Demographics & Culture

Categories

Artificial Intelligence

4 scenarios for the future of AI

Jared Franz

Jared Franz

April 1, 2026

Don't miss our latest insights.

Artificial intelligence continues to evolve at a rapid pace. Models are improving, computing costs are easing and companies are beginning to report tangible efficiency gains.

At the same time, AI’s investment cycle is becoming more structural. Hyperscaler capital expenditures (capex), data center expansion and financing for electricity‑intensive projects are increasingly utilizing debt markets. Corporate bond markets are experiencing a notable increase in supply this year, with a meaningful share linked to large‑scale technology investment. Rising capex, higher issuance and falling cost of computing power (the hardware resources required to make AI function) point to the start of a capital deepening cycle, not a temporary upswing.

Policy is shaping the transition. Fiscal easing in parts of Europe, accommodative settings in Japan and expected interest rate adjustments in the U.S. provide space for investment to continue. Regulation is tightening, but the overall policy environment — especially given the backdrop of national strategic competition — still points toward enabling adoption rather than impeding it.

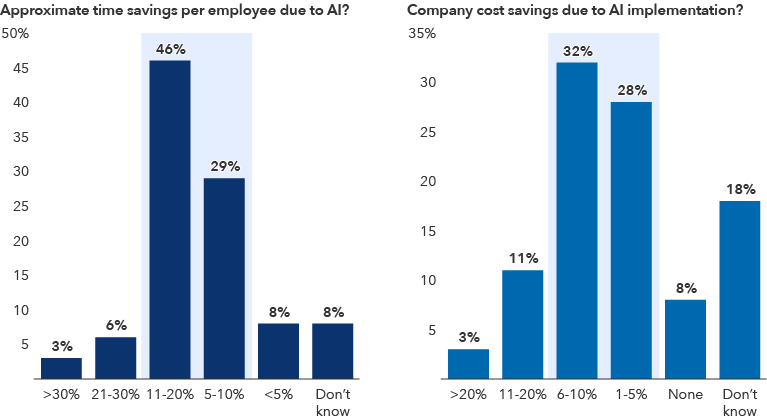

Productivity gains are beginning to show

The result is significant momentum, albeit with a side of uncertainty. Adoption is broadening, yet real‑world friction remains. Investment is strong, though returns will depend on how quickly these tools spread across the wider economy.

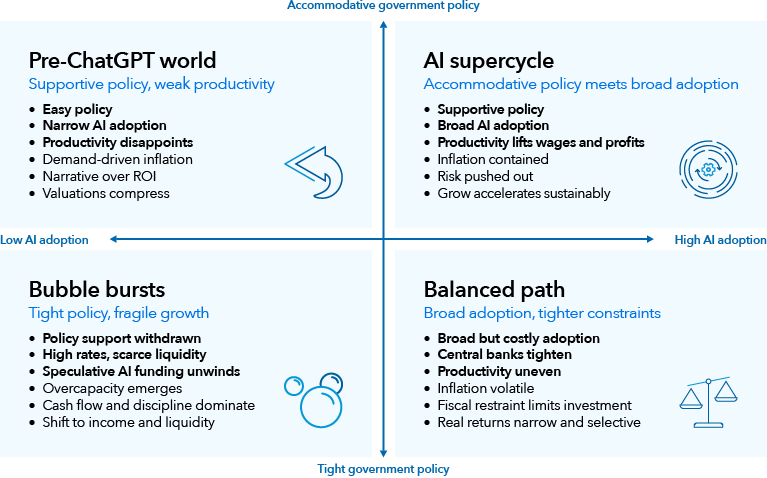

When uncertainty is high, single‑point forecasts can fall short. Enter the Night Watch: a multidisciplinary team of Capital Group economists, political analysts and portfolio managers who explore market disruptions to help make better investment decisions. The group collaborates to envision a range of plausible futures rather than predicting a single outcome. Night Watch helps illuminate how different combinations of technological, economic and policy forces could interact — and what each path might mean for portfolios.

In the case of AI, those axes can be expressed as the degree of AI adoption across the economy and the stance of policy and financial conditions. Crossing these axes produces four distinct worlds. The following scenarios draw on this framework to outline how the AI transition could unfold.

A framework for thinking about the future of AI

Scenario 1: AI supercycle

In this scenario, AI becomes embedded across industries. Companies reorganize workflows, automate routine tasks and use AI tools for operational, analytical and creative work. Early signs of productivity improvement and falling cost of computational capacity lower the barrier to broader adoption.

