Hyperscalers are large-scale cloud service providers that offer computing power and storage to organizations and individuals globally.

Circular financing is when an investor provides capital to a company that then buys that same investor’s products or services.

REIT (Real Estate Investment Trust)

SPAC (Special Purpose Acquisition Company) is a company with no operations that offers securities for cash and places substantially all the offering proceeds into a trust or escrow account for future use in the acquisition of one or more private operating companies.

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

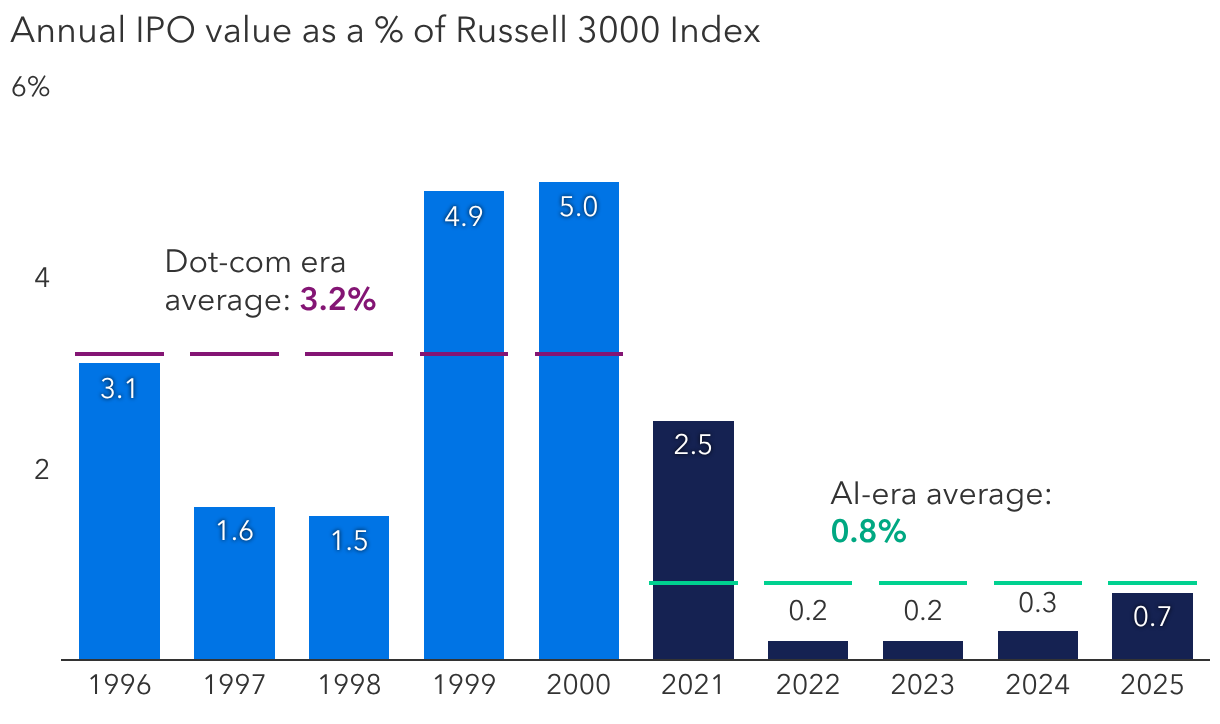

Russell 3000® Index measures the performance of 3,000 stocks and includes all large-, mid- and small-cap U.S. equities, along with some microcap stocks. The index is designed to represent approximately 98% of investable U.S. equities by market capitalization.

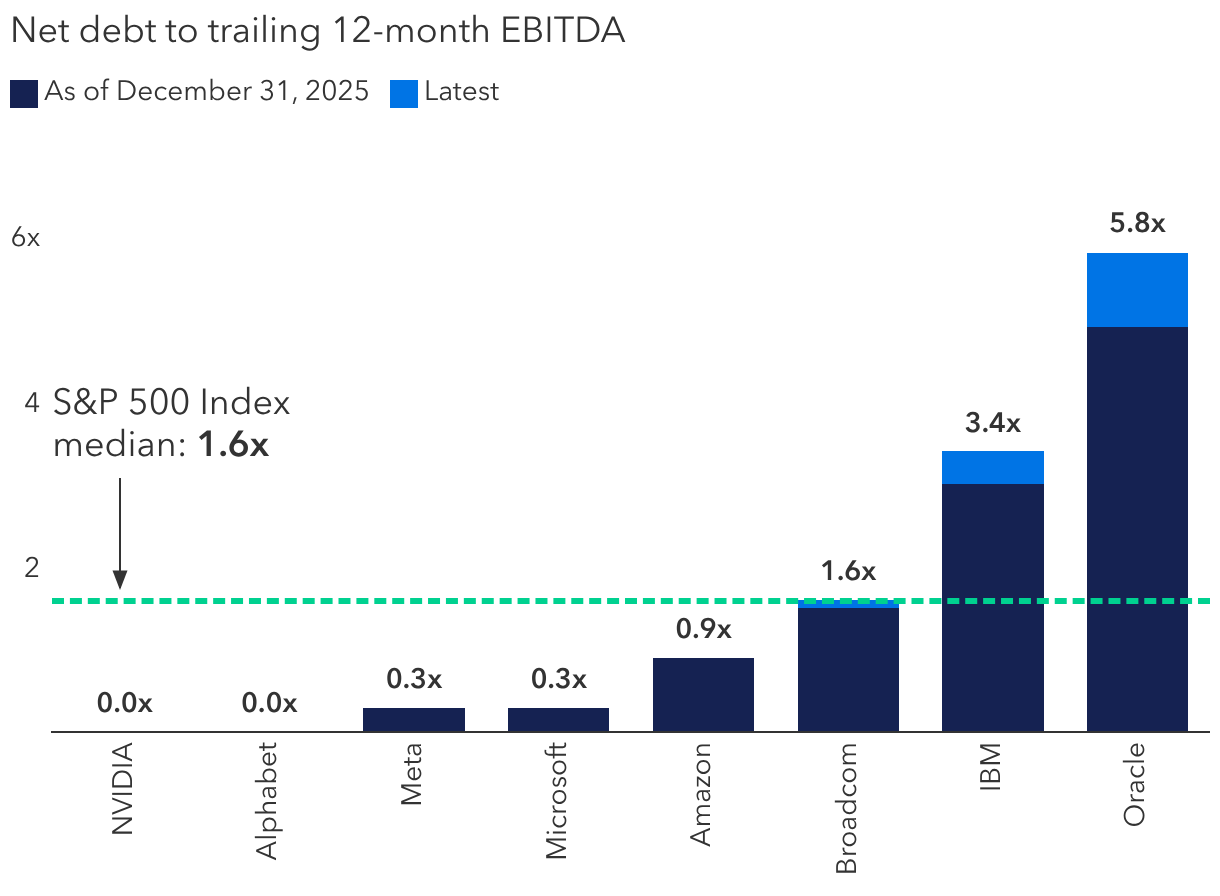

S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

The S&P 500 Index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. FTSE® and Russell® indexes are trademarks of the relevant LSE Group companies and are used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication.