Asset Allocation

Paul Benjamin

Paul Benjamin

Lisa Thompson

Lisa Thompson

Rob Lovelace

Rob Lovelace

Don't miss our latest insights.

With gold prices rising to record highs over the past three years, investors have increasingly turned their attention to this ancient store of wealth. What’s driving the rapid increases, especially at a time when stocks and bonds have also generally done well?

The war in Iran halted gold’s rise for a time, as investors worried that higher oil prices might drive up inflation and thus lead to higher interest rates. Gold and interest rates have historically moved in opposite directions. But with this week’s cease-fire agreement, volatile gold prices have stabilized in the range of $4,600 to $4,700 an ounce. While that’s below the record high around $5,300 in January, it’s still far above where it was when this remarkable rally began in early 2022 — when gold was trading below $1,800.

Where the price goes from here is a subject of vigorous debate. Was January the peak? Or does it have more room to run? And, regardless of its short-term direction, what role should gold play in a long-term investment portfolio? With those questions in mind, three Capital Group portfolio managers offer their views.

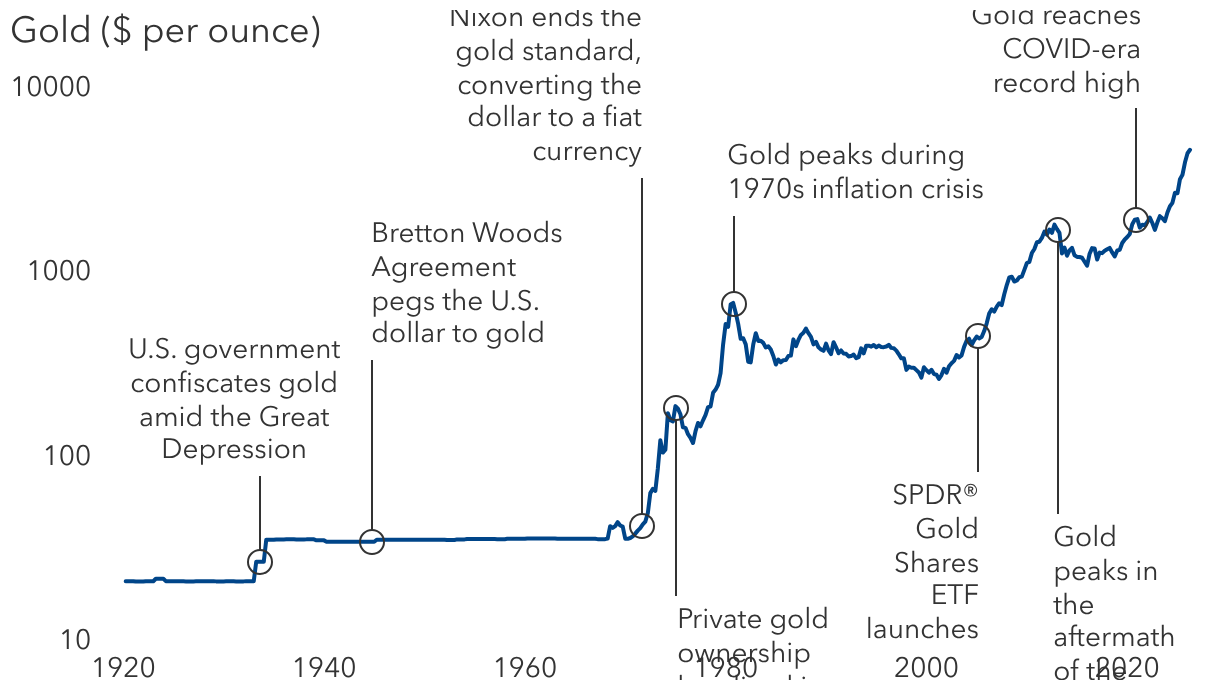

All that glitters: Charting the path of gold prices over the decades

Sources: Capital Group, Bloomberg. As of March 31, 2026. Event dates are aligned to the nearest end of quarter market price. Prices shown on a logarithmic scale.

Gold prices are likely headed higher

— Paul Benjamin, portfolio manager, American Balanced Fund®

My outlook for gold prices is likely upward, but the magnitude will be determined by the level of real interest rates and real inflation-adjusted return from stocks and bonds. If you were to use a constant basket to define inflation, and you looked at real interest rates minus inflation, you'd see that real rates have been very low since the global financial crisis. Gold tends to do well in those periods.

In addition, we had the freezing of Russian Treasury reserves in 2022, which caused central bank buying from non-Western central banks to accelerate dramatically. And then, interestingly, late last year we started seeing lots of news stories about the “debasement trade.” When people refer to the debasement trade, they're talking about fiscal concerns in many Western countries, including a lack of central bank independence and the risk that governments may need to inflate away their debt. I'd say those are the major issues that line up, driving gold and helping it accelerate in recent years.

