Politics

Jayme Colosimo

Jayme Colosimo

Matt Miller

Matt Miller

Don't miss our latest insights.

- Geopolitical risk is becoming a standing feature of the macro backdrop, not a temporary disruption.

- Its effects extend beyond headlines, influencing growth, inflation, policy and the structure of the global economy.

- Markets often look through individual shocks, but that becomes harder when risks overlap and reinforce one another.

Markets have long tended to treat geopolitical risk as episodic, often viewing shocks as temporary disruptions that fade as growth reasserts itself. While that pattern still holds in many historical episodes, the current environment reflects a more structural shift, with a series of overlapping geopolitical pressures increasingly shaping the macroeconomic outlook.

The baseline is of a global economy still growing under strain: U.S. activity remains relatively resilient, supported in part by AI-related investment, even as the Iran conflict keeps energy markets unsettled, oil prices higher than before the war, and trade flows slower to normalize. At the same time, the global cycle is becoming less synchronized and more conditional.

From a regional standpoint, Europe has weakened under the energy shock but would likely recover quickly if conditions stabilize. China is showing tentative signs of stabilization; Japan is facing a more stagflationary backdrop and India appears more exposed to higher energy costs. That leaves a world in which growth is slowing but not breaking, inflation pressures remain sticky, policy paths are less straightforward and the range of outcomes is becoming more asymmetric. Market reactions to geopolitical developments may still be short lived, but the underlying economic effects can continue to build through growth, inflation, policy and the structural realignment of economies.

From isolated shocks to a more complex global system

Ongoing conflict in the Middle East, U.S. China trade and technology competition, Russia-Ukraine hostilities, and broader fragmentation across major economies are reinforcing one another. The issue today is less any single event and more the growing fragility of the systems that link the world’s trade flows, capital movement, technology transfer and energy supply.

A growing emphasis on supply chain resilience and strategic self-sufficiency is driving firms and governments to reconfigure production and sourcing, reinforcing a more fragmented global system and reshaping cross-border trade and capital flows. When issues are no longer simply episodic, fading geopolitical risk becomes less straightforward.

