Interest Rates

Categories

Monetary Policy

What’s next for the Fed in 2019?

Tom Hollenberg

Tom Hollenberg

Ritchie Tuazon

Ritchie Tuazon

December 19, 2018

KEY TAKEAWAYS

- The Fed hiked rates to its new target range by 25 basis points, as expected.

- However, the Fed’s stance on future hikes has moderated amid tighter financial conditions.

- A pause in 2019 now appears more likely.

Business as usual? Not quite

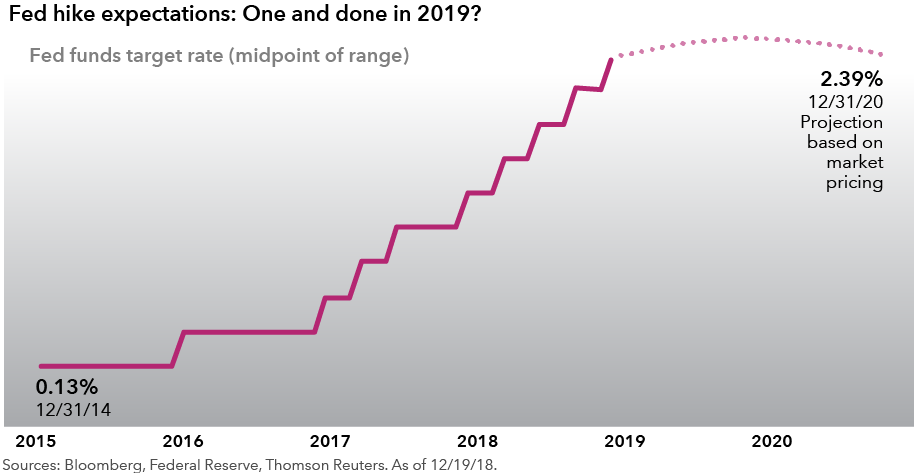

Hike number nine was, at first glance, business as usual for the Federal Reserve. The target federal funds rate range now stands at 2.25%–2.5%, following the widely expected move to raise rates by a quarter percentage point on December 19.

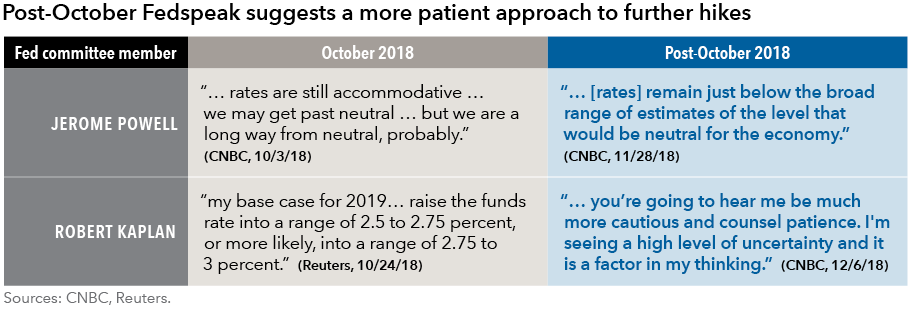

Yet in terms of what comes next the Fed’s stance has changed. Here’s why: In October and November 2018, a stronger dollar, wider credit spreads and weak equity markets all contributed to tighter financial conditions.

In the wake of this volatility, members of the Fed’s rate-setting committee have struck a more “dovish” tone. Put another way, their appetite for significant further rate hikes seems to be diminishing.

What’s in the cards for 2019 and beyond?

The Fed’s estimate of future rate hikes in 2019 — the closely watched “dot plot” — has declined from three to two. Importantly, the Fed has made a point of reminding the market that its decision-making is “data dependent.” That means their policy stance will evolve with financial and economic conditions. Bond investor expectations also have shifted, with market pricing suggesting zero or only a single hike is the most likely outcome next year.

The market’s view on rates in 2019 seems reasonable given the current backdrop. U.S. economic data have remained decent overall. The expansion has been solid, with GDP growth likely to come in above 3.3% for 2018. Manufacturing activity as measured by the Purchasing Managers' Index* is averaging 59.2 YTD, and wage growth has picked up to the neighborhood of 3%.

On the other hand, recent core inflation — which excludes volatile food and energy prices —has been slightly weaker than anticipated. A drop in fuel prices prompted headline inflation to fall from 2.5% year-on-year in October to 2.2% in November. The Fed’s preferred inflation gauge, the core Personal Consumption Expenditures index, remains below its 2% target.

Several large storm clouds also loom over U.S. economic prospects, such as simmering trade tensions between the U.S. and China and uncertainty over the fate of Brexit. Markets also have been spooked by a recent so-called inversion of the U.S. Treasury yield curve.

Looking further out, markets have shifted rate expectations in 2020 and 2021 from a Fed that is more likely to raise rates to a Fed that is more likely to cut. This market view seems reasonable. With the effects of fiscal stimulus wearing off in 2019, and growth in China and Europe softening, it may be difficult for the U.S. to continue to anchor the global economy. Recent business investment has not been robust and that can further dampen future growth prospects. The probability of rate cuts in 2020 and 2021 should indeed be higher than that of additional hikes.

Learn more about

* PMI measures manufacturing activity. A value over 50 is an indicator of an expansionary economy.

Our latest insights

-

-

Municipal Bonds

-

Artificial Intelligence

-

Target Date

-

Technology & Innovation

This is the headline for the Newsletter promo. Customize the message.

Related Insights

-

Market Volatility

-

Asset Allocation

-

Dividends

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

American Funds Distributors, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.