In my view, gold has an important role in a portfolio, particularly in a balanced fund. I view it as an important diversifier. At Capital Group, we don’t buy physical gold or gold ETFs. Instead, I prefer to invest in companies that create value and can do better than if you had just owned gold. They are known as gold streamers: companies like Wheaton Precious Metals, Royal Gold and Franco Nevada. They are not miners. They are effectively finance companies. They make loans to copper miners or gold miners, and the loans are paid back in gold. All three companies have compounded their earnings per share 600 to 900 basis points a year faster than the increase in gold prices. And so they've done exactly what you would want. They have provided the traditional gold hedge while also contributing substantially to growth of capital.

Central banks have been the key to rising prices

— Lisa Thompson, portfolio manager, New World Fund®

Central banks are what I call price-insensitive buyers. They are not investing in gold to beat an index. They have an entirely different objective. They are trying to diversify their reserve base. They tend to be focused on risk and liquidity. When they adjust their asset allocation strategy, they don’t care about the price. In my view, that’s been the primary driver of gold prices over the past three years. It started with Russia and has extended to many other emerging markets, China being a notable example. But even in markets like Poland, you’re starting to see this desire to diversify into gold and away from the U.S. dollar.

It’s difficult to speculate on motives but, obviously, the world is changing. They might be worried about the stability of fiat currency, or that we are moving into a multipolar world, or lots of other geopolitical issues. They're not necessarily dumping U.S. Treasuries, but with their incremental reserves, they clearly are diversifying. Some are being more aggressive, some less. That is a totally different demand driver than anything we’ve seen in the past 30 years.

I think it’s a very important change. Will it last forever? No, of course not. But for now, there is just a structural demand for gold — and that is supporting gold prices. Keep in mind, near term, gold can be very volatile. It can move up and down sharply on a day-to-day basis. But I think we are seeing a different set of price parameters now than we were a few years ago.

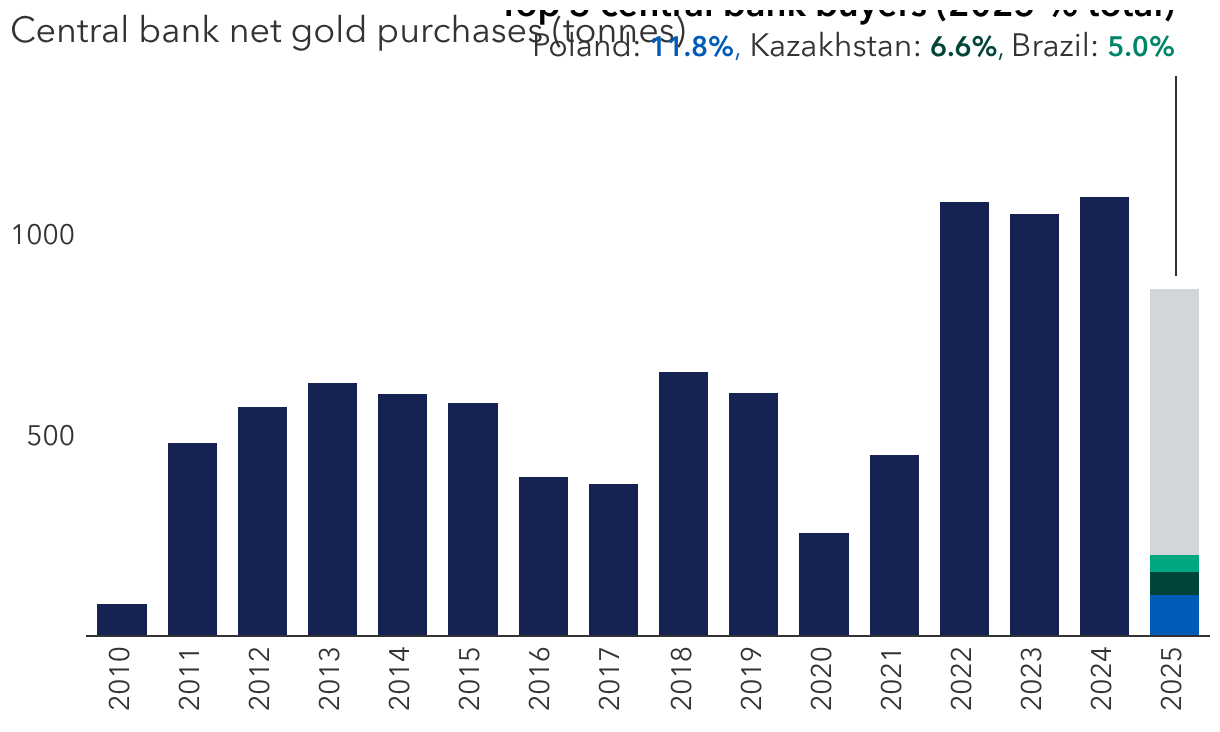

Since 2022, central bank gold buying has increased dramatically

Sources: Capital Group, World Gold Council, International Monetary Fund, and respective central banks. 1 tonne = 1,000 kilograms. Data as of December 31, 2025, where available.

