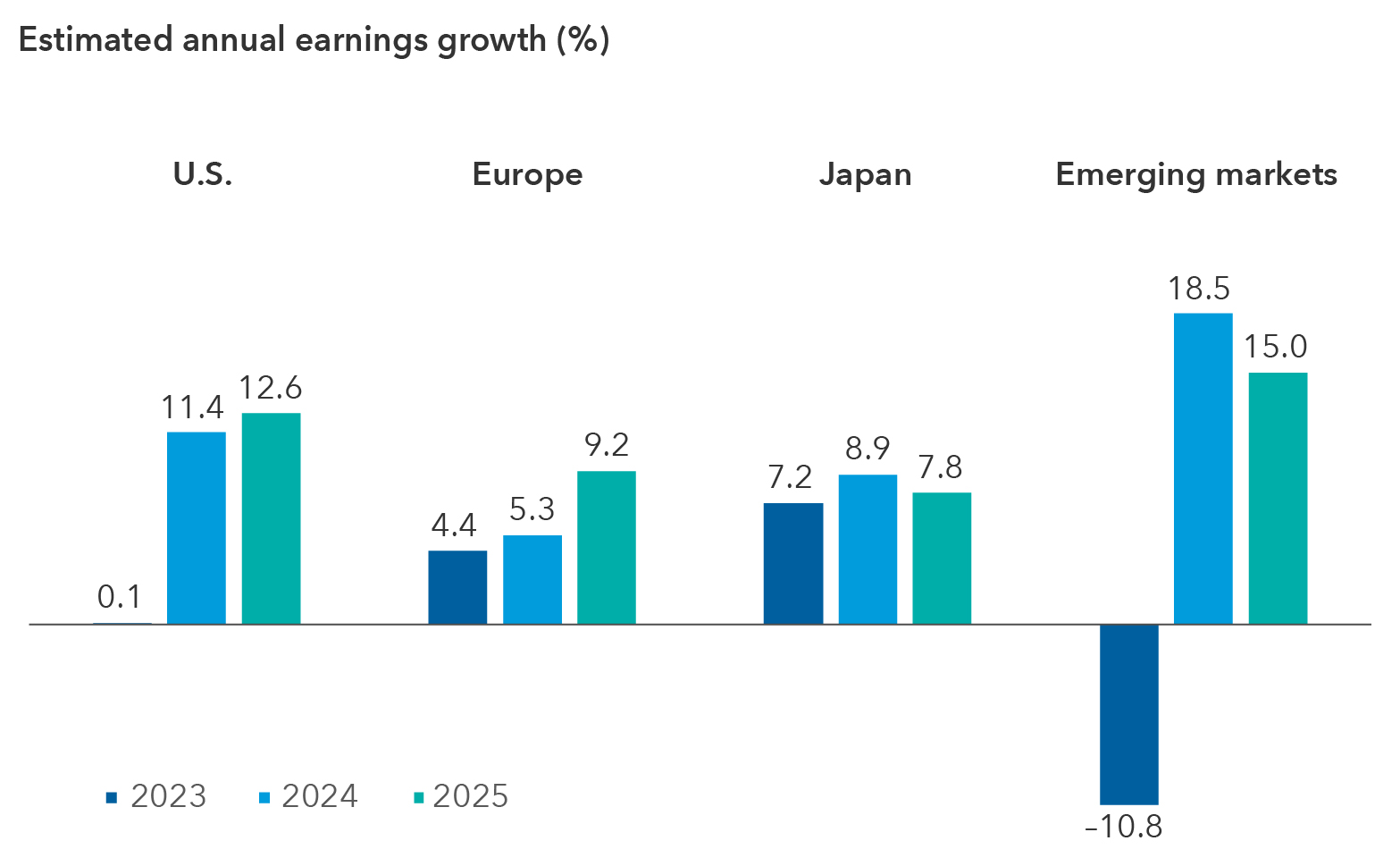

The MSCI Europe Index captures large and mid-cap representation across 15 Developed Markets (DM) countries in Europe.

The MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Markets (EM) countries.

