Chart in Focus

Categories

- Market & Economic Insights

- Retirement Planning Insights

- Portfolio Construction Insights

- Wealth Planning Advisor Insights

International

Making the case for international equities

Gerald Du Manoir

Gerald Du Manoir

Sung Lee

Sung Lee

Chris Thomsen

Chris Thomsen

May 4, 2023

International equities have long been overshadowed by the market’s fascination with leading U.S. technology companies. But the tide may be shifting. A confluence of top-down and bottom-up dynamics is making the case for international equities much stronger.

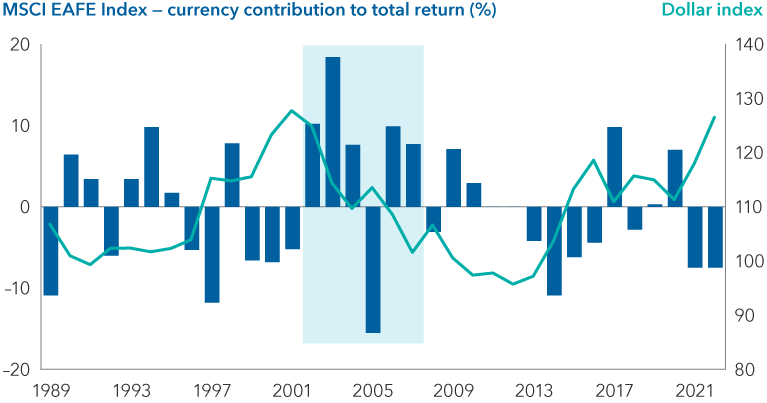

From a macro perspective, the U.S. dollar has weakened significantly against the euro and other global currencies since last October. Currencies can overshoot for extended periods, and the dollar has been overvalued on several metrics for many years. That said, in the past few months, we have seen signs of a turn. And in periods of dollar weakness, currency translation effects can significantly impact total returns from equities.

Weaker dollar can help boost international equities

Sources: Capital Group, Bloomberg, FactSet, J.P. Morgan. The dollar index is an effective exchange rate that measures the value of the U.S. dollar against a group of developed and emerging markets currencies. The annual currency contribution to the total return of the MSCI EAFE Index is expressed in percentage points of return. Shaded area represents prolonged period of dollar weakness. Data as of December 31, 2022.

Meanwhile, Europe has weathered the energy disruption from the Russia-Ukraine war better than expected, although a mild winter has helped. The European Central Bank’s efforts to rein in inflation had a dampening effect on the overall economy. GDP growth in the fourth quarter was flat as higher interest rates started to bite. Nevertheless, consumers have shown resilience, buffeted by savings built up during COVID lockdowns and by generous fiscal support provided to consumers during the pandemic.

China’s reopening could be another positive catalyst for Europe, given the strong trade ties between the two regions. It's also a large export market for Japan and other Asian countries.

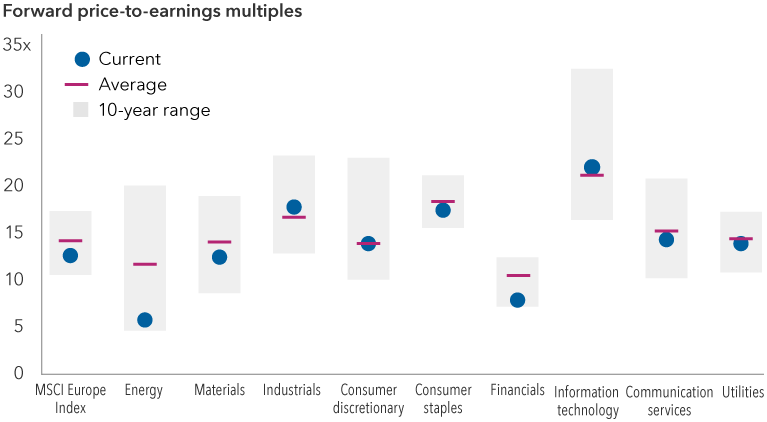

Against this supportive macro-economic backdrop, international equities led by European stocks have had a strong run over the past six months. Yet valuations remain below long-term averages for many sectors, suggesting there could be upside ahead.

Europe is trading at historically low valuations

Sources: MSCI, RIMES. Forward price-to-earnings ratio reflects the current share price relative to the consensus estimate for earnings per share on a forward 12-month basis. Data as of March 31, 2023.

