Time, not timing, is what matters

Investors learning how to invest in the stock market might ask when to invest. Knowing when to invest, however, isn’t as important as how long you stay invested.

Trying to navigate the peaks and valleys of market returns, investors seem to naturally want to jump in at the lows and cash out at the highs. But no one can predict when those will occur. Of course, we’d all like to avoid declines. The anxiety that keeps investors on the sidelines may save them that pain, but it may ensure they’ll miss the gain. Historically, each downturn has been followed by an eventual upswing, although there is no guarantee that will always happen.

The chart below shows two hypothetical investments in the S&P 500 Index over the 20-year period ending December 31, 2025. Each investor contributed $10,000 every year. One investor somehow managed to pick the very best day (the market low) of each year to invest. The average annual return on that investment would have been 14.65%. The other investor was not so lucky and actually picked the worst day (market high) each year. Even with the worst investment timing, the average annual return would have been 12.64%. At the end of 20 years, the cumulative investment of $200,000 had a value of $801,554.

So even selecting the worst day each year to invest, someone who continued investing in the market over the past 20 years would have come out ahead. It’s important to note that regular investing neither ensures a profit nor protects against a loss. However, the tables below illustrate how regular investing can be beneficial.

Timing isn’t critical to long-term success

Source: S&P 500 Index.

Riding it out

Note that the hypothetical investors above didn’t pull out of the market but stayed the course for 20 years. That perseverance helped improve the chances that they would come out ahead. In fact, history has shown that positive outcomes occur much more often over longer periods than shorter ones.

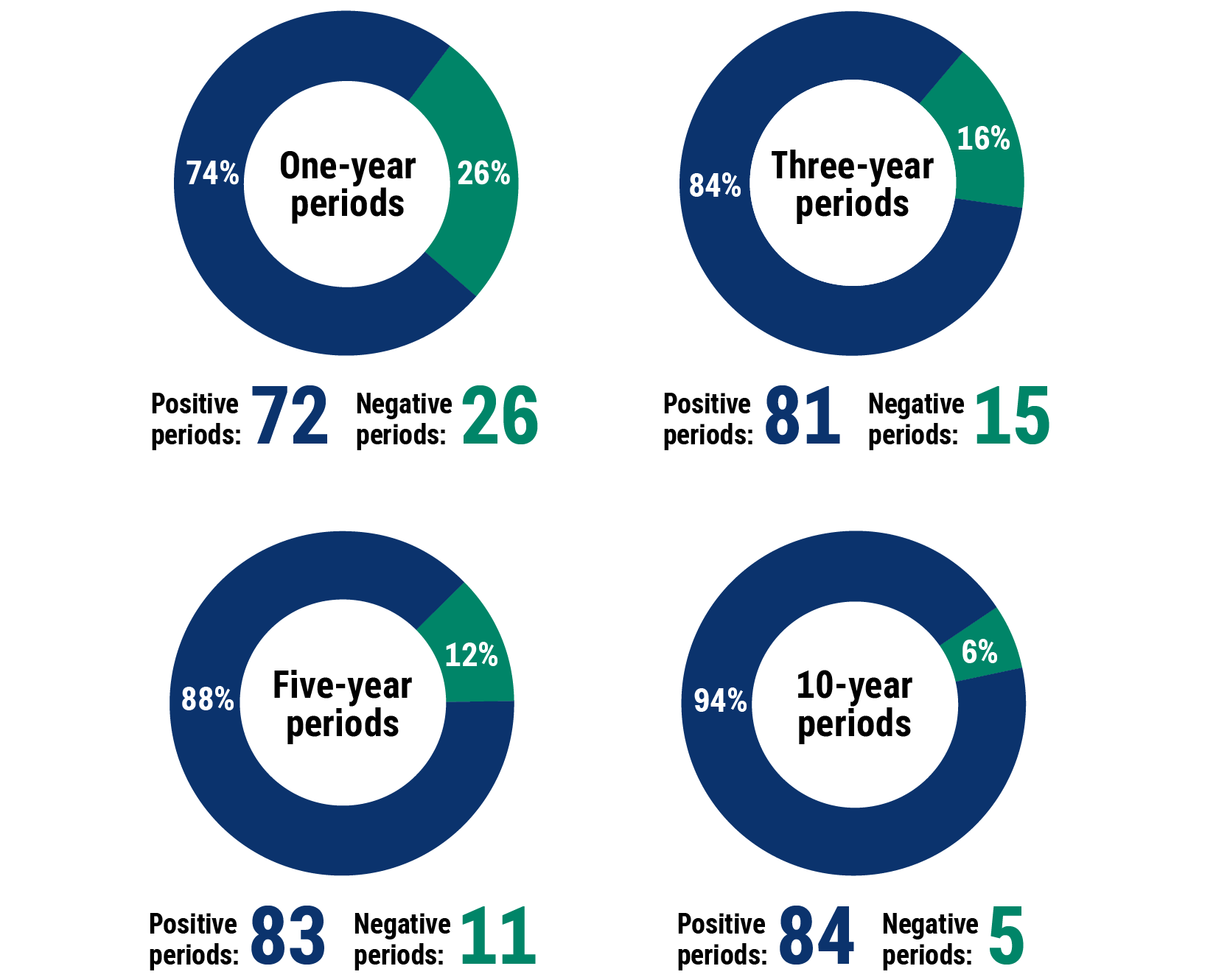

Over the past 98 years, the S&P 500 Index has gone up and down each year. In fact, 26% of those years had negative results. As you can see in the chart below, one-year investments produced negative results more often than investments held for longer periods. If those short-term one-year investors had held on for just two more years, they would have experienced nearly half as many negative periods.

And the longer the time frame — through highs and lows — the greater the chances of a positive outcome. Indeed, over the past 89 years, through December 31, 2025, 94% of 10-year periods have been positive ones. Investors who have stayed in the market through occasional (and inevitable) periods of declining stock prices historically have been rewarded for their long-term outlook.

History has shown the longer the period, the greater the chances of a positive outcome

Source: S&P 500 Index.

Rather than trying to predict highs and lows, it’s important to stay invested through a full market cycle. Focus on the time you stay invested, not the timing of your investments.

S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. The index is unmanaged and, therefore, has no expenses. Investors cannot invest directly in an index.

Each S&P Index ("Index") shown is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.