Municipal Bonds

Categories

Fed

How might Kevin Warsh steer the Fed?

Tom Hollenberg

Tom Hollenberg

Doug Kletter

Doug Kletter

May 13, 2026

Don't miss our latest insights.

Kevin Warsh is stepping into the top spot at the Federal Reserve at a challenging moment. Inflation has risen amid the U.S.-Iran conflict, labor markets are uneven and signs of growing internal dissent within the Fed are emerging. Against this backdrop, the path to lower interest rates has become less clear, raising the stakes for both policy decisions and market expectations.

Importantly, Jerome Powell indicated he’ll remain on the Fed’s Board of Governors until the investigation of the Fed building renovation is complete. Members of our fixed income investment team continue to expect institutional continuity at the Fed, which should limit political influence over the central bank.

The collective judgment of the Federal Open Market Committee (FOMC) and the Board of Governors remains central to policymaking. Governors serve staggered 14-year terms that deliberately extend across multiple presidential administrations, providing insulation from short-term political pressures and limiting the extent to which any single chair can unilaterally redirect policy.

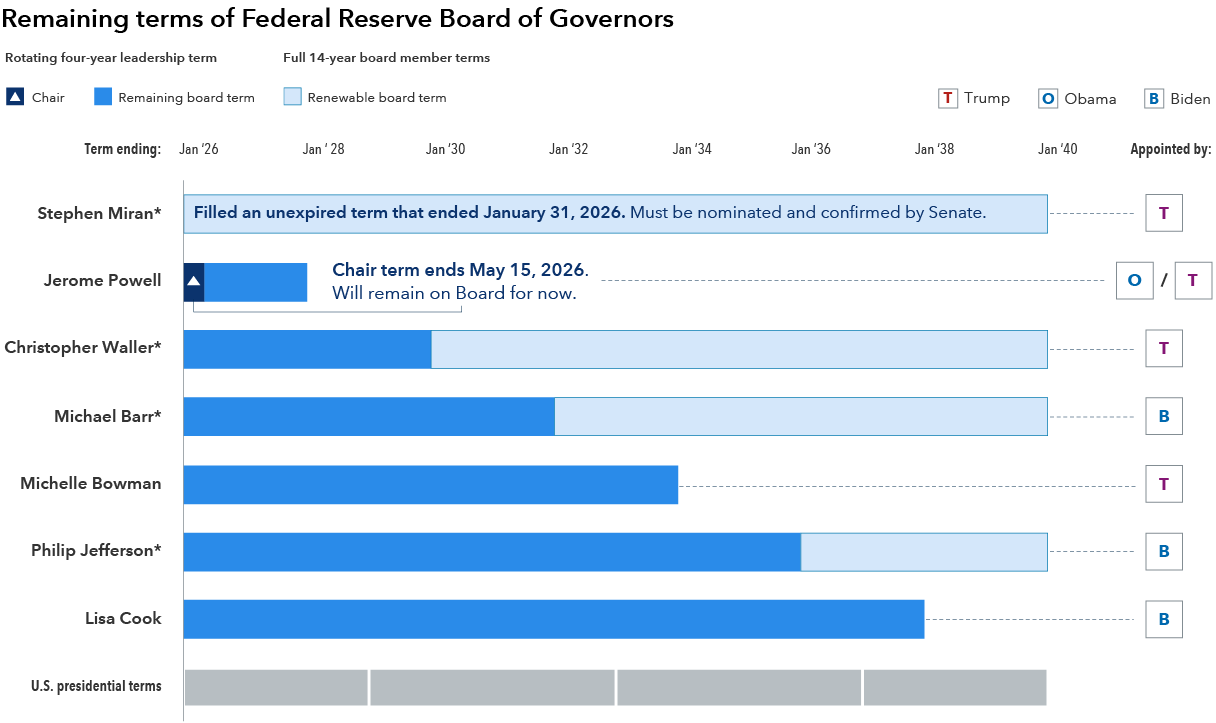

Institutional design of the Fed board favors continuity

Sources: Capital Group, Brookings, Federal Reserve. *A member of the Federal Reserve Board of Governors who is completing an unexpired portion of a prior member's 14-year term may be reappointed. Members and leadership positions are nominated by the U.S. president and confirmed by the U.S. Senate. President Trump nominee Stephan Miran had filled an unexpired term that ended January 31, 2026. Jerome Powell indicated during April Fed meeting he’ll remain on the board until investigation over Fed building renovation is complete. Renewable portion shown for illustration; reappointment is not automatic. As of January 30, 2026.

While leadership changes can shape messaging and risk tolerance at the margins, they do not override the existing monetary policy framework. Markets should focus on underlying fundamentals of the U.S. economy, rather than who the new Fed Chair is, as the main driver of monetary policy.