Here, we discuss eight investment themes prevalent in our international equity portfolios and why they may be sources of returns over the next few years.

1. Semiconductors are crucial to power the digital economy

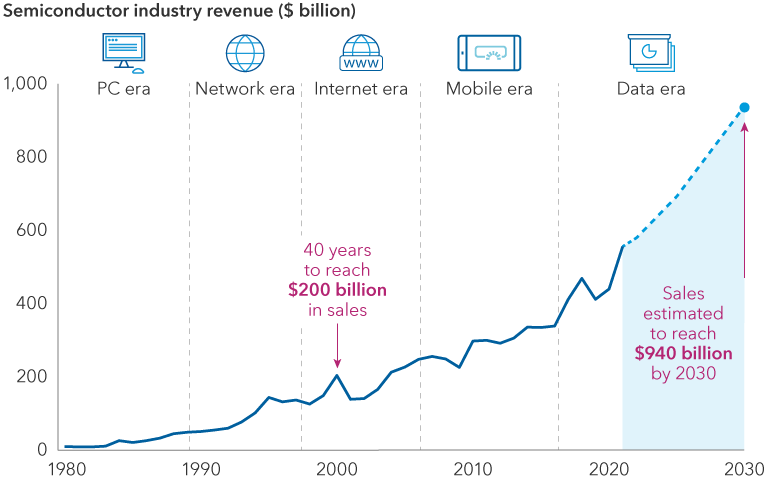

Despite the recent cyclical downturn and geopolitical headlines, the semiconductor industry appears poised to enjoy years of growth ahead. And companies outside the U.S dominate much of the industry.

The need for computing power is only increasing. Industry-wide revenue is projected to reach $940 billion by 2030, doubling from 2020, based on estimates from leading semiconductor equipment manufacturer ASML.

Several demand drivers are gaining traction. One is high-performance computing chips used in cloud computing and artificial intelligence (AI) functions like ChatGPT. Another is autos: Today’s average car contains many times more semiconductors than a smartphone.

We expect companies in Taiwan, Japan and Europe to thrive from these trends. Many of them have developed specialized expertise that is hard to replicate in manufacturing, chip-making equipment and laser-inspection tools for microchips.

Western governments have also realized semiconductors are essential to national security. The CHIPS and Science Act of 2022, which provides $52.7 billion for American semiconductor development, and a new fund established in Europe are among the efforts to incentivize companies to move production back home.

The pace of semiconductor sales is accelerating

Sources: Capital Group, ASML, Statista, WSTS. Data as of November 2022. 2022 estimate provided by WSTS. Projection through 2030 provided by ASML. The first semiconductor was created in 1960.

2. European firms have dominated interactive online entertainment

If you got lazy about making that trip to Las Vegas and decided to play online blackjack instead, chances are the platform is powered by a European company. Gaming and sports betting are among the fastest growing areas of online entertainment. The global online gambling market was valued at $63.5 billion in 2022 and is expected to grow at a double-digit rate for the next decade, according to various estimates.

Flutter of Ireland, Entain of the United Kingdom and Evolution of Sweden command this space, having developed the technology over the past decade. Online casinos and sports betting became legalized in many European markets earlier than the U.S. Now, as legalization of online casinos and sports betting expands state by state across the U.S., European firms have been gaining market share at a rapid pace.

We are seeing innovation in other areas of technology as well. Sweden’s Spotify is one of the world’s leading music-streaming platforms. U.K.- based Ocado developed valuable technology for the online grocery business. And there’s ASML in the Netherlands, whose EUV (extreme ultraviolet) lithography machines dominate leading-edge semiconductor manufacturing for high-end phones and data centers.

2024 Outlook webinar

Watch it on demand

CE credit available

3. The energy transition is creating new opportunities

Europe’s transition to energy sources outside of Russia is creating new opportunities across a host of industries, including renewed interest in European oil giants.

