Market Volatility

Talha Khan

Talha Khan

Darren Peers

Darren Peers

Pramod Atluri

Pramod Atluri

Don't miss our latest insights.

As war in the Middle East escalates, investors are confronted with the reality of a world that is becoming more dangerous. With markets reacting minute by minute to the news, it’s helpful to take a step back and consider events in a broader context. With that in mind, three Capital Group professionals offer their assessments of the developing U.S.-Iran conflict.

Markets are adjusting to higher geopolitical risk

Talha Khan, political economist

The death of Iran’s Supreme Leader Ayatollah Ali Khamenei marks a significant escalation in the long-running conflict between the United States, Israel and Iran. U.S. and Israeli military attacks targeting senior Iranian leadership represent a direct strike at regime command, rather than the type of limited infrastructure campaign we’ve seen in the past. Iran has responded with missile and drone attacks against Israeli territory, U.S. military bases and adjacent countries.

In financial markets, initial reactions reflected shock and uncertainty but not panic selling. Gold prices jumped and the U.S. dollar rose as investors sought safe-haven hedges. Oil prices moved significantly higher as traders worried about supply disruptions. But global equity and fixed income markets were more subdued amid expectations that U.S. military action may be short lived.

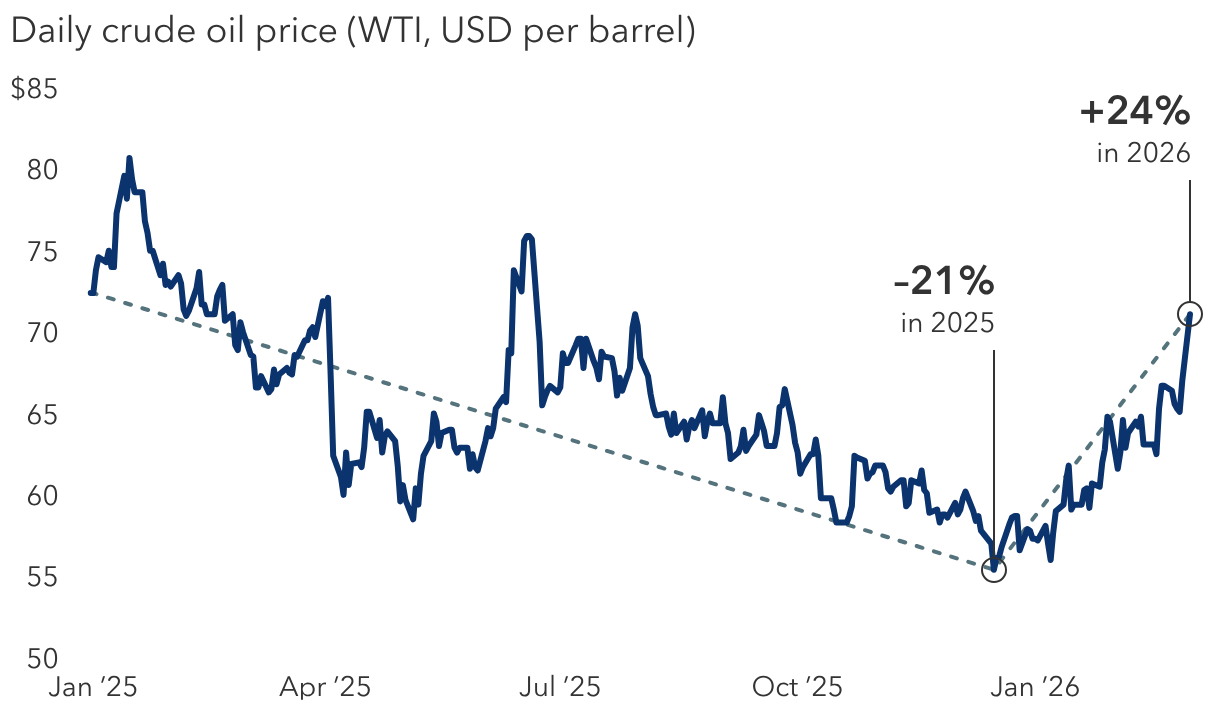

Oil prices have spiked this year amid growing tensions in Iran

Sources: Capital Group, LSEG Refinitiv. Oil prices are represented by the spot price for West Texas Intermediate (WTI) crude. As of March 2, 2026.

For now, markets are adjusting to higher geopolitical risk but not yet positioned for a prolonged regional war. Whether that happens will depend on three pivotal events: the severity of Iran’s retaliation, the security of oil flows through the Strait of Hormuz and, ultimately, the outcome of the Iranian leadership succession. If power consolidates quickly in Tehran, retaliation is likely to be forceful but controlled. If Iranian leadership splinters or competing factions emerge, the path of escalation becomes more unpredictable.

How high can oil prices go?

Darren Peers, equity investment analyst covering the oil and gas industry

For long-term investors, the critical question is what, if anything, could impair Middle East oil production over a medium- to long-term basis? Damage to above-ground oil export facilities can generally be repaired in a matter of days or weeks. The Strait of Hormuz isn’t likely to be closed for an extended period. Those are transitory issues unlikely to upset global oil supplies over the long term.