Markets react quickly, while underlying risks evolve more slowly

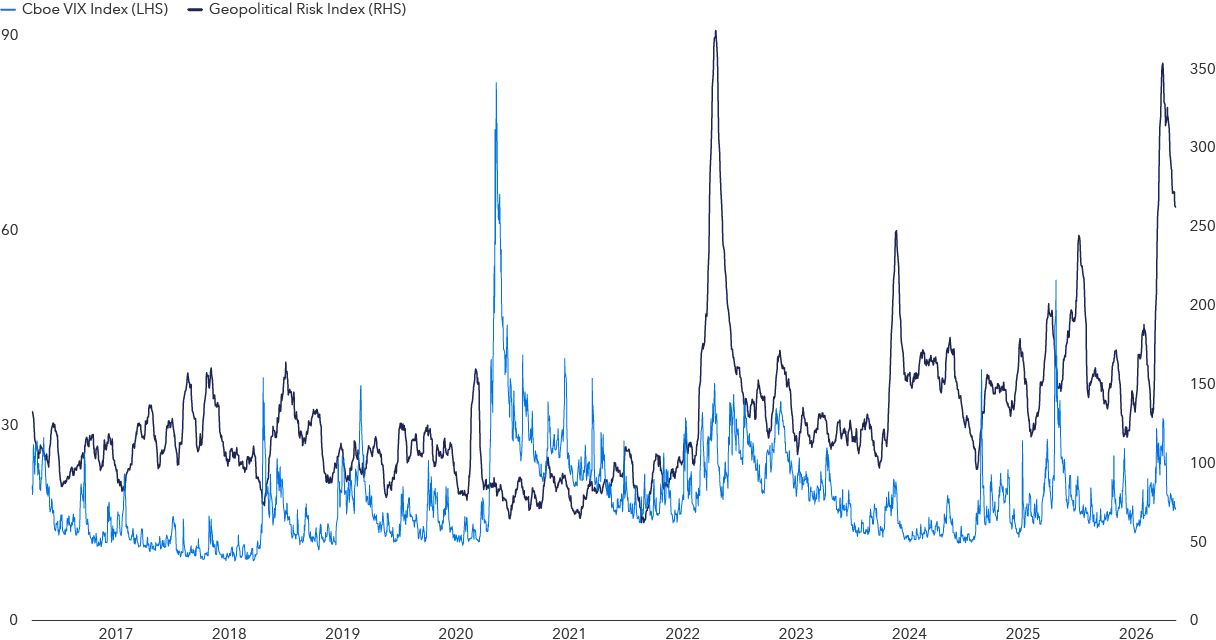

This risk persists, and is surfacing frequently, even as markets tend to treat episodes as temporary. One measure of such risk is the Geopolitical Risk Index (GPR), a gauge of geopolitical tensions and their associated risks. Such a measure moves in longer, sustained cycles with repeated spikes, suggesting an elevated risk backdrop. In contrast, the VIX (a gauge used to track investor sentiment and perceived risk) reacts in short, episodic bursts that typically mean-revert quickly. The result is a visible gap between the underlying risk environment and market-implied volatility.

Focusing on indicators like the VIX as a near-term, market-implied measure of volatility, risks overlooking the persistence of geopolitical pressures that can accumulate and ultimately transmit into growth, inflation and policy. When that transmission occurs, economic challenges tend to be more durable, not transient.

Rising global tensions have uneven impact on market volatility

Why the pathway matters as much as the shock

This distinction is central to the current macro backdrop. It is not necessarily the frequency of discrete shocks, but the pathway through which they propagate that drives market outcomes and investment implications. Increasingly, markets are less challenged by discrete events and more by a shifting regime in which geopolitical pressures more consistently feed into inflation, policy constraints and global economic fragmentation. As a result, attention shifts from short-lived market stress to how these pressures move through the real economy.

How geopolitical risks flow through the economy

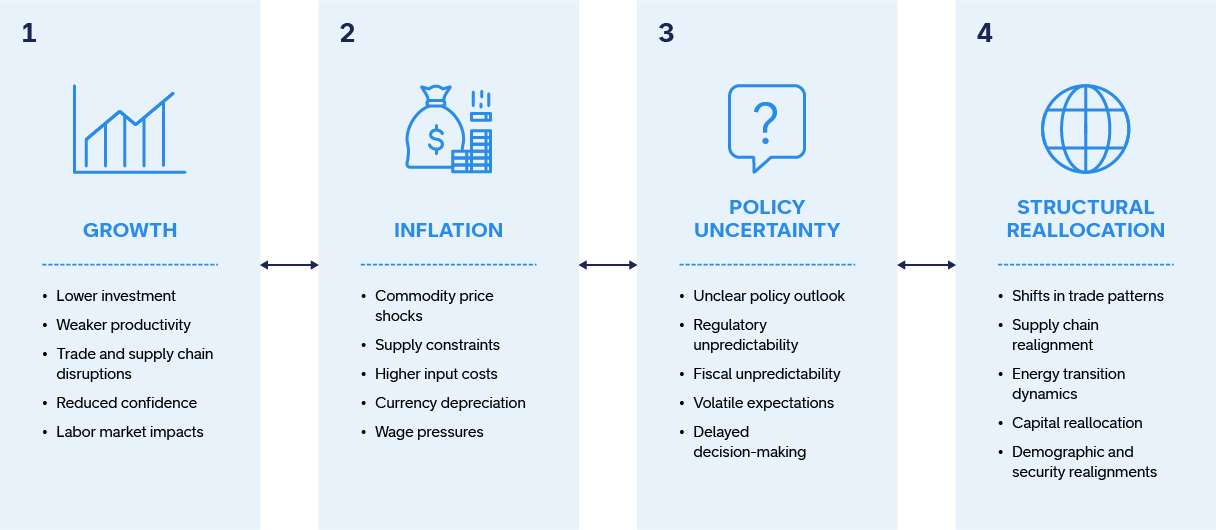

Geopolitical shocks become investment-relevant when they transmit into core economic variables that reprice assets. Four channels can shape that transmission. These are not exhaustive, but they provide a useful framework for understanding how geopolitical pressures propagate through the economy.

