The status of the United States as the world’s largest producer of oil and gas and the fact that oil markets are pegged to the dollar remain critical advantages. Still, even with U.S. energy independence, this war confirms that the U.S. is not immune to oil price shocks since oil prices are set in the global market. As a result, energy security in some countries may be reframed to include a broader range of energy sources, such as an increased focus on renewables. Even in places like Japan there is a renewed interest in expanding nuclear.

China’s introduction of the petroyuan in 2018 has caused some concern that the dollar’s dominance as the international reserve currency may fade. I remain skeptical. The renminbi remains constrained by capital controls and limited convertibility, restrictions Beijing is unlikely to loosen meaningfully anytime soon. Central banks are likely to continue the trend of diversifying their foreign currency holdings to reduce dependence on the dollar, but I see no other currency as having the ability to displace the dollar as the single largest reserve currency.

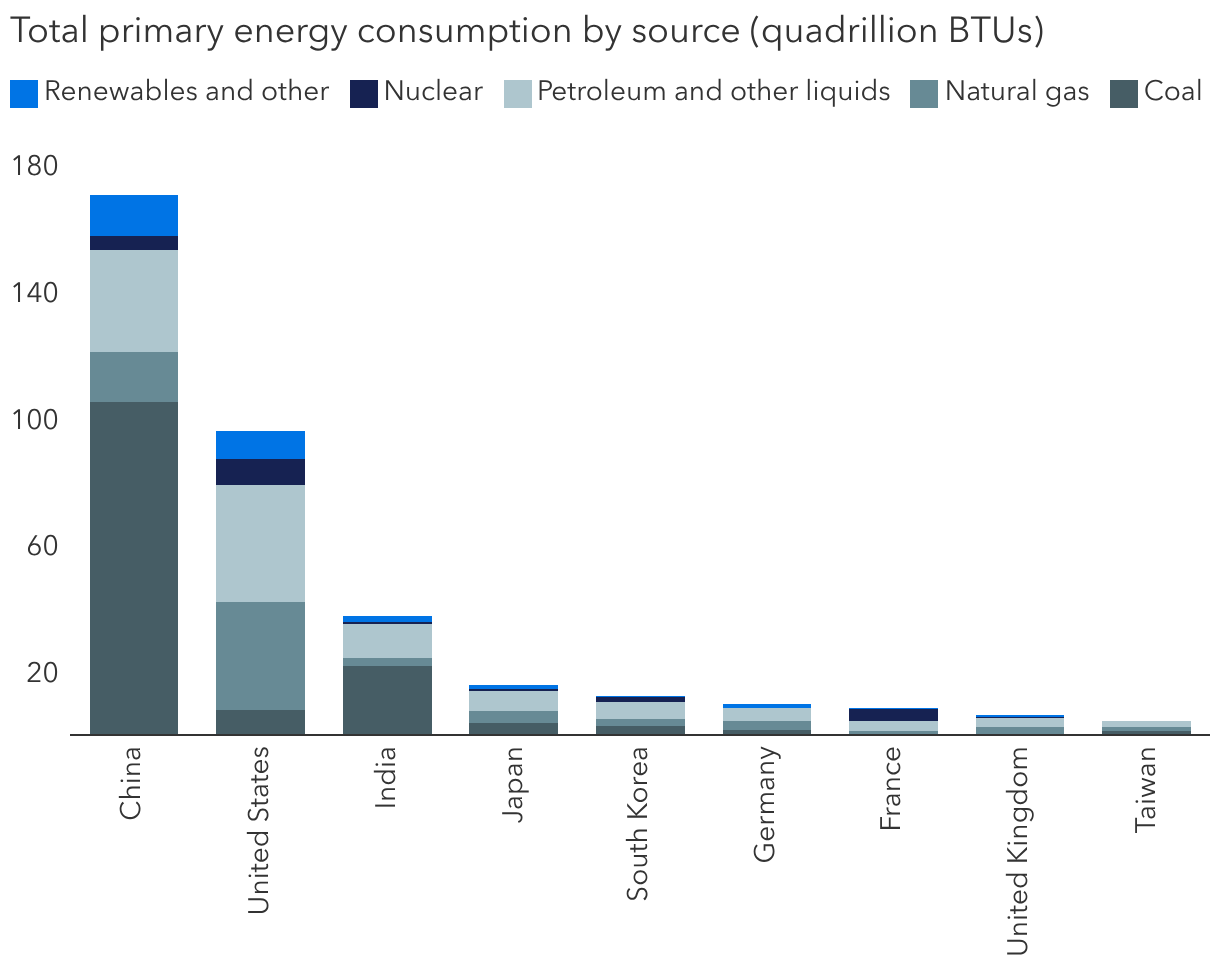

China has been well positioned to absorb the early energy disruption generated by the war. It was able to secure energy deals amid tight supplies with Iran and had for years stockpiled a large strategic petroleum reserve. While China remains the world’s top polluter, the country has also made impressive strides in alternate energy technology. The country has spent hundreds of billions of dollars investing in renewable sources such as wind and solar, as well as nuclear energy and energy storage capacity. It has emerged as a leader in electric vehicles, which now account for nearly half the vehicles sold in China. In the face of scarce energy resources, China can even temporarily turn back to higher levels of domestic coal use.

Worldwide, governments very likely will consider building larger reserves of oil and natural gas to get away from dependence on the spot market. For investors, war underscores that supply disruption tied to geopolitical events can no longer be viewed as rare, and a structurally higher energy risk premium may be warranted. Companies that benefit include energy conglomerates such as ExxonMobil, whose scale and diversification allow them to absorb these shocks.