Global Equities

Chris Buchbinder

Chris Buchbinder

Mark Casey

Mark Casey

Rob Lovelace

Rob Lovelace

Steve Watson

Steve Watson

Don't miss our latest insights.

Our latest insights

-

-

-

Demographics & Culture

-

-

Global Equities

- Earnings growth, not sentiment, is driving markets.

- The multiyear AI investment cycle is fueling growth across sectors, especially the “physical economy.”

- Non-U.S. markets offer attractive valuations and strong earnings potential relative to the U.S.

If you take your cues from the daily news headlines, you can find any number of reasons to feel squeamish about the stock market.

Those feelings may be misplaced, however. Thus far in 2026, stock markets have reached a series of new highs amid wars in the Middle East and Ukraine, fluctuating oil prices and elevated inflation. Why have stock markets shown such strength? It largely comes down to a simple yet critical factor: Corporate earnings are on a tear.

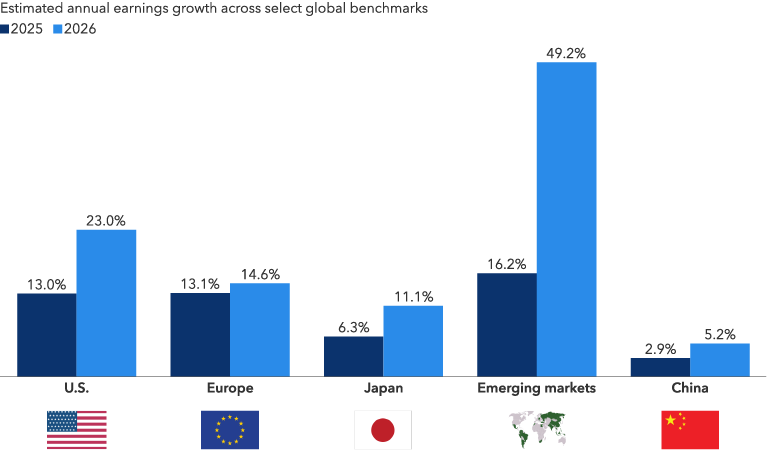

The artificial intelligence juggernaut accounts for much of the good news. Aggressive spending by technology companies has translated into revenue and earnings growth for companies across sectors. But there’s much more to the story than AI growth. Banks are capitalizing on higher interest rates, innovative therapies are driving sales growth in healthcare, and higher crude oil prices are pumping up energy companies. Looking forward, consensus earnings estimates reflect continued strength, particularly in emerging markets, where they are expected to soar 49.2% by year’s end.

Robust earnings growth is not just a U.S. phenomenon

Sources: Capital Group, FactSet, MSCI, S&P Global. Estimated annual earnings growth is represented by the mean industry analyst consensus earnings per share estimates for the year ending December 2026 across the S&P 500 Index (U.S.), the MSCI Europe Index (Europe), the MSCI Japan Index (Japan), the MSCI EM Index (Emerging markets) and MSCI China Index (China). Earnings growth represented in USD. Estimates are as of May 31, 2026.

“When I look at the market going forward, the key element is this underpinning of strong corporate earnings,” says Rob Lovelace, Chair of Capital International, Inc. and an equity portfolio manager for New Perspective Fund®. “This growth has been evident for the last three years, and it doesn’t look like it’s slowing down.”

Here are three equity market themes we are focused on for the remainder of 2026 and beyond.

1. The AI freight train shows no signs of slowing

In the race for AI supremacy, five hyperscalers — Amazon, Alphabet, Meta, Microsoft and Oracle — have committed to investing $650 billion this year on data centers, a historic level of spending that doesn’t appear to be slowing. “These investments are being led by some of the most profitable companies the world has seen,” says equity portfolio manager Mark Casey. “As long as the technology keeps advancing, I expect they’ll continue to invest.”

Indeed, total global investment in AI infrastructure and AI-related products could reach $30 trillion over the next decade, eclipsing China’s industrial boom of the early 2000s, considered by many to be the largest in modern history. That boom reshaped global trade, labor markets and politics, suggesting AI may be much bigger than a sector story.

“In the first half of the year, the Iran war seemed to block out the sun,” says Mark Casey, equity portfolio manager for The Growth Fund of America®. “But I think AI still is the sun in the sense that it is potentially the highest impact technology in a generation and the most significant force in the economy.”

All this spending has translated into soaring demand for advanced semiconductor makers like NVIDIA and Broadcom as well as semiconductor foundries like Taiwan Semiconductor Manufacturing Company (TSMC) and networking companies like Cisco Systems, for example.