1. Growth. When geopolitical developments weaken confidence, disrupt investment or slow consumption, growth expectations decline and risk assets come under pressure. Historically, high-quality duration can provide diversification in these episodes — but only if inflation remains contained, which is often not the case when the shock originates in commodity markets or trade disruption. When growth and inflation channels activate together, the hedging properties of traditional fixed income may erode, making portfolio construction materially more difficult.

2. Inflation. Shocks that raise energy prices, increase input costs or introduce trade frictions can create stagflationary pressure. Even where headline inflation moderates, underlying pressures may remain persistent, reflecting second round effects from energy shocks and ongoing input cost pass-through across supply chains. This is often the most challenging outcome for portfolios, as both equities and bonds can come under pressure simultaneously.

3. Policy uncertainty. When the direction of tariffs, sanctions, regulation or industrial policy is unclear, companies may delay capital expenditure and hiring. The resulting drag on activity may be gradual but persistent, potentially widening risk premia and weighing on growth over time. Because this type of impact may accumulate slowly, it is often underpriced by market

4. Structural realignment. Geopolitical pressures can encourage companies and countries to reorganize supply chains, redirect capital flows and prioritize national security over efficiency. An increasing focus on supply chain resilience and strategic self-sufficiency is prompting firms and governments to rethink how and where goods are produced and sourced, contributing to a more fragmented global system and reshaping cross-border trade and capital flows.

How geopolitical shocks feed into the economy and policy

These forces rarely act in isolation. Growth and inflation outcomes increasingly reflect overlapping supply disruptions, policy responses and shifts in confidence. As supply chains are reconfigured in pursuit of resilience and self-sufficiency, these adjustments can reinforce fragmentation while extending the duration of inflationary pressures.

Positioning in a more fragmented world

Portfolio diversification is increasingly complex. With policy paths and growth outcomes diverging across regions, market performance is increasingly driven by dispersion rather than broad directional moves.

International exposure remains important and the emphasis is shifting from allocation to selection. Valuations, currencies, and policy divergence are creating opportunities — but exposures need to reflect where companies operate and generate earnings, not simply where they are listed. Economic conditions are diverging, with relatively resilient U.S. growth for now, a weaker, energy‑sensitive backdrop in Europe, with scope for recovery if conditions stabilize and tentative signs of stabilization in domestic demand in China.

Higher starting yields are reestablishing fixed income’s role not just as portfolio ballast, but as a meaningful source of income potential. That higher income can also help support returns even as certain geopolitical conflicts can add uncertainty to growth and inflation.

Within equities, outcomes are becoming more dispersed, with index concentration masking a widening gap between companies. Resilient margins, pricing power, and diversified supply chains matter more as the operating backdrop fragments. Dividend-paying companies with durable cash flows can provide a source of return potential that complements fixed income, particularly in an inflationary environment where income consistency matters.

When constructing portfolios over the longer term, understanding how geopolitical risks transmit through the real economy becomes as important as identifying the risks themselves.

Duration measures a bond’s sensitivity to changes in interest rates. Generally speaking, a bond's price will go up 1% for every year of duration if interest rates fall by 1% or down 1% for every year of duration if interest rates rise by 1%.

Stagflation is an economic condition characterized by slowing economic growth, high unemployment and rising prices that occur simultaneously.

Our latest insights

-

-

Demographics & Culture

-

Demographics & Culture

-

Artificial Intelligence

-

RELATED INSIGHTS

-

U.S. Equities

-

Emerging Markets

-

Global Equities

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week