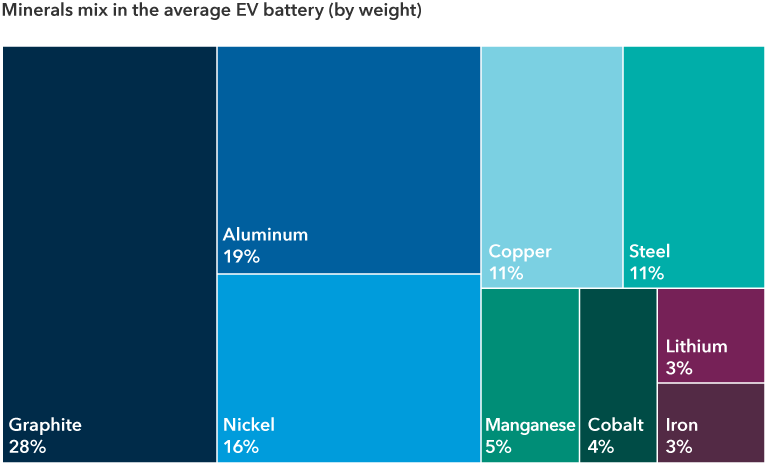

At the same time, many governments around the world are committed to reducing their reliance on fossil fuels and pivoting to renewable energies. The Inflation Reduction Act in the U.S. provides for a massive $369 billion package of tax credits, loans and grants to spur the capital investment needed to create a meaningful U.S. domestic solar and wind power-generation industry. But this energy needs to be stored using batteries that rely heavily on rare earth materials and industrial metals including copper, nickel and lithium.

Mining companies are gearing up for the energy transition. Rio Tinto recently said it intends to double its annual copper output by 2030, while BHP Group acquired OZ Minerals, a copper and gold miner. Mining companies in Canada, Great Britain and Australia have both the resources and the highly specialized expertise. In the near term, the materials sector can also benefit from a pickup in manufacturing activity in China as factories reopen across the country.

When it comes to building new homes or retrofitting older buildings, industrial companies in Europe are rapidly transitioning to alternative energy sources and newer, less energy-intensive manufacturing technologies.

Raw materials will play an important role in the energy transition

Sources: Capital Group, European Federation for Transport & Environment. Figures above reflect the mineral content of the average lithium-ion battery with a 60-kilowatt-hour capacity, which refers to the weighted average of electric vehicle battery chemistries on the market in 2020. Figures exclude materials in the electrolyte, binder, separator and battery pack casing. Data as of July 2021.

4. Consumer companies are showing pricing power

Although European economic growth has remained flat, the consumer has shown resilience, partly due to savings accumulated in the last few years amid COVID lockdowns and fiscal support from central governments. Against this backdrop, and facing rising input costs, large consumer goods giants have raised prices. In the near term, this can put pressure on operating and profit margins. Longer term, the price hikes usually stick, even as costs plateau or soften over time, which can help expand margins and profitability.

Consumer demand has been surprisingly resilient in many parts of the world. Now, with China’s reopening, we expect demand for luxury goods and travel to shoot higher. Prominent luxury goods companies LVMH and Hermès both reported strong first-quarter results, bolstered by demand from customers in China. While there is a degree of risk, given the potential for an economic slowdown, rising demand from China should offset slower demand in other markets. And importantly, European brands have become synonymous with luxury around the world, building leading market share positions and a level of expertise that is difficult to replicate, affording them a degree of pricing power.

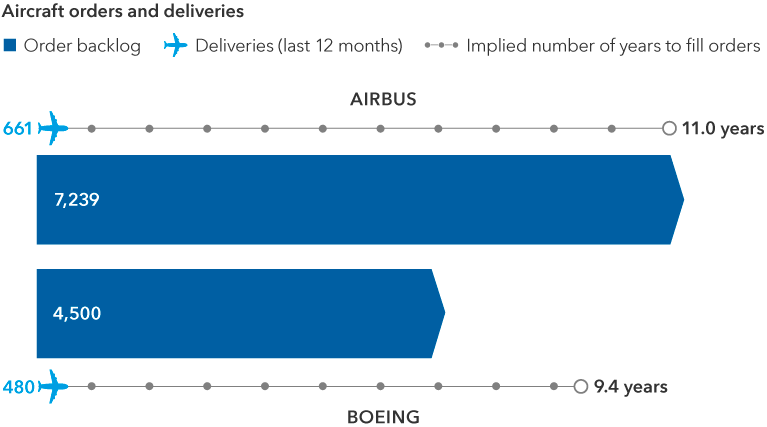

5. Aircraft makers, suppliers should benefit from secular growth in travel

Air travel is picking up again in a post-pandemic world and should get a big boost from China ending its three-year lockdown. Travel is a secular growth industry in a lot of countries, and demand is growing for new airplanes. Only about 20% of the world’s population has ever been on a plane. So there is huge room for growth, especially in emerging markets, where the middle class is growing, and air travel is still in its infancy.

