This article is part of our Retirement Plan Trends series, which explores issues affecting the retirement space.

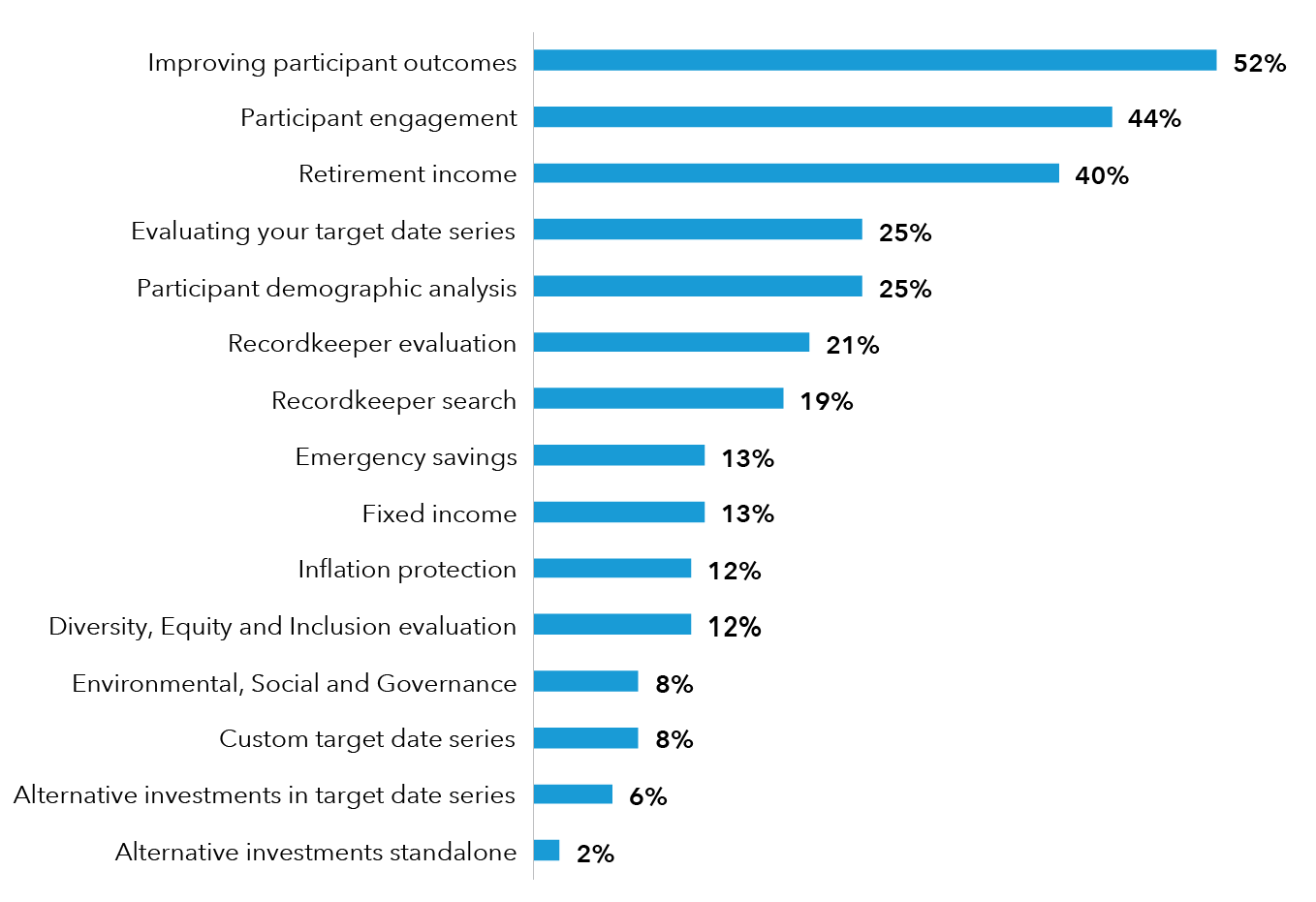

What keeps defined contribution (DC) retirement plan sponsors awake at night? While improving participant outcomes and addressing retirement income needs are among their top priorities, sponsors say potential legislative changes, consolidation in the recordkeeping industry, market uncertainty, inflation, rising interest rates and litigation risk could all disrupt how they manage their plans over the next five years, a new Capital Group survey shows. Several sponsors also mentioned aging participants needing more advice.