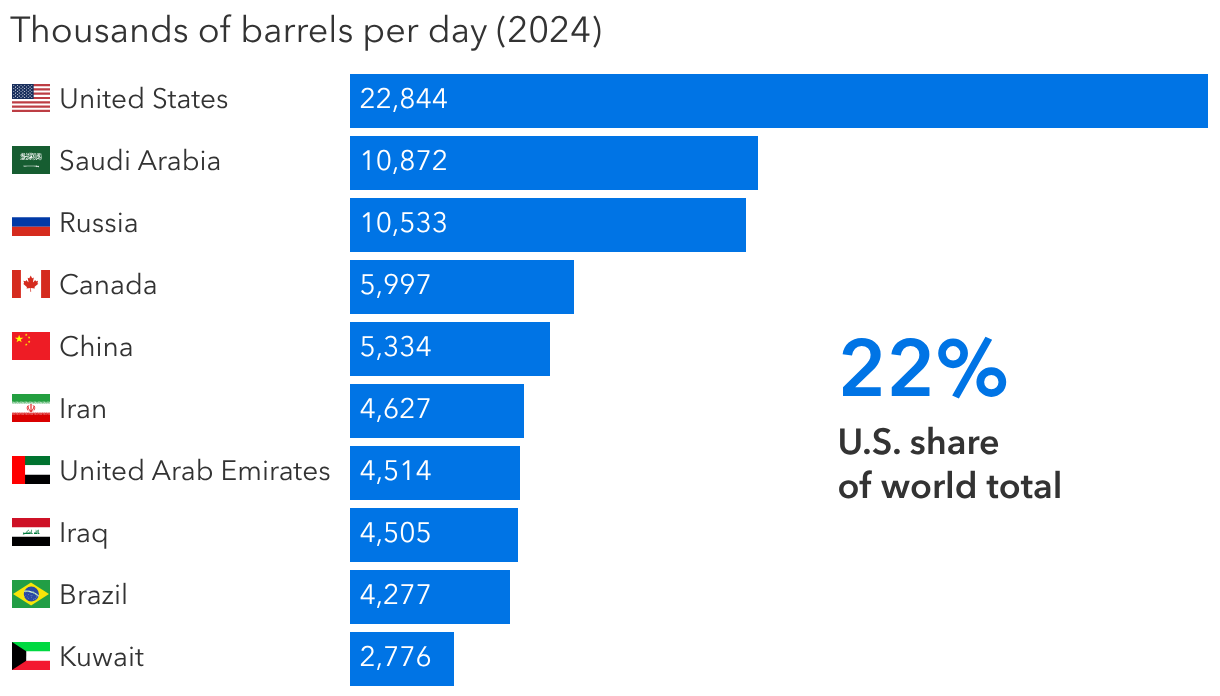

During the past two decades, energy markets have generally bounced back from geopolitical shocks because they haven’t led to prolonged physical disruptions. Over time, investors have tended to fade any big commodity price moves or equity price moves. It also helps that the United States, which is the world’s leading consumer of oil and gas, is also now the largest producer. That wasn’t the case 20 years ago when troubles in the Middle East would have had a bigger impact on U.S. and global markets.

U.S. oil production has soared in recent years

Sources: Capital Group, U.S. Energy Information Administration. Data includes petroleum and other liquids such as biodiesel, ethanol, liquids produced from coal, gas, and oil shale, Orimulsion, blending components, and other hydrocarbons. Latest data available is 2024 as of March 2, 2026.

Today there are significant differences. This conflict has the potential to linger longer than markets expect with more widespread military action. But if we don’t experience a lengthy disruption in oil supplies then, in my view, prices that have risen well into the $70s today will likely move back to pre-conflict levels in the range of $60 a barrel as the geopolitical premium fades and market fundamentals reassert themselves.

Bond markets are focused on inflation impact

Pramod Atluri, principal investment officer, The Bond Fund of America®

The Iran conflict has the potential to worsen some of the trends that have been pressuring risky assets over the past few weeks, including AI fears, private credit troubles, record corporate bond supply and sticky inflation that could lead to a more hawkish Federal Reserve. The most obvious impact is higher energy prices, which feed directly into inflation. If rising inflation leads the Fed to hike interest rates, that could hurt future economic growth and increase capital costs for businesses and consumers.

Broadly speaking, the fixed income markets are not acting like the conflict is a material risk-off event for companies. Instead, the greatest impact is being felt by a sell-off in rates — which means inflation is the biggest concern. We haven’t seen a meaningful widening in credit spreads yet. And that means there is still time to de-risk if one thinks these global macro forces could lead to an economic downturn.

Right now, the market is treating this conflict as an inflation shock, not a growth shock. But should the conflict expand or last longer than expected, an inflation shock could become a growth shock. That’s something investors may want to keep in mind as events unfold.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries.

Oil prices are expressed in U.S. dollars per barrel.

A “risk-off event” refers to a shift in investor sentiment from optimism to pessimism, resulting in a general rotation into perceived safe-haven assets, such as gold and the U.S. dollar.

Our latest insights

-

-

Demographics & Culture

-

-

Global Equities

-

Target Date

RELATED INSIGHTS

-

Emerging Markets

-

-

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week