With technology advancing so rapidly and the build-out likely stretching years into the future, the epicenter of demand could shift among various hardware suppliers. That’s why selective investing is essential, Casey adds.

2. Look beyond U.S. borders for magnificence

Think the AI story is the exclusive domain of U.S. tech giants? Think again.

Just as the Magnificent Seven have led U.S. markets, seven companies that play a key role in the AI revolution are also dominating emerging markets. TSMC, Samsung Electronics and SK hynix are common names, but lesser-known companies MediaTek and Delta Electronics are also asserting leadership. Tencent and Alibaba have access to the largest market in the world by operating in China.

As in the U.S., seven tech stocks have dominated emerging markets

Sources: Capital Group, MSCI, RIMES, FactSet. Emergent Seven represents the seven largest companies in the MSCI Emerging Markets Index: Taiwan Semiconductor Manufacturing, Samsung Electronics, SK Hynix, Tencent, Alibaba, MediaTek and Delta Electronics. The Magnificent Seven refers to a group of seven dominant U.S.-based technology companies: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla. The forward 12-month price-to-earnings (P/E) ratio divides the current share price of a company by the estimated future earnings per share of that company. Tesla’s forward 12-month P/E of 220x places it outside of the graph axis and is thus excluded above. As of May 31, 2026.

These seven tech and platform companies are the largest by market capitalization in the MSCI Emerging Markets Index, making up 33% of the index. At Capital we refer to them as the “Emergent” Seven. They generally have smaller market capitalizations and lower valuations than many of their U.S. counterparts, but they are generating earnings growth expectations beyond those for the S&P 500.

Investors focused on U.S. equities may not fully grasp the scope of these opportunities. “Now many global leaders in their industries can be found outside the United States,” says Steve Watson, equity portfolio manager for New Perspective Fund®.

More broadly, a powerful rally in emerging and developed non-U.S. markets that started in 2025 continues, driven by attractive valuations, a weak dollar and strong corporate earnings. Although U.S. stocks have narrowed the gap, Watson expects further opportunity in non-U.S. markets, citing as examples industry leaders like Airbus, ASML, AstraZeneca and Safran as headquartered beyond U.S. borders.

3. The physical economy is flexing its muscles

While AI may be the biggest driver of stock markets — after all, NVIDIA’s market capitalization alone has grown larger than three S&P 500 Index sectors — ignoring companies in the physical economy could be a mistake.

NVIDIA is larger than three S&P 500 Index sectors

Sources: Capital Group, S&P Global, FactSet, RIMES. As of May 31, 2026. Companies shown are the three largest in their respective sectors within the S&P 500 Index.

To begin with, AI can’t run without the physical economy. Demand for steel, copper, heavy construction services and power generation equipment is soaring in support of the data center build-out. For instance, sales in Caterpillar’s construction division jumped 38% in the first quarter. The company also reported an order backlog of $62.7 billion for power generation equipment.

“Pick-and-shovel companies, both the semiconductor supply chain and the infrastructure developers, are where I see the clearest opportunity,” says Chris Buchbinder, principal investment officer for The Investment Company of America®.

Others are attractive because they are unlikely to be disrupted by AI. “Consider, for example, Royal Caribbean. I don’t see AI replacing cruise ships,” Buchbinder explains. Another example is jet engine maker GE Aerospace, which entered the year with a $190 billion order backlog, driven by rising global demand for travel and greater defense spending.

In addition, investors concerned about rising risks may want to consider investing in some physical economy companies with a history of paying dividends. Many drugmakers, for example, generate healthy free cash flow that allows them to return capital to shareholders through dividends while strengthening their pipelines through targeted acquisitions. For example, pharmaceutical company AstraZeneca has a well-established range of oncology franchises. To drive future growth potential, it has assets targeting heart disease, chronic kidney conditions and metabolic disorders.

The bottom line for investors

To be sure, investors are confronted with risks heading into the back half of the year. Not least of them are soaring energy prices, elevated inflation and high valuations in certain sectors. But every year offers its own unique mix of risks and opportunities. Indeed, the market volatility immediately after the start of the Iran War in late February is a reminder that maintaining well-diversified, balanced portfolios is crucial in any market environment.

Hyperscalers are large-scale cloud service providers that offer computing power and storage to organizations and individuals globally.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging markets (EM) countries.

S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

The S&P 500 Index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

RELATED INSIGHTS

-

Emerging Markets

-

Global Equities

-

World Markets Review

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week