The MSCI Japan Index is designed to measure the performance of the large and mid-cap segments of the Japanese market.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

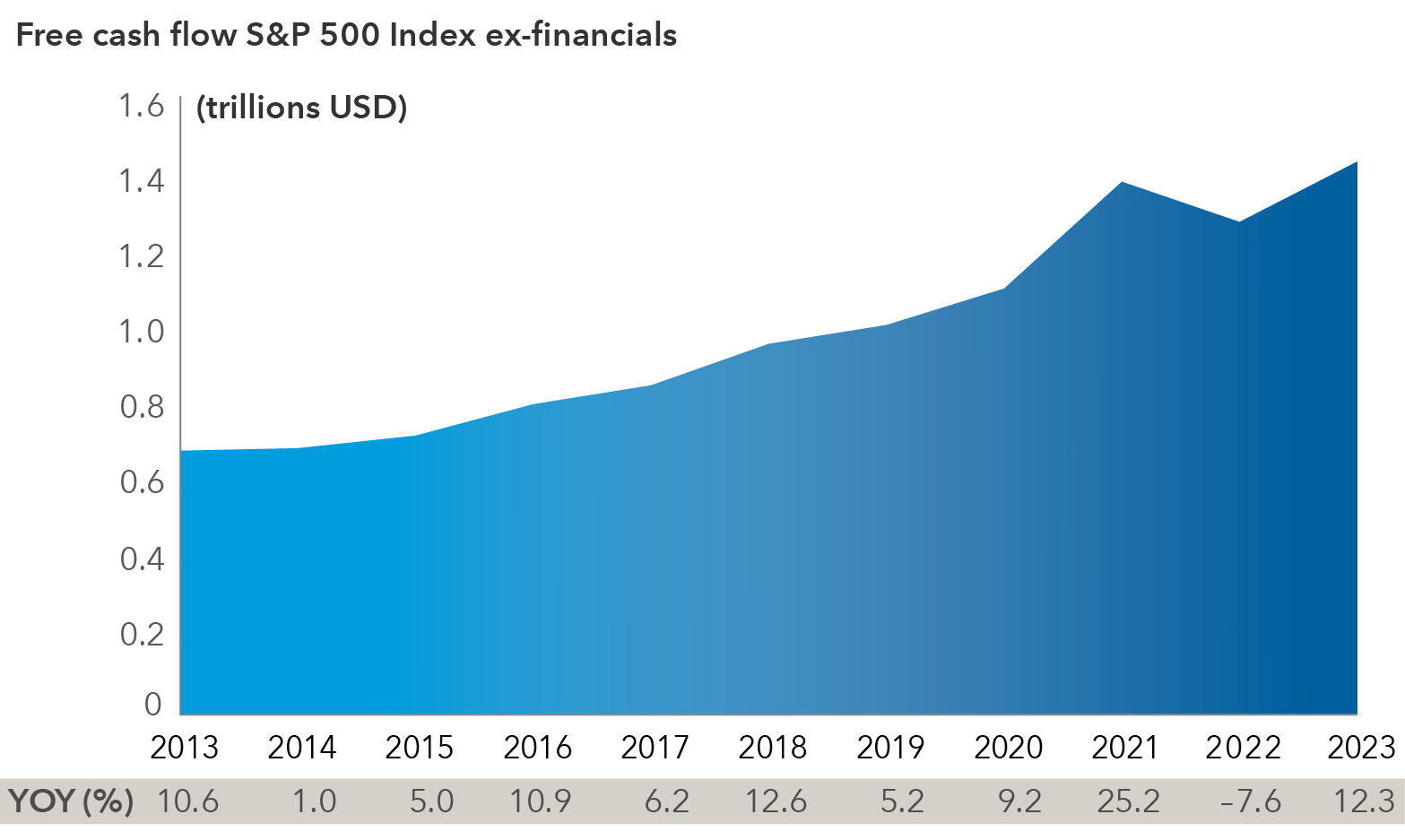

Free cash flow (FCF) – The remaining money available to a company after it has paid its operating expenses and capital expenditures. The more free cash flow a company has, the more it can use to repay creditors, pay dividends and for growth opportunities.