More than 39,000 new aircraft are projected to be built by 2040, with roughly 40% slotted for Asian countries, according to Airbus and Boeing, who dominate the market. While U.S.-based Boeing specializes in wide-body aircraft, Airbus in France leads in midsize planes used for short-haul flights — the segment seeing the fastest growth. European companies also build engines and components, led by Safran, the world’s largest maker of engines for single-aisle planes as well as landing gear.

The dynamics of aircraft orders benefit the manufacturers. Airlines pay in installments and have prepaid most of the cost by the time the planes are delivered. Given the backlog, they don’t like to lose their place in the queue for deliveries. This provides a strong baseline for forecasting cash flows and revenue streams.

Commercial aircraft production has a long runway

Sources: Capital Group, company reports. Boeing's last reported order backlog is over 4,500, while Airbus has an order backlog of 7,239 planes. Data as of December 31, 2022.

6. Japanese companies are showing signs of reinvention

Japan’s corporate world doesn’t garner much headline attention. But several companies are undergoing transformations. Olympus is known worldwide as a camera brand, but that’s no longer its emphasis after a multiyear restructuring. Leveraging technology developed over the decades, Olympus has transformed itself into the world’s leading supplier of endoscopes used in medical procedures. Fujifilm is another example. The company has evolved into a major player in health care, offering drug development and manufacturing services to multinational pharmaceutical companies. It has also expanded into the semiconductor materials business.

In other areas, Japanese firms have carved out unique technologies used in industrial automation equipment and inspection tools for semiconductor manufacturers. These companies will likely play a central role as we see an industrial renaissance in developed economies and ongoing industrialization in developing economies.

Corporate Japan has been on a journey to improve profitability, capital allocation and corporate governance since 2012 under policy reforms advocated by former Prime Minister Shinzo Abe. And more recently, Japanese companies have seen a rise in shareholder activism, with investors asking for a better return on investments. As many companies tend to have high levels of cash on their balance sheets, this could lead to companies paying out more of their excess cash in dividends.

7. Innovation could benefit pharmaceutical giants

Innovation is ramping up in health care. Europe is home to many high-quality pharmaceutical companies. Many have invested heavily in drug discovery in recent years and have built deep pipelines of pioneering treatments to tackle some of the world’s biggest health issues.

Some pharmaceutical companies such as AstraZeneca are transitioning from a broad suite of health care drugs toward specialty care; roughly 40% of AstraZeneca’s drugs are now related to oncology. This allows companies to create dominant franchises in select areas of health care.

As investor optimism has risen, valuations have expanded, making us somewhat cautious in the near term. That said, with better visibility on future growth and no major patent expirations in the coming years, pharmaceutical companies may see higher price-earnings multiples than they did in the prior decade.

In an uncertain macro environment, the strong capitalization of many pharmaceutical companies is another positive factor. Many have plenty of cash on their balance sheets to pay dividends or fund their own growth through acquisitions. This could help in a higher interest-rate world where raising debt capital will be more expensive.

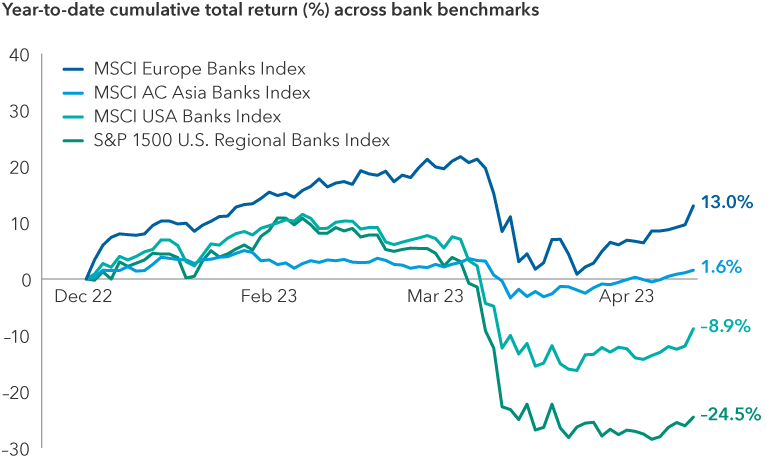

8. Select opportunities may exist in European and Asian financials

Credit Suisse’s merger with UBS in late March generated headlines about weak links in the banking system. But overall, the European banking sector is arguably in its strongest operating position since the great financial crisis. Banks have built up significant capital reserves to absorb potential loan losses, which should protect earnings in a recession. Capital ratios and profitability are at all-time highs. Furthermore, positive interest rates should help net interest income (a key profitability measure) for the rate-sensitive banks.

