Interest Rates

Categories

Market Volatility

Investing ahead of a recession: 5 mistakes to avoid

It’s been a summer to remember for investors, but for all the wrong reasons. The yield curve inverted, trade conflicts intensified and the U.S. economy showed more signs of its age. But just as the summer inevitably turns to fall, investors may be wondering if the economy is moving into its next stage too. Could a recession be on the horizon?

Maybe. Maybe not. Recessions are notoriously difficult to predict , even when signals are starting to flash red. But that doesn’t mean investors should do nothing. Since the stock market tends to lead the economy by several months it’s often better to be proactive. Late in the economic cycle can be a good time to re-evaluate portfolios, ensuring they are properly balanced and positioned for elevated volatility.

Some may think the best way to prepare portfolios for a recession is to drastically reduce stocks in favor of bonds. The problem with this approach is that it requires a soothsayer-like ability to time the markets. Some of the strongest returns can occur during late stages of an economic cycle and immediately after a market bottom, so being wrong on either turning point can be devastating to long-term returns. A more realistic approach may be to maintain an appropriate balance between equities and fixed income but upgrade the quality of both.

Upgrade your stock portfolio

In volatile markets, investors often tilt their equity portfolios toward value investing and focus more on dividend stocks. This can be an effective way of reducing portfolio risk, but it can also give investors a false sense of security if they don’t know what they’re buying. Here we highlight three common assumptions often made by investors when they look to increase their value-oriented allocation followed by a suggestion for what may be a better way to upgrade equity portfolios.

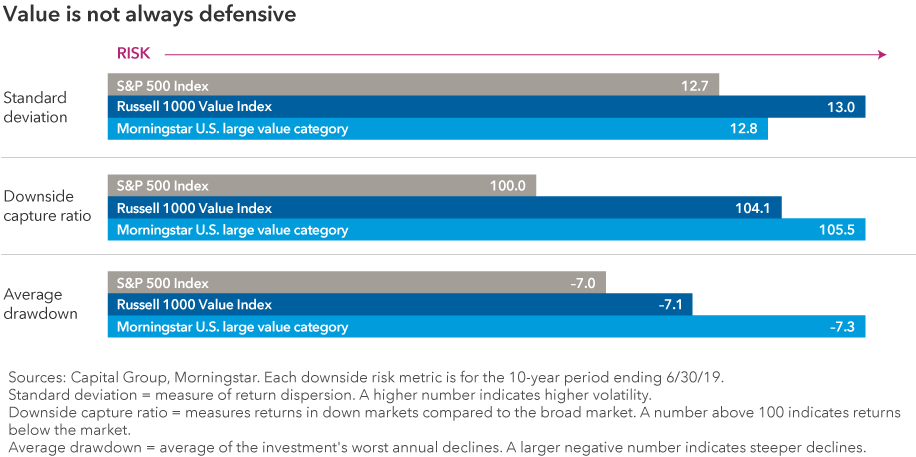

Assumption 1: Value investing will always reduce volatility.

Reality: Value indexes can be just as risky as the broader market. Portfolio risk is commonly measured by standard deviation, downside capture ratio and average drawdown. If moving to a value portfolio ahead of expected volatility, you’d want these measures to show lower risk than the overall market. But surprisingly, we see exactly the opposite for both the Russell 1000 Value Index (the most common benchmark for large-cap value investing) and the Morningstar Large Value category (a composite of value-oriented mutual funds) over the last 10 years.

The takeaway? Not all value is created equal. It can be more effective to hold a mix of dividend-paying stocks than a value index.

Assumption 2: Value investing is the same as dividend investing.

Reality: Many stocks in value indexes don’t pay dividends. Dividend-paying stocks have tended to hold up better during periods of volatility, so investors may benefit from more dividend exposure ahead of a recession. But don’t assume every value fund will make dividends a priority. About 22% of stocks in the Russell 1000 Value Index paid dividends of less than 0.1%, as of December 31, 2018.

Assumption 3: Value investing only includes high-quality companies.

Reality: Low-quality and distressed companies are commonly included in value portfolios. Around 40% of the rated companies in the Russell 1000 Value Index were BBB- or lower (as of December 31, 2018), including many high yielding dividend payers. Companies often appear solid on the surface but carry significant debt burdens and may be on the cusp of losing their investment-grade credit rating. A missed payment or a downgrade could send share prices tumbling, so investors should focus on higher quality companies that are most likely to maintain consistent dividend payments.

What can be done instead?

Investors looking to reduce equity volatility ahead of a recession should consider more rigorous fund screens and not assume that any product with a “value” label will help them achieve their goals. As we see with the Russell 1000 Value Index, even the flagship benchmark for value investing falls short in many ways. Consider a screen that includes funds with the following factors:

- High percentage of dividend-paying stocks

- High percentage of companies with credit ratings of BBB and above

- Low fund-risk metrics, including average drawdown, downside capture ratio and standard deviation

There are many funds that fit these criteria. Within the American Funds family, two funds to consider for your clients’ portfolios include Washington Mutual Investors Fund and American Mutual Fund®.

Upgrade your core bond portfolio

Fixed income investments can provide an essential measure of stability and capital preservation, especially when stock markets are volatile. But here too, investors often assume their portfolios are safer than they really are.

Assumption 4: In a low-rate world, I should reach for yield to get income.

