Demographics & Culture

Categories

Artificial Intelligence

Why AI will transform, not replace, your job

Chris Buchbinder

Chris Buchbinder

Mark Casey

Mark Casey

Steve Watson

Steve Watson

Rob Lovelace

Rob Lovelace

Jared Franz

Jared Franz

May 21, 2026

Don't miss our latest insights.

Ask ChatGPT whether layoffs at Big Tech companies are a preview of what’s coming for everyone else, and its answer is as clear as mud: Not yet. But the warning signs are real.

Companies outside the tech sector are using artificial intelligence for a growing list of tasks, from reading legal documents, to creating marketing materials, and even conducting job interviews. Whether that’s enhancing or replacing human work is a question our economists and portfolio managers are grappling with.

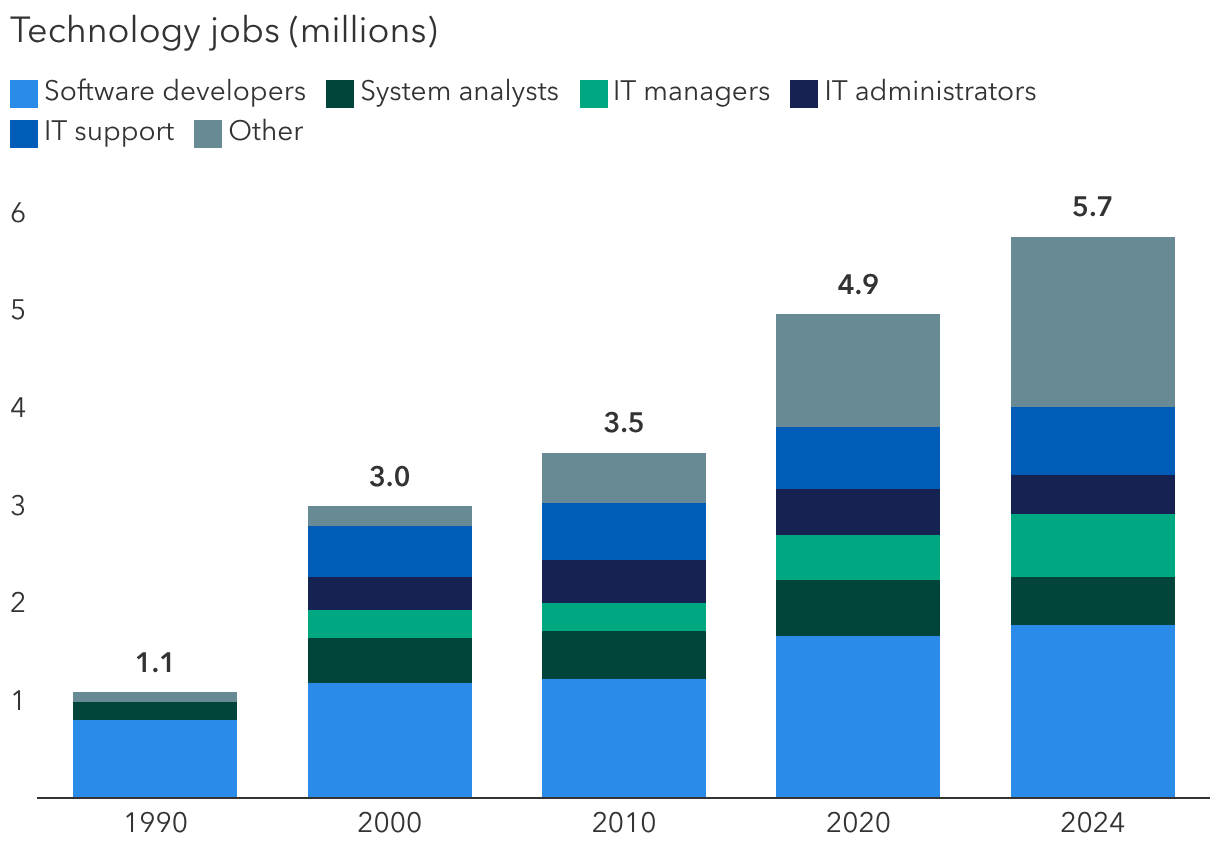

For many of them, AI is seen more as a long-term job creator than a job destroyer. “I have no doubt that AI is going to dramatically transform our lives and eventually touch most of the economy,” says Chris Buchbinder, portfolio manager for CGVV — Capital Group U.S. Large Value ETF. “Some have argued this is going to lead to large-scale white-collar job loss, and those concerns reflect real anxiety for many workers. But I believe that is far too pessimistic, and that is not my view. It’s also not consistent with the history of productivity enhancing technology.”

Instead, AI is likely to drive faster economic growth and a surge of new businesses. “As a telecom analyst in the late 1990s, I saw the internet create all kinds of new companies and jobs. It was unimaginable that Amazon would become a retail giant, Netflix would overtake much of the media industry, or online advertising would surpass traditional channels,” Buchbinder explains. “We’re at that same stage now. The next generation of AI companies and use cases will be just as hard to predict and just as transformative.”