Compared with their U.S. counterparts, European banks do not take on large amounts of interest-rate risk due to tighter regulations. Banks in Europe also tend to be relatively well diversified, with large funding bases built on retail branch deposits. Our banking analysts anticipate returns on capital should improve. Given a less restrictive regulatory environment, dividends could increase, and buybacks may rise.

Similarly, domestic-focused Asian banks appear relatively sound for several reasons. Besides operating in countries where economic growth rates are projected to outpace the developed world, they have limited exposure to U.S. regional banks and Credit Suisse. They are well capitalized and tend to have smaller investment portfolios.

European and Asian bank stocks have held up relatively well

Sources: Capital Group, MSCI, RIMES, Standard & Poor's. Data reflects period from December 31, 2022, through April 14, 2023.

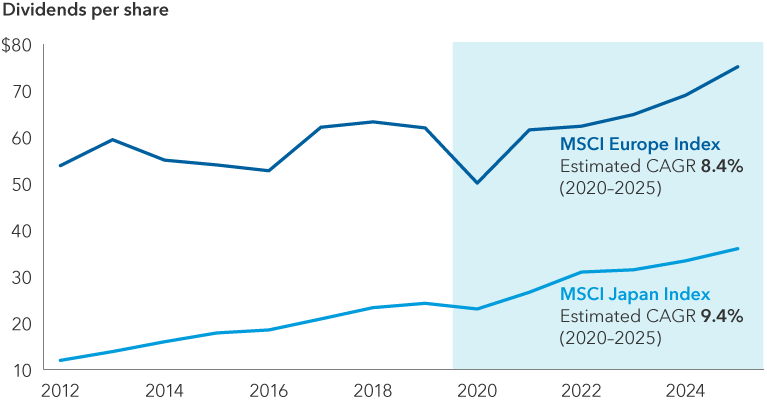

An increased focus on dividends

We are also seeing a greater-than-ever focus on and commitment to dividends. Corporate managements, particularly in Europe and Japan, seem to be balancing capital expenditure and operating cash flow needs with a stronger desire to return cash to shareholders via dividends.

International dividends projected to grow

Sources: FactSet. Data for 2023-2025 is based on consensus estimates as of February 17, 2023. CAGR = compound annualized growth rate.

A broad opportunity set spans growth and value

Inflection points in markets tend to prompt investors to take a fresh look at asset allocation. The rise in interest rates around the world triggered by tighter monetary policy has been a reset of sorts for all financial assets. Growth stocks pulled back last year and have rebounded as the monetary tightening cycle appears closer to the end than the beginning.

Nevertheless, portfolio flows over the past six months can be read as a signal that investors are looking to broaden their equity exposure beyond the dominant U.S. technology companies. International equities spanning many industries across the growth and value spectrum provide a diversified opportunity set with valuations that appear reasonable by many measures.

Learn more about

All indexes are unmanaged, and their results include reinvested distribution but do not reflect the effect of sales charges, commissions, account fees, expenses, or U.S. federal income taxes.

The MSCI Europe Index captures large and mid-cap representation across 15 developed market countries in Europe. With 424 constituents, the index covers approximately 85% of the free float-adjusted market capitalization across the European developed markets equity universe.

The MSCI AC Asia Index captures large and mid-cap representation across developed market countries and emerging markets countries in Asia. With 1,425 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market. With 237 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan.

The MSCI USA Banks Index captures 17 large and mid-cap banks in the United States.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The S&P 1500 Regional Banks Sub-Industry Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2022 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

Get the 2024 Midyear Outlook report

RELATED INSIGHTS

-

Markets & Economy

-

Asset Allocation

-

Markets & Economy

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

There have been periods when the results lagged the index(es) and/or average(s).

The indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Effective July 1, 2024, American Funds Distributors, Inc. was renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.