Don’t be surprised if gold disappoints

— Rob Lovelace, portfolio manager, New Perspective Fund®

Over time, gold provides normative to no creation in value. It’s a commodity that is primarily a store of wealth. In recent years, the largest buyers of gold have been central banks. However, prior to this buying activity, central banks for many decades had been divesting gold because it's not a very useful asset. It doesn't pay interest. It doesn’t compound. In fact, physical gold essentially has a tax on it because you have to bury it in a secure place and hire guards to protect it. So it actually has a negative income, especially at scale.

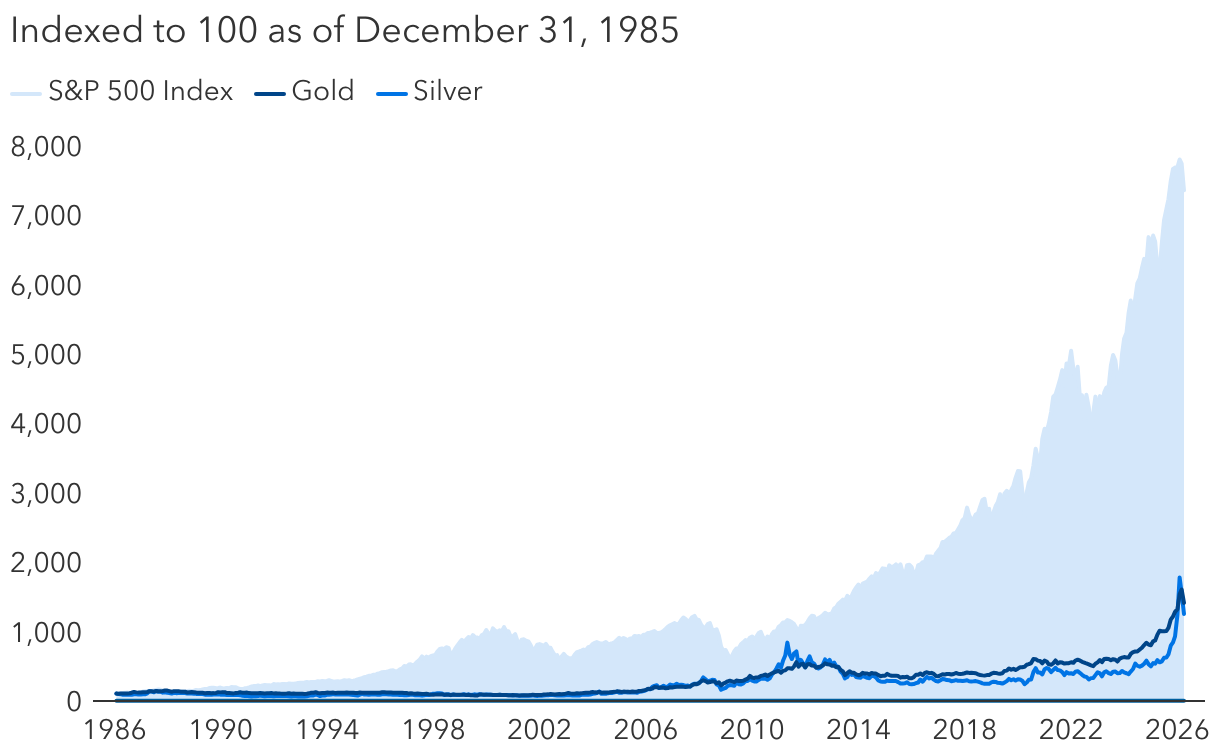

U.S. stocks have outpaced precious metals over the long term

Sources: Capital Group, ICE, London Bullion Market Association (LBMA), LSEG Workspace, Standard & Poor's. S&P 500 returns reflect total returns (with dividends reinvested). Gold and silver reflect LBMA prices per troy ounce in U.S. dollars. Figures shown are monthly from January 31, 1986, through March 31, 2026.

A few years ago, central banks were more interested in owning interest-bearing instruments, and the U.S. dollar was seen as safe and secure. As confidence in the dollar has waned over the past few years, central bank gold buying has increased. I would attribute much of the current run in gold prices to this asset allocation decision that many central banks — almost entirely outside the U.S. — have made to hold fewer dollars and more gold. At a certain point, they will have all the gold they need. They will no longer be buyers. And since there's a constant stream of new gold coming into the market from gold mines, at a rate of about 1% or 2% a year, you need to have a consistent, incremental buyer or the price will go down.

I have never used physical gold as an asset in my personal allocation mix, and I rarely use the indirect path of owning gold stocks or other gold-related investments in my portfolio. That said, throughout history, gold has served an important role as a store of wealth, as a currency, and as a hedge against inflation. In my view, gold is an asset of last resort. In essence, if everything goes wrong, at least I have the gold.

Past results are not predictive of results in future periods.

S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. The market index is unmanaged and, therefore, has no expenses. Investors cannot invest directly in an index.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The S&P 500 Index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Our latest insights

-

-

Demographics & Culture

-

-

Global Equities

-

Target Date

RELATED INSIGHTS

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.