Demographics & Culture

Categories

U.S. Equities

How AI is reshaping U.S. equity markets

Martin Romo

Martin Romo

Greg Miliotes

Greg Miliotes

David Polak

David Polak

Victoria Quach

Victoria Quach

May 5, 2026

Don't miss our latest insights.

Get the latest report on U.S. equities

Signs of transformation are emerging in U.S. equity markets amid a torrent of AI-related spending. The shift comes after more than a decade of concentrated gains for market-cap-weighted indexes, which thanks to a narrow group of megacap technology stocks, pushed valuations to historic extremes.

Investors are increasingly moving into sectors and individual stocks underrepresented in these indexes. Dispersion among the stocks that constitute the S&P 500 Index is near multidecade highs. Previously lagging sectors, such as industrials, and style factors, including value and yield, are reasserting leadership amid expectations that AI hyperscalers could drive top-line growth.

In this environment, deep fundamental research and careful security selection have become increasingly important. Here are the key themes our team is following.

AI revolution gets physical as earnings surge

Although investors have focused on semiconductor manufacturers and hyperscalers to capitalize on the AI boom, focus has since shifted to AI-adjacent beneficiaries. These companies stand to benefit from a surge of tech-driven capital expenditure amid an arms race to train AI models, deploy them at scale and integrate them into virtual and physical workspaces.

Free cash flow in the tech sector has empowered a substantial increase in earnings expectations over the past few months. But the market appears to see through this dynamic, realizing instead of driving dividends, share buybacks or mergers and acquisitions as in the past, earnings could turn into top-line growth for AI-adjacent sectors. As a result, forward price-to-earnings (P/E) ratios of non-tech sectors are perking up.

Outside of the energy rally driven by the Iran conflict, industrials, utilities and materials have been among the better performing sectors year-to-date through March. These sectors drive the picks-and-shovels enablement of the AI boom, powering steel- and concrete-intensive data centers built with plumbing, HVAC machinery and electrical — some of which are back-ordered for years.