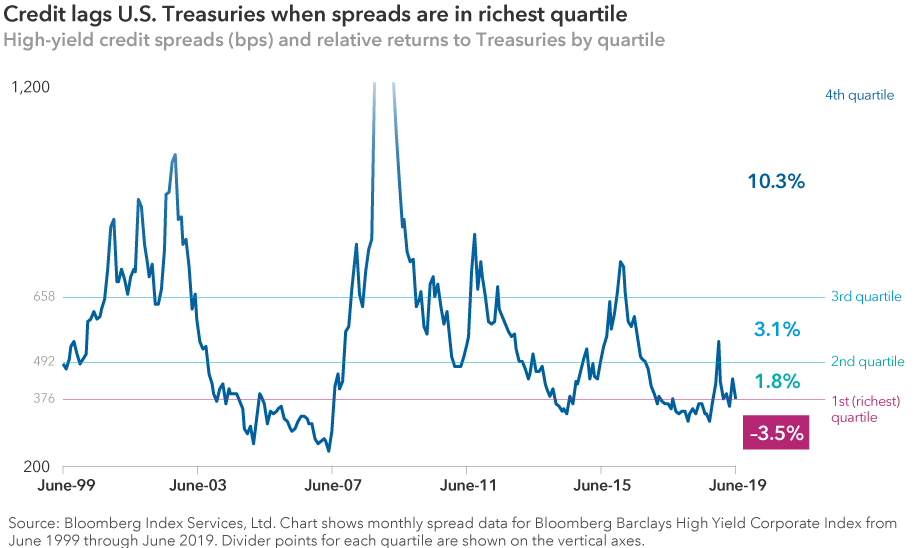

Reality: Reaching for higher yield can be risky. High-yield credit spreads have tightened, and when that has happened in the past credit has significantly lagged U.S. Treasuries. Bond funds with more high-yield exposure also tend to have higher correlations to equity, something investors should avoid in the core bond holdings if they are trying to reduce portfolio volatility.

Assumption 5: Short duration will help reduce volatility.

Reality: Shortening duration probably won’t help as the Fed is done hiking rates for now. Investors often turn to short-term bonds for lower interest rate risk, but that is usually most beneficial in a rising-rate environment. Following the Fed’s rate cut in July, markets have been pricing in five more rate cuts by the end of 2020.

What can be done instead?

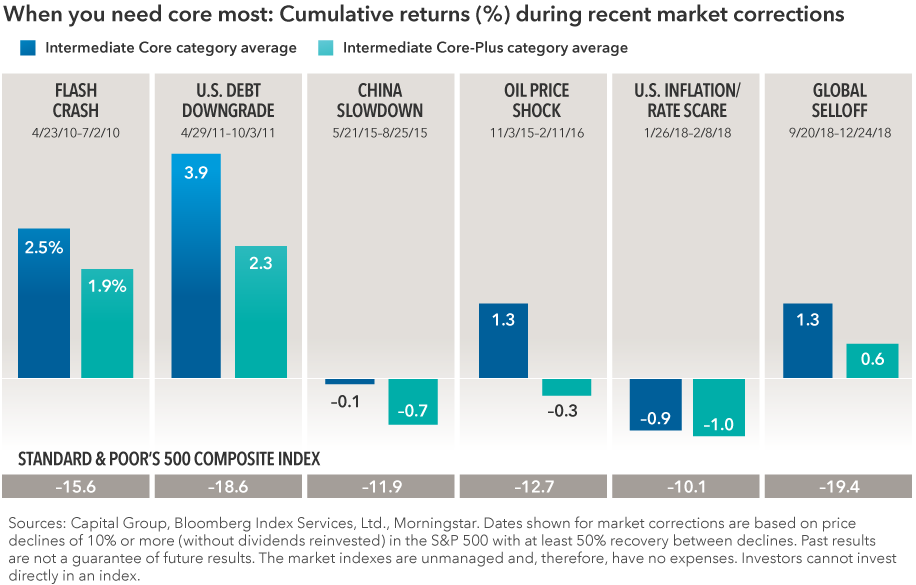

Research firm Morningstar helped simplify bond fund selection earlier this year when it split its largest Intermediate-Term Bond category based on credit risk. Bond funds with less than 5% high-yield exposure were relabeled Intermediate Core, while funds with more now fall into the Intermediate Core-Plus category.

The distinction can be especially important during periods of elevated market volatility, when it’s likely you want more core in your portfolio. During the last six equity corrections, the core category had higher returns than core-plus and provided much needed portfolio stability. The Bond Fund of America® is now the largest fund in the category.

Maintain a long-term perspective

Recessions can be painful, but investors who are well prepared and maintain a long-term investment horizon should be comforted that economic declines have been relatively small blips in economic history. Over the last 65 years, the U.S. has been in an official recession less than 15% of all months, with the average recession lasting just under a year. Maintaining a balanced, well-diversified portfolio can help investors avoid the pitfalls of market timing, while being prepared for the relative short-term volatility that comes with recessions.

Learn more about

Bloomberg Barclays U.S. Corporate High Yield Index covers the universe of fixed-rate, non-investment-grade debt. This index is unmanaged, and its results include reinvested distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

Bloomberg® is a trademark of Bloomberg Finance L.P. (collectively with its affiliates, “Bloomberg”). Barclays® is a trademark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Neither Bloomberg nor Barclays approves or endorses this material, guarantees the accuracy or completeness of any information herein and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

©2019 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

Russell 1000 Value Index measures the results of the large-cap value segment of the U.S. equity universe.

The Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the average weighted results of approximately 500 widely held common stocks. The S&P 500 is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2019 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor's, Moody's and/or Fitch, as an indication of an issuer's creditworthiness.

Our latest insights

-

-

Municipal Bonds

-

Artificial Intelligence

-

Target Date

-

Technology & Innovation

This is the headline for the Newsletter promo. Customize the message.

RELATED INSIGHTS

-

Market Volatility

-

Asset Allocation

-

Global Equities

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

American Funds Distributors, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.