Internet boom created new, highly skilled jobs

Sources: Capital Group, Bureau of Labor Statistics. Latest data available is 2024 as of May 14, 2026. Tech jobs data compiled from Occupational Employment and Wage Statistics (OEWS) and classified using the Standard Occupational Classification (SOC) system.

Most industries bolt new tech to old systems

Technological advances rarely change industries overnight. It took a pandemic for widespread adoption of video conferencing, a technology that AT&T debuted in 1927 and improved upon into the 1990s. “There is plenty of technology available that industries and companies aren’t using because integration with the real world is messy and often requires rethinking entire business processes,” says economist Jared Franz.

Industries including construction, healthcare, aerospace and defense, and financials are likely to adopt AI more gradually. That’s because many companies in these industries rely on complex, difficult-to-integrate legacy systems, with data often fragmented.

Historically, companies tend to adopt new technologies by bolting them to existing systems. “You don’t want an AI system to make a medical diagnosis without human input, especially in radiology and other potentially life-altering situations,” Franz says.

Automation has expanded work for radiologists

Sources: Capital Group, Centers for Medicare & Medicaid Services, Medscape. As of May 18, 2026.

That may explain why there are more radiologists today than 10 years ago, when AI pioneer Geoffrey Hinton warned that the job would become obsolete. “We should stop training radiologists now. It’s just completely obvious that within five years, deep learning is going to do better than radiologists,” he stated. Although Hinton accurately predicted automation advances, the number of radiologists and their pay increased as demand for scans jumped.

OpenAI, Google and others are working to lower their AI systems’ hallucination rates, or how often they respond with incorrect or fabricated information. The bar is high. “It’s not that AI has to be better than humans,” Franz says. “In certain settings, it must be 10 times better or with close to zero errors. As a result, there’s still debate about whether today’s dominant AI systems, which are built on large language models, are suited for high-stakes tasks.”

Companies have bottlenecks to widespread AI adoption

It may be hard for AI to devour certain jobs simply because there are too many bottlenecks across corporate America. “Workers may draft, code, summarize and screen faster, but they may still be constrained by bottlenecks such as industry or government regulation, physical capacity and management bandwidth,” Franz explains. “A worker that is twice as productive doesn’t make a company twice as productive.”

