Bonds

Margaret Steinbach

Margaret Steinbach

Don't miss our latest insights.

Our latest insights

-

-

Demographics & Culture

-

-

Global Equities

-

Target Date

- Nearly one-third of U.S. institutional investors surveyed plan to increase fixed income allocations in the next 12 months, most often funded by reductions in equities and alternatives.

- Investors are prioritizing diversification of their credit positioning across sectors.

- Nearly 60% of U.S. institutional investors surveyed now allocate 10% or more to private credit, reinforcing its role as a mainstream portfolio component.

Amid a backdrop of macroeconomic uncertainty, U.S. allocators are returning to a familiar anchor: fixed income.

Capital Group contracted CoreData Group to survey 300 global institutional allocators about their approach to fixed income during February and March 2026. The 75 U.S. investors who participated indicated they are tilting more heavily into bonds for a measure of relative safety.

The data from our 2026 Fixed Income Horizons global survey suggests a deliberate, structural shift — one driven by the need for resilience, greater diversification and better portfolio balance. The survey captures the views of senior investment professionals at institutional asset owners, including pension funds, insurers, endowments, foundations and single-family offices.

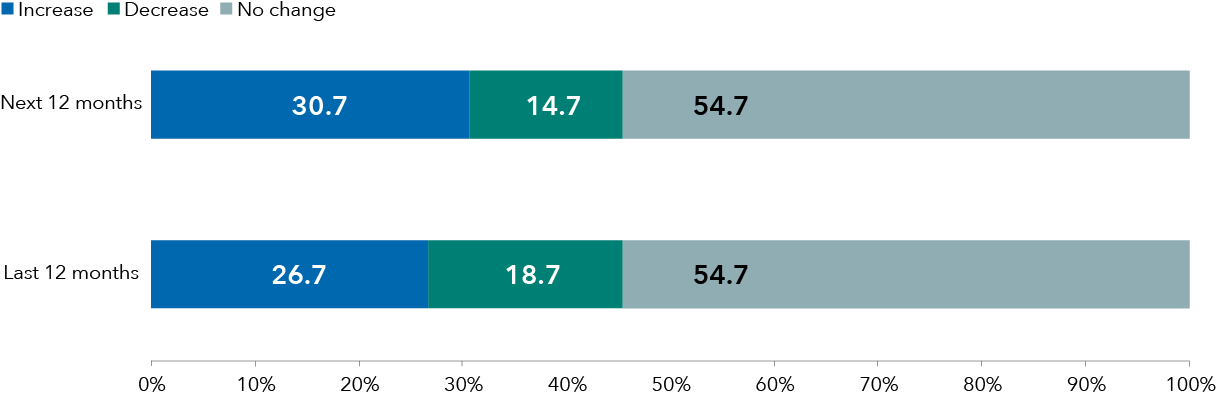

Nearly one-third of U.S. allocators surveyed plan to boost their overall allocation to liquid public fixed income in 2026, up from 26.7% who increased it in the last 12 months. This marks a continued shift toward bonds as a defensive anchor, driven by demands for downside protection and portfolio de-risking potential — the top-cited motives for increasing fixed income exposure.

Overall allocations to fixed income (%)

Crucially, this is not happening in isolation. Respondents indicated that allocations to fixed income are largely being funded by reductions in listed equities, real estate and hedge funds.

“We are underweight public equities, at least around the margins compared to where we should be in our policy,” said one deputy chief investment officer at a U.S. endowment fund. “That is an active decision, to taper off a bit of that risk. You feel pretty good about just owning a 7% returning bond, for example, and just sitting on it for a bit if needed.”

In an environment defined by geopolitical uncertainty, fixed income is reasserting its role as a portfolio stabilizer.

Strong emphasis on diversification across credit sectors

Although headline allocation increases are notable, equally interesting is how the composition of fixed income portfolios is evolving.

