Chart in Focus

David Polak

David Polak

Marc Nabi

Marc Nabi

Don't miss our latest insights.

Our latest insights

-

-

Demographics & Culture

-

-

Global Equities

-

Target Date

SpaceX kicked off its initial public offering ahead of pending listings from high-profile AI firms Anthropic and OpenAI, among others. How should investors approach these deals, especially in the context of index inclusion, market concentration and portfolio construction?

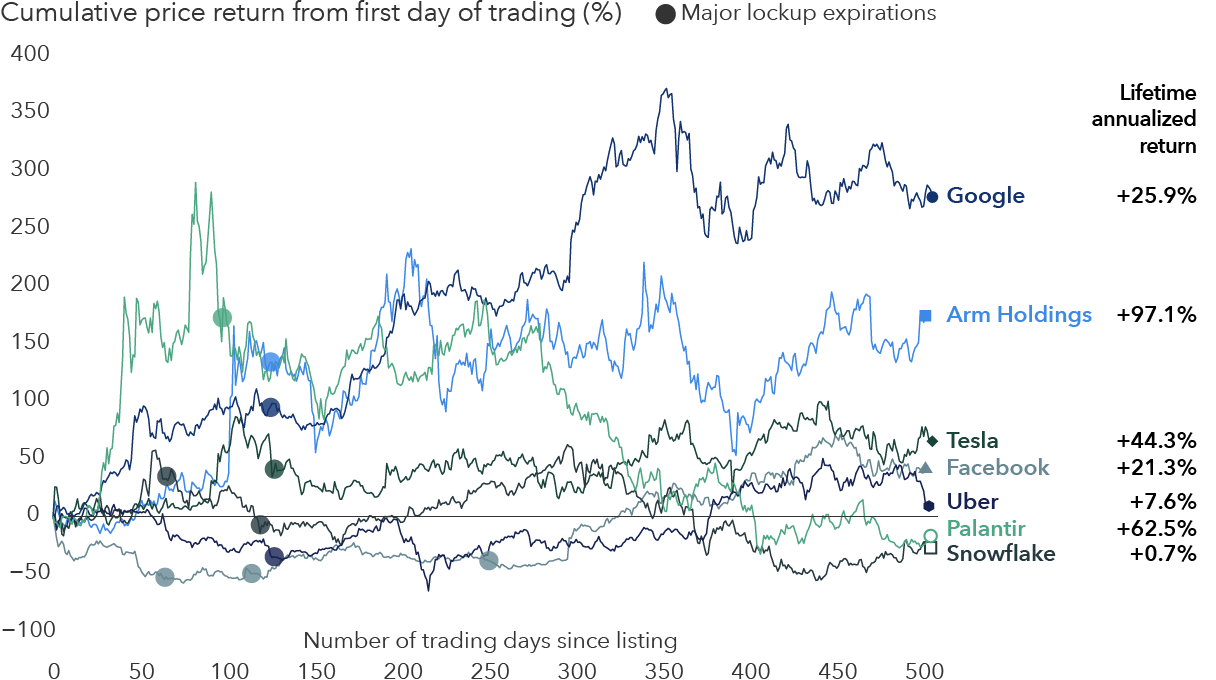

Zooming out on some of the largest U.S.-listed tech IPOs since 2004 shows that after the initial first-day return, many struggled in the weeks that followed. This reflects a period of price discovery, as some investors take profits while others build positions. Over time, however, shares tend to track earnings potential and better reflect the value of the underlying business.

High profile tech listings tend to be volatile in the short term

Sources: Capital Group, FactSet, company filings. Data shown represent cumulative price returns from the opening price on each company’s first day of trading over the first two years following its IPO or direct listing. Companies shown are selected examples of widely followed technology listings since the early 2000s, included to illustrate a range of industries, listing types and post-listing outcomes. Returns are shown for illustrative purposes only. Major lockup expirations shown reflect initial or significant subsequent expiration dates for insider share sale restrictions following each listing, based on company filings and publicly reported lockup schedules. Lifetime annualized returns are calculated from each company’s first day of trading: Google (now Alphabet, August 19, 2004), Tesla (September 29, 2010), Facebook (now Meta Platforms, May 18, 2012), Uber (May 10, 2019), Snowflake (September 16, 2020), Palantir (September 30, 2020) and Arm Holdings (September 14, 2023), all through May 31, 2026. Returns are based on Class A shares where applicable. Price returns exclude the reinvestment of dividends and capital distributions. Past results are not predictive of results in future periods.

What makes this current wave of mega IPOs unique is that some index providers have altered their inclusion rules to accommodate large IPOs to join more quickly, such as Nasdaq and Russell 1000.

Near-term, we expect SpaceX’s index inclusion will generate some sustained buying interest in the days following the company’s addition. At the same time, some existing index constituents may face modest selling pressure to create room for a new entrant. These effects are likely to be relatively mild and short-lived.

Evaluating a vast range of IPOs relies on thorough research that assesses the long-term fundamental case for a stock affecting various industries. That framework does not change because an index does.

The AI boom has generated widespread retail and institutional interest, which is expected to increase further as large IPOs come to market. At the same time, companies have experienced rapid valuation gains, bringing market concentration into sharper focus. While the long-term earnings trajectory remains uncertain, periods of valuation adjustment and volatility are a natural part of aligning expectations with realized outcomes.

AI can support long-term return potential and represent a credible allocation within portfolios. However, exposure should be balanced, with no single theme dominating overall risk.

Recent dispersion within the Magnificent Seven highlights this dynamic. Despite strong interest in AI, stock performance has diverged this year, reinforcing the need for selective exposure, particularly as new IPOs come to market.

The Magnificent Seven stocks consist of Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla.

RELATED INSIGHTS

-

-

Podcast

-

World Markets Review

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.