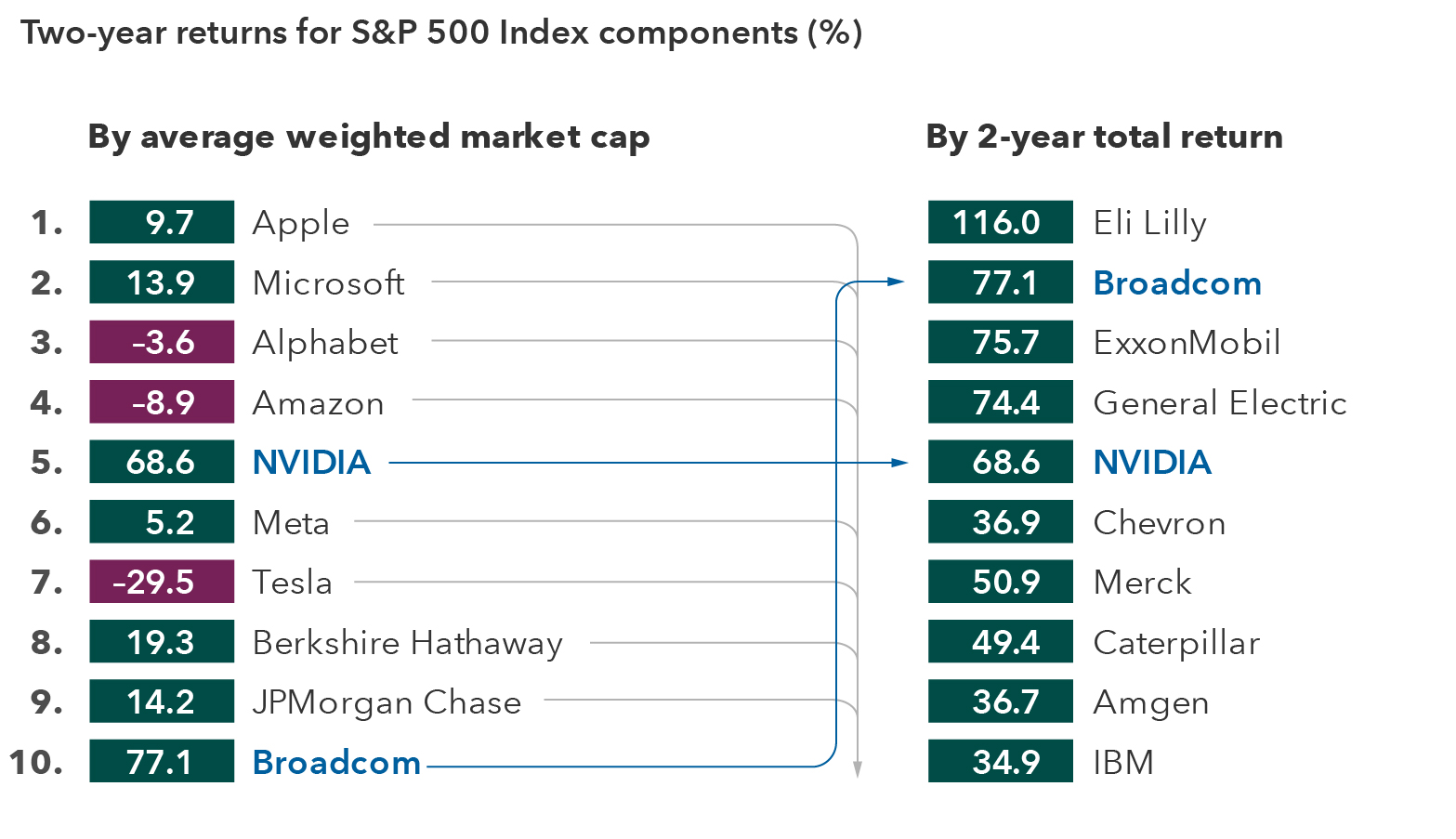

Average weighted market capitalization refers to a market index (e.g., S&P 500) in which each component is weighted according to the size of its total market capitalization.

The S&P 500 Index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.