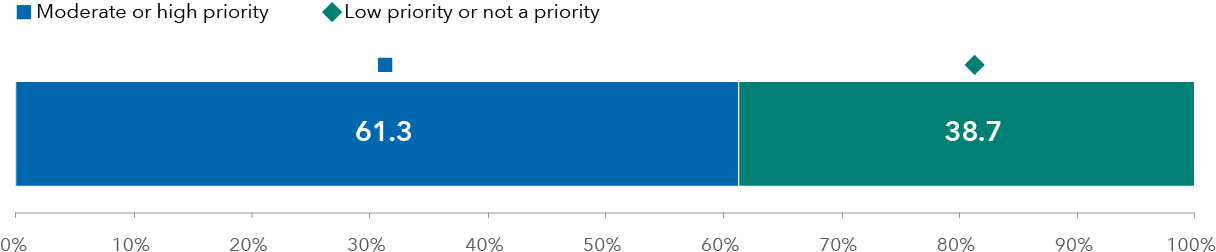

One-third of U.S. allocators said they plan to decrease their overall credit risk in the next 12 months, up from just 11% last year while a majority (61.3%) of U.S. investors said adjusting the composition of their credit portfolios is a priority. Investors also indicated they want to maintain flexibility in their portfolios.

To what extent are you prioritizing adjusting the composition of your credit portfolio in the next 12 months?

This signals a more nuanced approach reflective of the current market environment: Against a backdrop of tight spreads and macroeconomic uncertainty, investors are less interested in increasing credit risk and more focused on the composition within credit and adding flexibility to portfolios. They are diversifying more and positioning themselves to take advantage of future changes in valuations that may be uneven across different credit sectors.

Together, these shifts point to a market that remains constructive on income but increasingly selective about where risk is being taken.