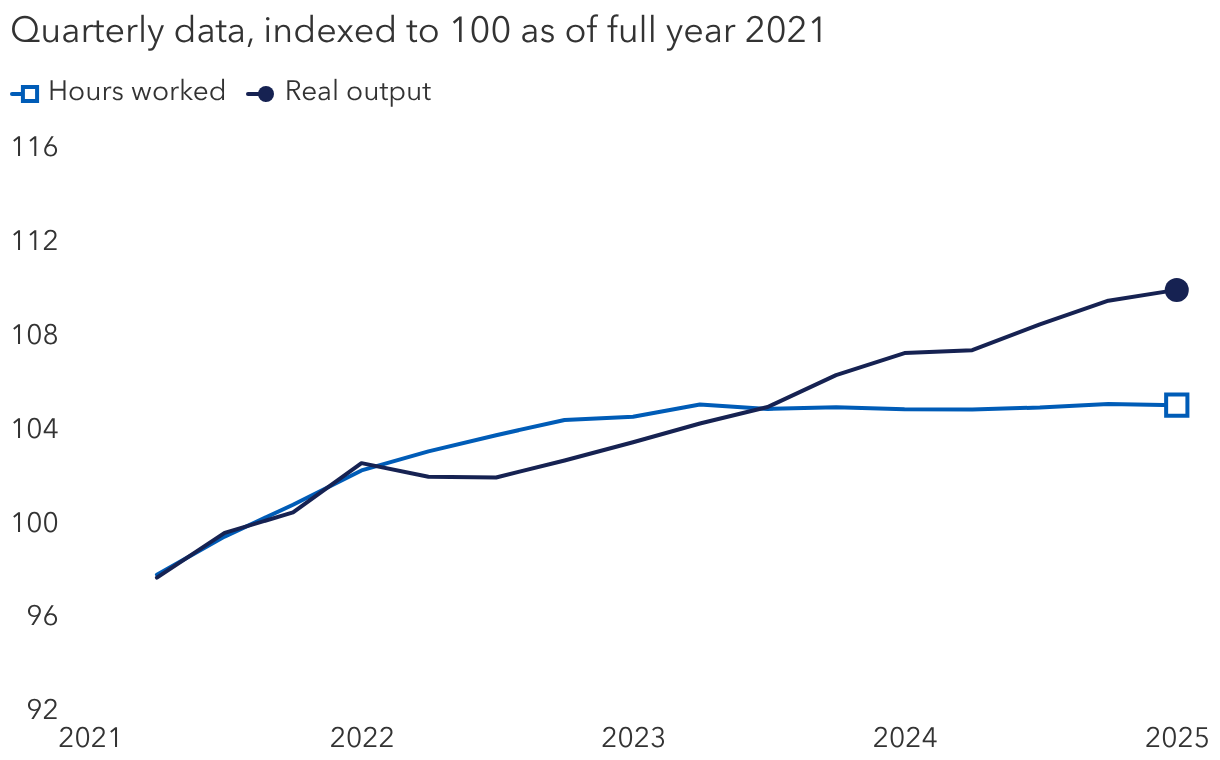

U.S. output has been on the rise

Sources: Capital Group, Haver Analytics, U.S. Bureau of Labor Statistics. Indexed to 100 in 2021. Latest data available is for fourth quarter 2025 as of March 16, 2026.

Franz notes five criteria must be met for companies to potentially benefit from AI productivity gains:

- The task being improved must matter to the company’s overall output.

- The gain must be captured by the firm rather than retain a private advantage for the employee.

- The surrounding workflow must scale alongside it.

- Managers must be willing to reorganize how work gets done.

- Competitors cannot immediately force those gains to be passed to customers.

“If any one of those breaks, then worker-level improvement does not show up one for one in company profits, overall production, or macroeconomic data,” Franz adds.

Franz believes AI productivity gains are likely to be uneven, creating what he calls a jagged edge across the economy. Some companies will experience company-wide improvements, particularly in areas like customer support, insurance claims processing and select software workflows.

In other corners of the economy, AI’s impact may be smaller. “Elite legal and advisory work, health and medicine, and organizations where the hard part isn’t producing more things but converting analysis into high-quality decisions may experience much lower gains from AI,” Franz concludes.

AI systems are nowhere near human intelligence

In certain tests, AI systems can outperform humans with PhDs, but that is not the kind of intelligence that replaces human work, according to Mark Casey, a portfolio manager for CGGG — Capital Group U.S. Large Growth ETF and CGGR — Capital Group Growth ETF. “AI systems are pattern recognizers and producers. They don't have a grasp of what a bicycle or bicycle seat is. They're making statistically valid guesses, but they're still guesses.”

According to Casey, AI innovation has a long way to go before it can reliably replace humans in many real-world tasks. “Simple changes to the context of basic games such as tic-tac-toe or tasks requiring an understanding of how the world works expose their limitations,” he says. This leaves a wide gap for humans to fill based on their experience, understanding of context and creativity.

“People who work with words and numbers may feel especially exposed given how these machines are optimized to produce both,” Casey explains. “But success isn’t defined by the ability to write or code. Instead, the hardest part is figuring out what customers want and how to deliver on those needs.”

Most layoffs aren’t AI-related

Warnings of an AI-fueled jobs apocalypse are likely overstated. “We are still in the early stages of AI implementation, and many companies don’t know what the impact will be on employee productivity,” says Steve Watson, portfolio manager for CGIC — Capital Group International Core Equity ETF. “I would take announcements of AI-related job losses with a dose of skepticism. Generally, the reasons for head count reductions are less about AI and more about business fundamentals, including increased competition and higher cost pressures.”

Several companies across technology, e-commerce and finance hired aggressively during the pandemic to meet surging demand. Those same companies likely found themselves overstaffed as demand cooled and interest rates rose. “AI offers a convenient explanation for cuts already justified by lower earnings growth and a more normalized consumer spending pattern,” Watson adds.

“Executives are attuned to their stock prices and would rather say ‘we are reaping the benefits of AI implementation and therefore will be a leaner company,’ rather than admit their margins and business segments may be suffering.”

Vibe coding has its limits

The impact of AI on the labor market is a theme that touches every business, sector and geography. For consulting and software companies, there are existential questions about whether their customer base will continue to outsource, says Rob Lovelace, portfolio manager for New Perspective Fund®.

The answer may depend on who you ask. CEOs often suggest outsourcing and hiring may decline, while chief technology officers are more guarded. “They’re seeing that we may actually just be hiring different types of consultants and workers to help us. The reality may be that the complexity of work has shifted elsewhere, so companies may need to hire more people to do other things. Ultimately, the savings in time and efficiency will be large, but the reduction in head count may be a lot less than what everyone’s predicting AI will bring," Lovelace says.

There’s also the reality that most people don’t want to do everything themselves. Just as homeowners may watch YouTube videos to help them unclog a drain but still call a plumber to install a water heater, businesses may use AI tools but still rely on experts to get critical work done right. “Though information may be more readily available, the desire for expertise, efficiency and accountability keeps humans firmly in the driver’s seat,” Lovelace explains.

Learn more about

Real output: goods and services produced by the business sector adjusted for inflation.

Vibe coding: the ability to write code and build apps almost entirely with AI.

Our latest insights

-

-

-

Global Equities

-

Target Date

-

Demographics & Culture

RELATED INSIGHTS

-

-

Emerging Markets

-

Global Equities

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and/or summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.