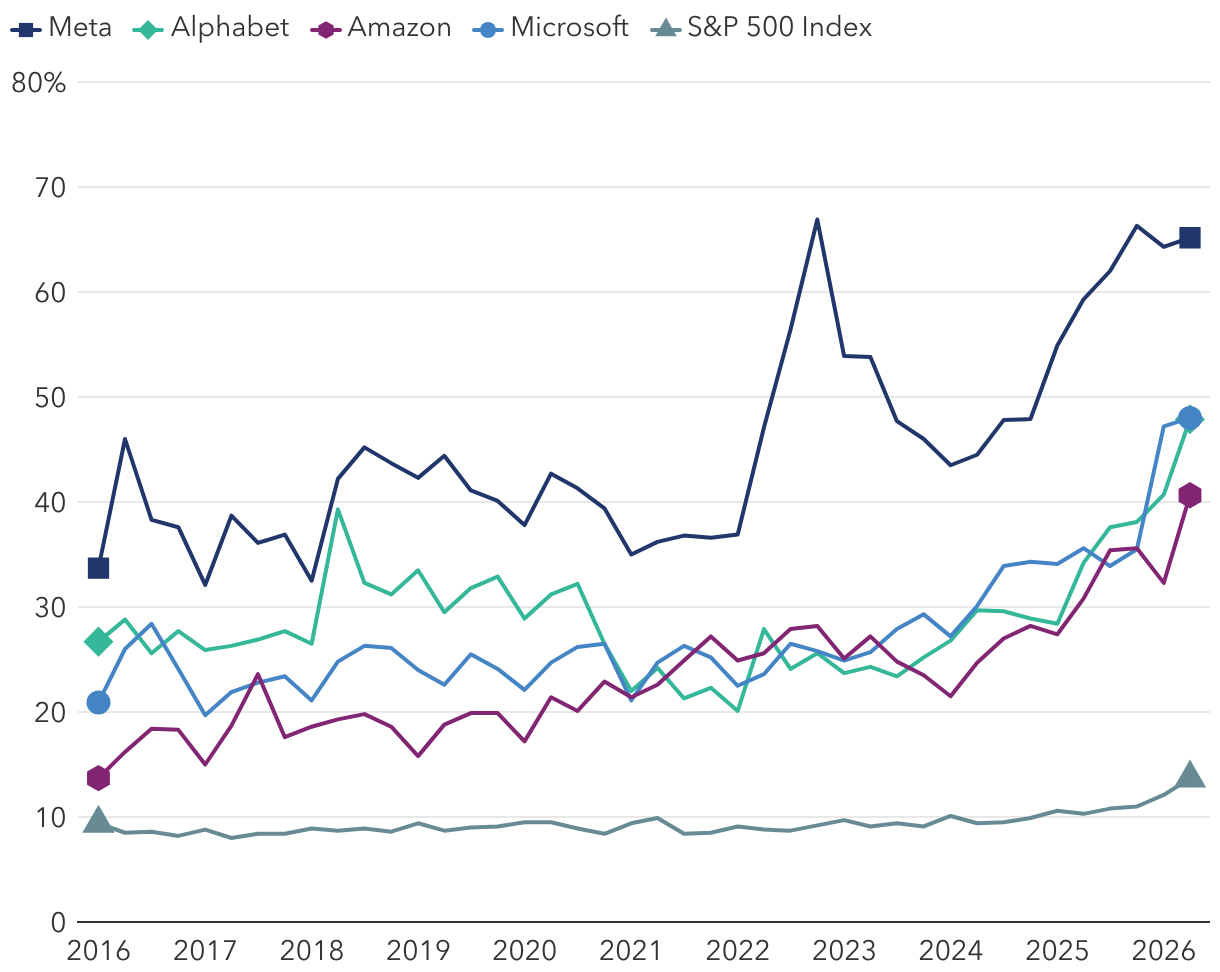

AI spending surge puts hyperscalers atop broader market

R&D and capex share of sales

Sources: Capital Group, FactSet. As of March 31, 2026. R&D: Research and development costs. Capex: Capital expenditure.

Magnificent Seven introduces concentration risk

The Magnificent Seven stocks have been moving in ways that challenge portfolio diversification. There are two dimensions to this:

- How correlated are these seven stocks to each other?

- How correlated are they to the rest of the S&P 500?

When correlations are high, the benefits of diversification fall, because these stocks increasingly trade as a single unit. A 2025 analysis by S&P Global Market Intelligence found the average rolling 2-year correlation among this cohort hit nearly 60% in 2024, with the highest correlations between Microsoft and both Alphabet and Amazon.

Relative to the S&P 500 Equal Weight Index, the Magnificent Seven’s correlation hit almost 100% in the second half of 2025 before reversing into negative territory, as these stocks have significantly underperformed the average S&P 500 stock as of March 31, 2026.

This correlation trend shows that owning all seven is no longer providing independent streams of return but rather one giant concentrated tech position.

Get the latest report on U.S. equities

Gap widens between winners and losers

Cross-sectional volatility within the S&P 500 is returning to COVID-era highs. This indicates the gap between winners and losers is widening.

A 2025 analysis by Goldman Sachs found that roughly 73% of the variance in the typical S&P 500 stock’s trailing 6-month return was driven by company-specific factors, versus an average of 58% from 2002 through the first two months of 2025. Separately, a 2024 analysis by Morningstar found a correlation between higher return dispersion and higher active manager success rates against their benchmarks during the period studied from 1999 to 2023.

S&P 500 cross-sectional volatility rises

Source: Capital Group. As of December 31, 2025. Based on Bloomberg total return data for S&P 500 constituents. Return volatility is expressed through standard deviation.