A Fed chair focused on rate cuts takes the reins

Rate cuts are still possible, but they face an increasing number of headwinds. High oil and gas prices have garnered headlines, though renewed supply chain pressures, including second-order effects from chemical and industrial inputs, could add modest upside to core personal consumption expenditures (PCE) in the coming months. These cost pressures are likely to squeeze consumer spending, which would slow growth. As a result, the Fed will be weighing a potential growth slowdown against elevated inflation over the next six to 12 months.

Market-based rate hike probabilities have increased since early this year; however, they could be overstated if wage growth and inflation expectations remain anchored. A sustained rate hiking cycle would likely require a more persistent inflation impulse, potentially driven by a combination of firm demand, tightening labor markets and a meaningful pickup in wage growth that challenges the current view of contained underlying inflation. Even in that scenario, our rates team views the probability of that outcome as a tail risk, closer to 10% than the higher levels implied by options markets, reinforcing the case for maintaining some duration exposure.

At the same time, inflation progress remains uneven. Core PCE was already sticky above 3% prior to the U.S.-Iran conflict, and underlying pressures remain a key focus for the FOMC. If the assumption that supply-driven shocks will fade without affecting wages or broader inflation proves incorrect, the Fed’s ability to remain patient could be tested. Until then, policy is likely to remain data-dependent, with a bias toward easing if disinflation unfolds.

Inflation expectations are elevated but within recent range

Source: Bloomberg. 5-year inflation is the 5-year zero-coupon inflation swap rate. As of May 7, 2026. New York Fed Survey of Consumer Expectations, median five-year ahead, as of April 2026.

Beyond interest rate cuts

Warsh may face an uphill battle in containing long-term interest rates given his views on the Fed’s balance sheet. While policy rates anchor the front end of the curve, longer dated yields are shaped by inflation expectations, fiscal dynamics, global demand for U.S. Treasuries and term premiums. Tools such as quantitative easing and Operation Twist put downward pressure on term premia and Warsh has been a critic of the Fed’s balance sheet size.

More broadly, compared with past cycles, the Fed is operating with more constrained policy levers. Policy rates remain barely restrictive while inflation is still above target, limiting the ability to ease preemptively. Additionally, bank reserves are at levels that have historically been thought of as Lowest Comfortable Level of Reserves (LCLoR), so if Warsh wanted to shrink the Fed’s balance sheet while easing rates, bank demand for reserves must fall. Bank deregulation could help accomplish this on a limited basis, but it would be a slow process where the Fed would want to proceed carefully.

The Fed retains tools such as its standing repo program and reserve management purchases of Treasury bills, which will be helpful in providing a safety net when trying to lower long-run reserve levels. The U.S. Treasury is also considering investing its cash balances in the repo market to dampen funding market volatility.

Elephant in the room: U.S. debt

U.S. federal debt now exceeds the size of the U.S. economy, and the government’s annual deficit is at levels traditionally associated with extraordinary periods such as COVID-19 or major wars. The scale of today’s debt burden and persistent large deficits raises important questions about how the Fed might navigate such an environment.

Elevated debt levels can constrain fiscal flexibility and increase market sensitivity to interest-rate movements, placing greater pressure on monetary policy to act as a stabilizer during market stress.

The size of the U.S. national debt is not weighing heavily on markets right now, perhaps because investors still see it as manageable or a longer-term issue that’s not as pressing as other near-term macro factors. Strong demand for Treasuries, the dollar’s central role in global finance, and consistent growth supported by AI investment all support confidence that the government can service its obligations.

For now, markets focus less on the size of the debt and more on whether it is becoming harder to finance. That could change if borrowing costs remain elevated, deficits do not contract or inflation credibility weakens. In that scenario, pressure would likely show up gradually through higher yields and volatility, tightening financial conditions. These factors, combined with the potential of a rapidly weakening dollar, if investors were to question its reserve currency status, could limit policymakers’ flexibility.

Bottom line

Ultimately, Warsh is entering a period constrained by a more uncertain inflation outlook, an uneven labor market, geopolitical pressures and elevated debt, all of which may limit policy flexibility. Although he is expected to differ from Powell in communication style, the path of policy will likely remain data-dependent and institutionally driven. The market no longer prices an easing bias from the Fed and we think this provides an opportunity to own duration provided wages and inflation expectations remain contained.

Learn more about

The value of fixed income securities may be affected by changing interest rates and changes in credit ratings of the securities.

Duration measures a bond’s sensitivity to changes in interest rates. Generally speaking, a bond's price will go up 1% for every year of duration if interest rates fall by 1% or down 1% for every year of duration if interest rates rise by 1%.

Operation Twist: A $400-billion program used by the Fed in 2011 to support long duration U.S. Treasuries by selling short-dated instruments while keeping its balance sheet unchanged in size.

Quantitative easing (QE): The Fed’s purchases of large quantities of Treasury securities and mortgage-backed securities issued by government-sponsored enterprises and federal agencies to achieve its monetary policy objectives.

RELATED INSIGHTS

-

-

Economic Indicators

-

Interest Rates

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and/or summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.