Chart in Focus

Categories

- Market & Economic Insights

- Retirement Planning Insights

- Portfolio Construction Insights

- Wealth Planning Advisor Insights

Russia-Ukraine Conflict

Russia-Ukraine conflict threatens global economy

Robert Lind

Robert Lind

February 24, 2022

Russia’s invasion of Ukraine has triggered a swift response from U.S. and European governments. The imposition of economic sanctions is dominating the financial pages, but there are two other aspects of this crisis that I believe will have a more profound impact on the world economy. The first is the rising price of oil, which is now above $100 a barrel. We know from previous instances of geopolitical uncertainty, such as when Russia invaded Crimea in 2014, higher oil prices can have a significant drag on global economic activity.

From a European perspective, the more serious concern is what's happened to natural gas prices, which are already elevated. This reflects the concern that we will see a significant disruption of Russian gas supplies to the European Union. Ongoing geopolitical instability will likely push gas prices even higher. This will be especially problematic for countries such as Germany and Italy, two of Europe’s largest economies.

The major European economies have already experienced a steep rise in energy prices. Oil prices tend to feed through quickly to consumer prices. But the pass-through of gas prices from wholesale to retail varies, especially given support from governments seeking to protect consumers. Recent increases likely will continue to feed into consumer prices over the next few months.

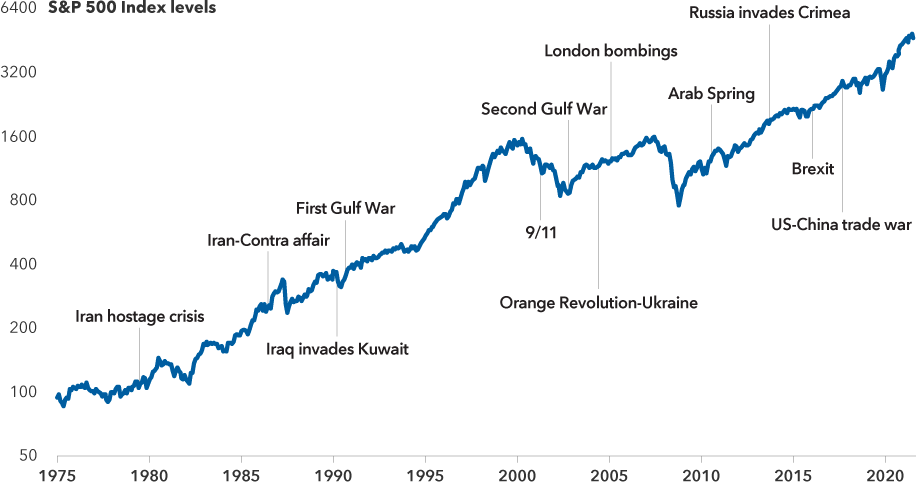

Equity markets have historically powered through geopolitical events

Sources: Capital Group, Refinitiv Datastream, Standard & Poor’s. Chart shown on a logarithmic scale. Index levels reflect price returns, and do not include the impact of dividends. As of January 31, 2022.

Germany’s announcement that it would not certify Nord Stream 2, a new gas pipeline from Russia to Germany, does not have any direct impact on supply as it’s not yet operational. Still, it’s possible we could see more significant disruption to Europe’s supply if Russia retaliates by restricting exports to the EU. This would hurt the Russian economy as well, of course, but Russia has built up its currency reserves to protect against such an eventuality.

Another pressing issue is what elevated commodity prices could mean for central bank policy.

Market Volatility Center

Find resources to help clients navigate the current crisis.

We may be in for another negative supply shock, which effectively raises inflation and depresses economic growth. I believe the Federal Reserve and the European Central Bank will proceed more cautiously in terms of tightening monetary policy. Both will likely wait to see how financial markets and commodity prices react. Ultimately, I think the Fed will raise interest rates but perhaps do so more gradually than markets anticipated a week ago.

I also expect European governments to step up support for households and companies to protect them from higher energy prices, reinforcing measures taken over the past few months. In a worst-case scenario of severe supply disruptions and elevated prices, governments might have to curtail energy demand and compensate affected companies and industries.

While the major European economies can cope with short-term supply disruptions and price volatility, there are growing concerns about the security of Europe’s energy supply in the medium term. It will be challenging for the EU to rebuild its gas storage in the spring and summer if there are continuing supply disruptions and demand remains strong.

As countries phase out coal the need for gas has increased. The German government has also confirmed the closure of its remaining nuclear plants by the end of 2022. There will be mounting pressure on European governments to continue their build-out of other energy sources. But this will take time, leaving Europe vulnerable to any further deterioration in relations with Russia.

Learn more about

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries. Small-company stocks entail additional risks, and they can fluctuate in price more than larger company stocks.

Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

Standard & Poor’s 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2022 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

RELATED INSIGHTS

-

Markets & Economy

-

-

Economic Indicators

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Effective July 1, 2024, American Funds Distributors, Inc. was renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.