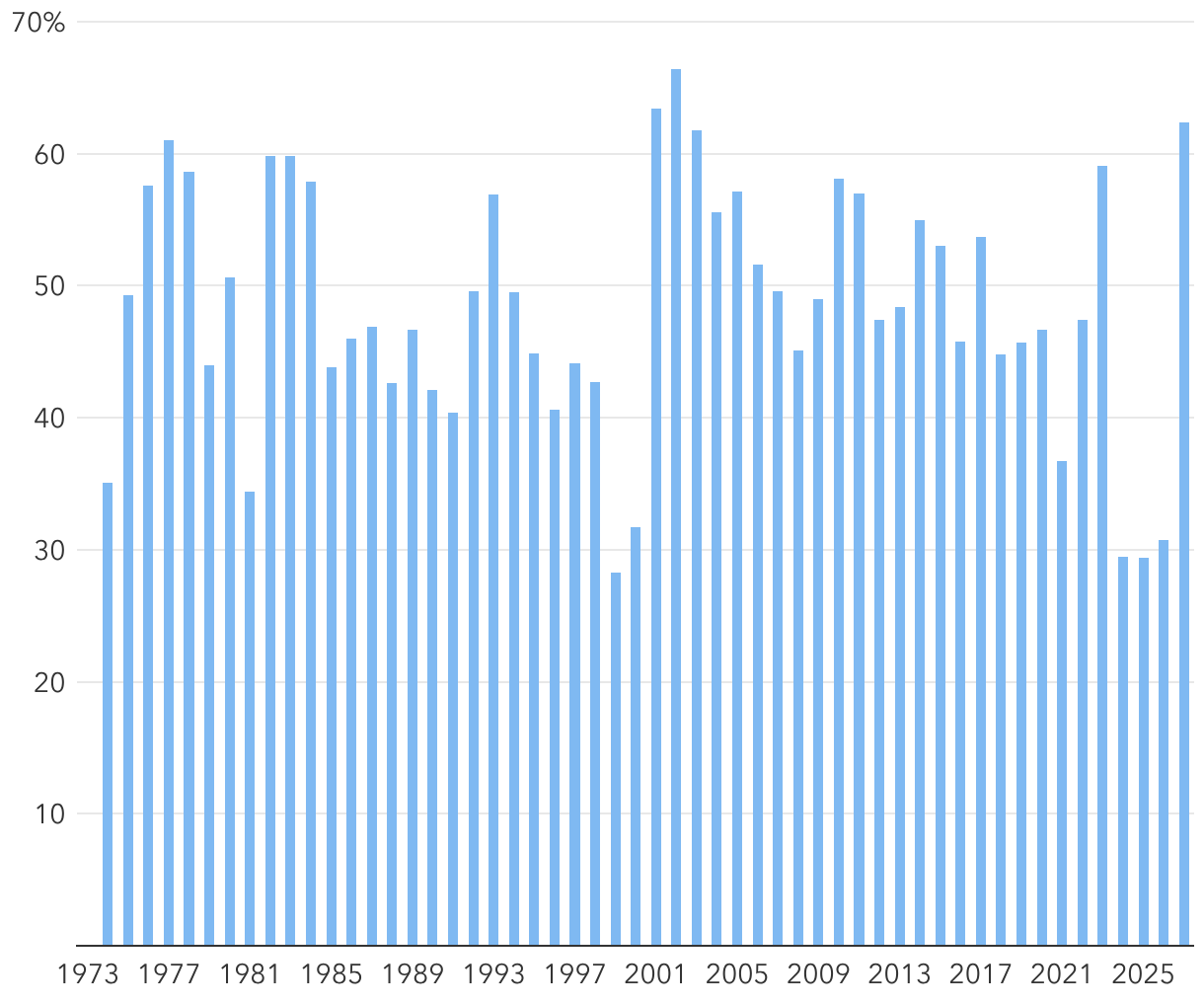

Smaller, cheaper and rising fast

Finally, 2026 started with 62.4% of S&P 500 constituents outperforming the index itself — the highest level in more than two decades and a marked reversal from the lows seen in recent years.

Share of individual stocks outperforming hits multidecade high

Percentage of S&P 500 stocks outperforming the index over a calendar year

Source: Ned Davis Research, Inc. Based on year-end data from 1973 to 2026 (year-to-date as of February 16, 2026).

Returns are no longer concentrated in a handful of megacap, growth-oriented stocks. For example, value has outpaced growth. The Russell 1000 Value Index beat the Russell 1000 Growth Index by 12% through the first quarter.

Small-cap stocks represent another area of opportunity. After years of underperformance, they trade at historical valuation discounts relative to large caps. The Russell 2000 Index, which tracks small-cap stocks, outpaced the S&P 500 by more than 5% as of March 31, 2026.

Bottom line

The capital expenditure fueling the AI boom is also driving broader dispersion in the market. Success moving forward is likely to depend on discernment — directing capital toward quality businesses, emerging winners and genuine bargains, while avoiding the overhyped and overvalued. A more selective approach could become increasingly important if capital transfer accelerates between sectors in the years ahead — rotating from tech earnings and capex to companies anchored in tangible assets, durable cash flows and disciplined reinvestment.

Learn more about

Correlation: A statistical measure of how assets or indexes move in relation to each other, ranging from -1 to 1. A positive correlation close to 1 implies that when one moves either up or down, the other moves in the same direction. A negative correlation approaching -1 indicates the two have moved in opposite directions.

Magnificent Seven: A group of companies (Microsoft, Apple, Alphabet, Amazon, NVIDIA, Meta and Tesla) whose stocks dominated U.S. stock market indexes in 2023.

Passive funds are not striving to outpace their benchmarks; rather, they seek to replicate the benchmark’s return pattern.

Price-to-earnings (P/E) ratio: A company’s price per share of stock divided by the company’s earnings per share. Also known as the earnings multiple, this measure is a common tool in fundamental analysis that helps compare how relatively expensive one stock may be compared to another.

Russell 1000 Growth Index: A market-capitalization-weighted index that represents the large-cap growth segment of the U.S. equity market and includes stocks from the Russell 1000 Index with higher price-to-book ratios and higher expected growth values.

Russell 1000 Value Index: A market capitalization-weighted index that represents the large-cap value segment of the U.S. equity market and includes stocks from the Russell 1000 Index that have lower price-to-book ratios and lower expected growth values. This index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

Russell 2000 Index: Measures the results of small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000 Index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership.

Standard deviation: A statistical measure that quantifies the amount of variation or dispersion of a set of values from their mean.

S&P 500 Equal Weight Index (EWI): The equal-weight version of the widely used S&P 500 Index. The EWI includes the same constituents as the capitalization-weighted S&P 500, but each company in the S&P 500 EWI is allocated a fixed weight, about 0.2% of the index total, at each quarterly rebalance.

S&P 500 Index: A market-capitalization-weighted index based on the results of approximately 500 widely held common stocks. This index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

Success rate: The percentage by which a portfolio outperforms a benchmark or index over a given period.

Our latest insights

-

-

Demographics & Culture

-

-

Artificial Intelligence

-

RELATED INSIGHTS

-

Podcast

-

Economic Indicators

-

Artificial Intelligence

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Small-company stocks entail additional risks, and they can fluctuate in price more than larger company stocks.

The indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

FTSE/Russell indexes: London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. FTSE indexes are trademarks of the relevant LSE Group companies and are used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication.

Each S&P Index ("Index") shown is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

© 2026 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar, its content providers nor Capital Group are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Information is calculated by Morningstar. When applicable, due to differing calculation methods, the figures shown here may differ from those calculated by Capital Group.