Supportive policy plays a reinforcing role. Governments prioritize competitiveness, national productivity and the strategic importance of AI‑enabled industries, leading to an environment that encourages continued investment. Regulatory frameworks evolve in ways that enable experimentation and deployment, and fiscal tools — whether incentives, procurement or targeted infrastructure spending — help clear bottlenecks and accelerate wider use.

A sustained investment cycle also takes hold. The expansion of data center capacity and related infrastructure drives persistent demand for electricity‑intensive equipment and materials, while lower unit computing costs make it easier for firms to scale up AI usage. With accommodative policy and accessible financing working alongside broad adoption, the interaction between the two axes is mutually reinforcing: productivity gains support earnings, which support investment, which drives further usage. The result is a prolonged period of elevated growth and improving margins.

Scenario 2: Balanced path

Here, AI continues to move forward, but the pace differs meaningfully across companies and sectors. Some firms scale adoption quickly, while others proceed cautiously due to costs, power constraints, data readiness issues or regulatory uncertainty. Progress is real, but inconsistent. The trajectory resembles a staircase rather than an escalator.

Several practical constraints contribute to this uneven progress. In some areas, financing costs remain elevated or balance sheet priorities limit the speed at which firms can retool. Elsewhere, companies are working through legacy systems or adapting to evolving regulatory standards that slow full integration. Policy signals can also be mixed — supportive in some jurisdictions, more cautious in others. These frictions do not halt momentum, but they produce a pattern where some sectors move quickly while others wait for clearer economics or a more favorable policy backdrop.

Scenario 3: Bubble bursts

In this world, investment runs ahead of realized returns, while policy or financial conditions become less supportive. Higher borrowing costs, tighter credit standards or a shift in risk appetite make it harder to fund new projects. Fiscal positions may also become more constrained, prompting governments to rein in support or prioritize other areas. Regulatory scrutiny may increase, particularly in sectors facing questions about data security, competitive dynamics or labor displacement. The combined effect is a tightening in the overall policy environment that amplifies existing concerns about returns.

Meanwhile, some data center projects face delays, and parts of the power and semiconductor supply chain may prove overbuilt in the near term. Companies reassess the pace of deployment and investors tilt toward stability. The key risk is not that AI fades, but that investment outpaces the underlying economics.

Large, debt‑funded projects may crowd out other corporate issuances or lead to patches of underutilized infrastructure. Markets reassess timelines for returns, prompting firms to delay expansion plans and focus more on utilization than on rapid buildout.

Scenario 4: Return to pre-ChatGPT world

In this scenario, AI never becomes the catalyst many expected. Adoption remains stuck at the margin: tools are tested, dashboards improved, a few workflows partially automated — but the step change never arrives. Businesses experiment without fully committing, held back by fragmented systems, uneven data foundations and limited capacity to absorb change. AI proves helpful in pockets but fails to shift how firms operate at scale, leaving productivity gains modest and confined to isolated functions rather than the broader economy.

Even with supportive policy and cheap capital, momentum slows. Funding flows remain available, yet investment gravitates toward proven technologies with clearer returns. Liquidity lifts markets, but it floats narratives more than output, and valuations become increasingly disconnected from real efficiency improvements. Growth continues to rely on traditional drivers while AI plays a peripheral role, shaping expectations more than outcomes. The result is a cycle defined by optimism without transformation — a world where AI matters, but not enough to move the macro needle.

Investor implications

Early signals currently suggest that AI‑driven expansion has already begun. Productivity gains are becoming evident in the data, investment in AI‑related infrastructure remains elevated and the policy backdrop in major economies is broadly supportive of continued innovation.

Against this backdrop, the balance of evidence leans toward a constructive path — one in which adoption widens, productivity accumulates and capital continues to be allocated to AI’s development. But the picture is not one‑sided. A world of steady but uneven progress remains entirely plausible, and there is always the possibility that expectations run ahead of returns or that adoption settles at a steadier state. Each scenario reflects a different alignment of the two critical axes: how broadly AI spreads through the economy, and whether policy and financial conditions remain supportive or begin to tighten.

For investors, the practical task is not to pick a single outcome, but to monitor the signals that indicate where we are moving along those axes: the pace of enterprise integration, evidence of durable productivity gains, the rhythm of capital spending and how policymakers respond as the cycle evolves. AI is advancing quickly; the economy will adjust more gradually. Staying attuned to the shifts that pull us closer to one scenario or another will be essential as this transition unfolds.

Learn more about

Our latest insights

-

-

Demographics & Culture

-

-

Artificial Intelligence

-

RELATED INSIGHTS

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and/or summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.