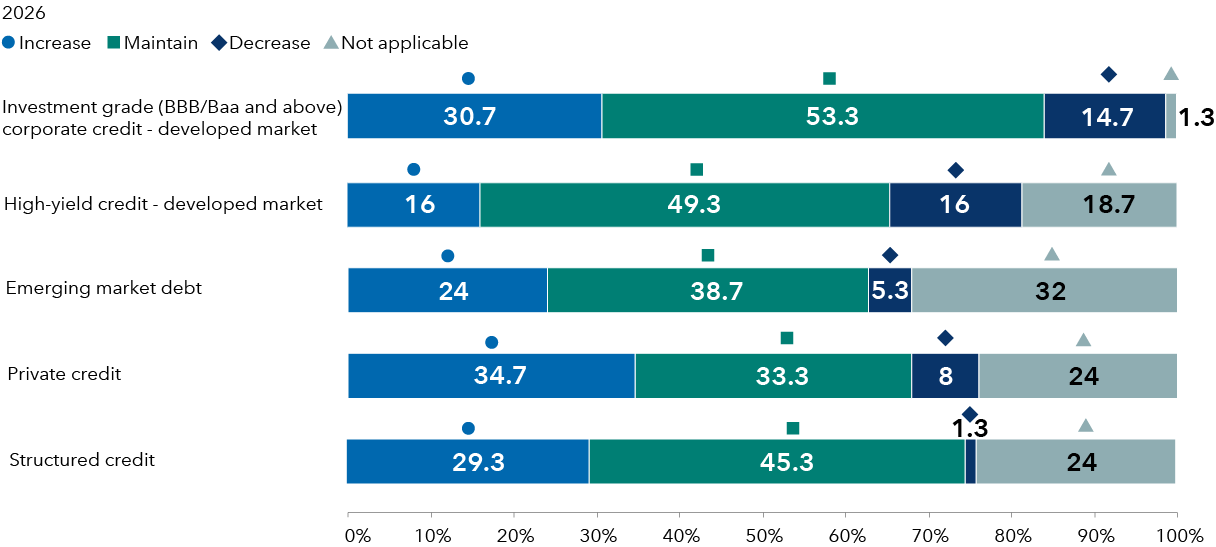

Fixed income allocations in the next 12 months

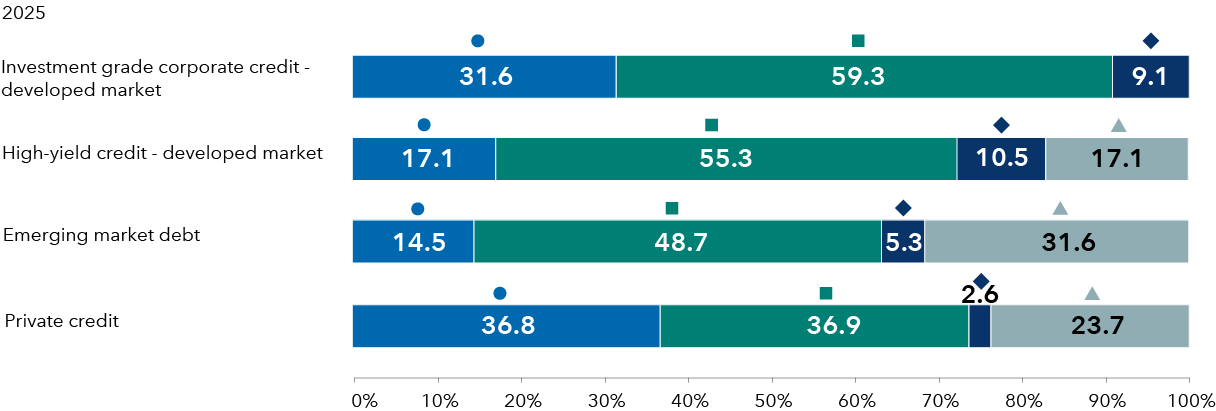

Respondents were not asked about structured credit in 2025.

Private credit moves into the core

At the same time, private credit continues its transition from niche allocation to strategic core holding.

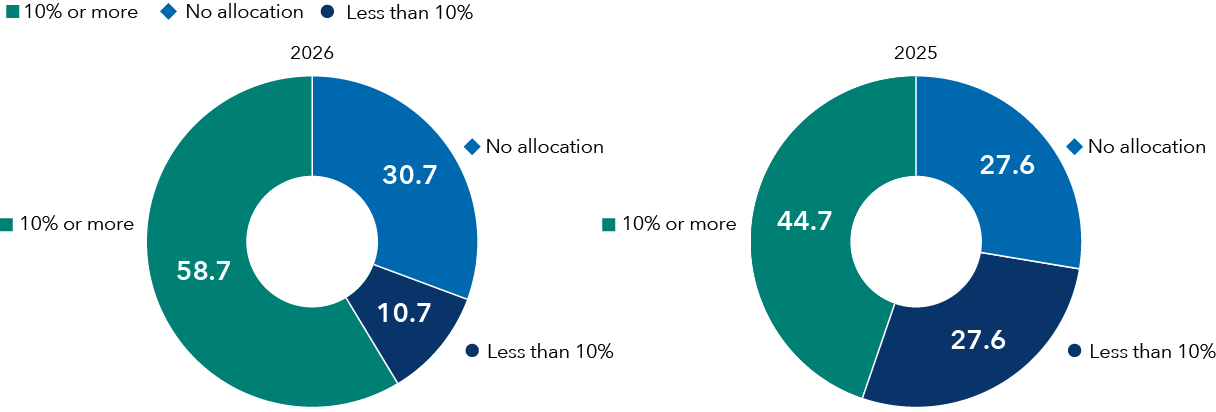

Today, approximately 60% of U.S. institutional investors surveyed allocate at least 10% of their portfolios to private credit — up from roughly 45% a year ago. The resilience of this adoption is notable, particularly given ongoing concerns around liquidity and recent outflows.

“We think private credit is a better absolute return diversifier,” said one U.S. allocator. “We've made the decision to own less hedge funds and more private credit. We like its profile and downside better than other absolute return vehicles.”

What is your current allocation to private credit?

Importantly, forward-looking sentiment suggests moving toward stability rather than retrenchment. Of U.S. investors surveyed, 35% plan to increase private credit allocations in the next 12 months while only 8% expect to reduce exposure.

U.S. continues to be seen as a safe haven

U.S. institutions continue to exhibit a home bias, viewing core fixed income — particularly Treasuries — as a durable foundation, even amid evolving macro risks.

When asked about certain scenarios related to the strength of U.S. economic indicators, a majority expect U.S. dollar weakness to be a short-term phenomenon, with 64% assigning a near-term likelihood compared with 23% who see it as a long-term scenario. Concerns about U.S. Treasuries losing their reliability as a hedge remain limited, with 51% viewing this scenario as unlikely and 28% viewing it as short term. Similarly, economic growth convergence between the U.S. and Europe is not seen as a dominant risk.

Overall, these insights reveal that U.S. allocators are focused on diversification within portfolios amid a backdrop of continued macro uncertainty and elevated valuations for risk assets. Their focus on downside protection and maintaining flexibility indicates a desire to bolster portfolios to better navigate different scenarios.

Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor's, Moody's and/or Fitch, as an indication of an issuer's creditworthiness.

Investments in private credit and related strategies involve significant risks, including limited liquidity and potential loss of capital. These strategies may include exposure to low and unrated credit instruments, structured products, and derivatives, all of which carry heightened credit, market, valuation, and liquidity risks. Investors should consult with their financial professional when considering such strategies for their portfolios.

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.