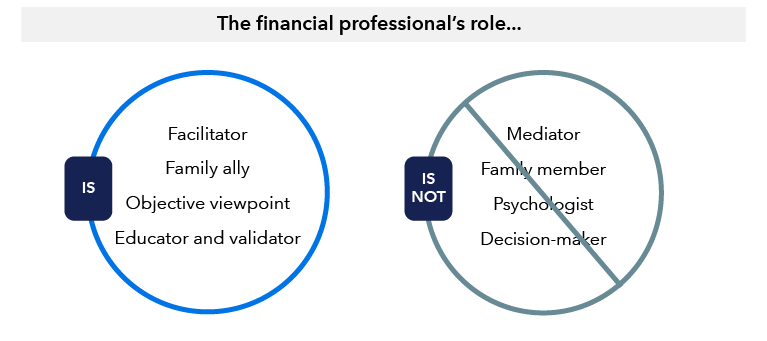

As a financial professional, you are well positioned to play an important role for clients looking to do generational wealth planning. You have the ability to look beyond assets and tailor family wealth management guidance based on the needs of the individual members and the family as a whole. More importantly, you have the skills to help bridge the communication gap between today’s very distinct generations.

Wealth transfers are not always easy to pull off. This is not necessarily due to the quality of the financial or estate planning advice or structures in place, but to inadequate preparation of the family and issues of trust and communication. Among the challenges faced by holders of wealth: a lack of comfort sharing financial information with their children in their lifetimes along with fear that children are not prepared to inherit wealth, according to the 2024 Private Wealth Management Executive Summary from Cerulli Associates.