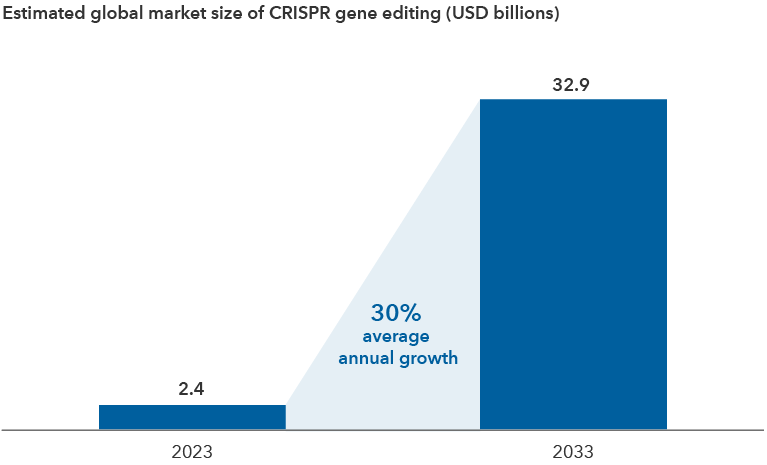

You’ve heard of computer hacking, now meet gene hacking. In an age of remarkable health care innovation, scientists are manipulating human DNA to find new ways to treat diseases.

They’ve moved from the lab to the real world with a treatment for the life-shortening disease sickle cell — the first approval based on a revolutionary gene-editing technology known as CRISPR.

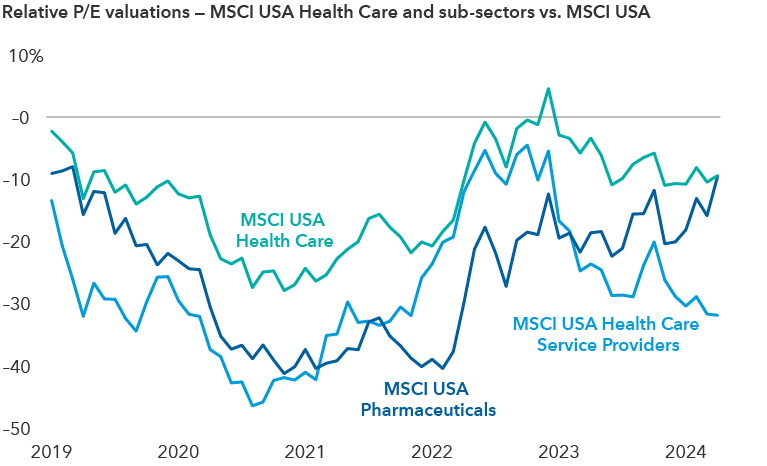

“Whether it’s biotechnology or medical devices, there has always been an important moment that has changed how investors view a new technology or therapy. It could be one major success or a series of successes, and we are seeing pockets of that now across health care,” says Rich Wolf, portfolio manager for The New Economy Fund®.