Active Management

Categories

Bonds

Look beyond Canada for bond diversification and yield

Naoum Tabet

Naoum Tabet

March 13, 2026

For advisor use only. Not for use with investors

In today’s complicated fixed income landscape, Canadian investors are increasingly seeking ways to enhance portfolio resilience, income generation and diversification.

“One potential solution may lie outside Canada,” says fixed income investment director Naoum Tabet. According to Tabet, the limitations of the Canadian bond market are becoming more apparent, especially when compared to the breadth and depth of U.S. bond markets.

“The Canadian investment-grade (IG) bond market is a useful example,” says Tabet.

He describes the market as being relatively small and highly concentrated in three sectors: banking, utilities and energy. Further, these sectors in Canada are interlinked, which potentially exposes investors to commodity cycles. This structural concentration can limit diversification and increase vulnerability to economic shocks that may affect these industries.

Moreover, liquidity in the Canadian IG bond market is limited. With fewer issuers and less trading volume, investors may face challenges in executing trades efficiently or finding attractive entry points. Limited liquidity can also lead to pricing inefficiencies and reduced flexibility in portfolio management. Unlike the U.S. market, which is guided by the mandatory reporting system of over-the-counter transactions, Canada lacks a strong centralized reporting system, making Canadian corporate bond pricing semi-opaque, dealer driven and concentrated in institutional, with less transparency than the U.S. market.

The U.S. advantage: Scale, sector breadth and yield

In contrast, the U.S. IG bond market is the largest and most diverse in the world. It spans hundreds of issuers across a dozen-plus number of sectors, including consumer non-cyclicals, technology, and capital goods — areas largely absent from the Canadian landscape.

“This breadth provides Canadian investors with exposure to a wider array of economic drivers and reduces reliance on any single sector,” says Tabet.

From a yield perspective, as of February 28, 2026, U.S. IG bonds yielded 4.8% in comparison to their Canadian IG counterparts at 3.6%. This equates to a yield differential of 1.2%.

“The yield differential is particularly attractive given the similar credit quality and risk profiles of investment-grade bonds in both markets,” adds Tabet.

Higher yields outside Canada

Aggregate and select Canadian vs. U.S. bond yields (average yield-to-maturity)

As of February 28, 2026

Sources: Capital Group, Bloomberg, S&P.

*Canada aggregate represented by FTSE Canada Universe; U.S. aggregate represented by Bloomberg U.S. Aggregate Bond Index; Canada investment grade represented by S&P Canada Investment Grade Corporate Bond Index; U.S. investment grade represented by Bloomberg U.S. Corporate Investment Grade Bond Index.

When it comes to aggregate yields, which encompass most bond segments in each country, the difference is 3.3% in Canada compared to 4.2% in the U.S.

Currency hedging: Cost today, opportunity tomorrow

One of the primary concerns for Canadian investors considering U.S. bonds is currency risk. Hedging U.S. dollar exposure can reduce volatility but comes at a cost, which is currently significant.

This cost initially offsets the yield advantage of U.S. bonds, but it’s worth noting that these costs are not static. They are driven by the interest rate differential between Canada and the U.S., and are reset whenever the currency-hedging derivative instruments are rolled forward (typically monthly), as depicted in the chart. It illustrates the historical and projected relationship between U.S. and Canadian interest rates and the corresponding cost of hedging U.S. dollar exposure back to Canadian dollars.

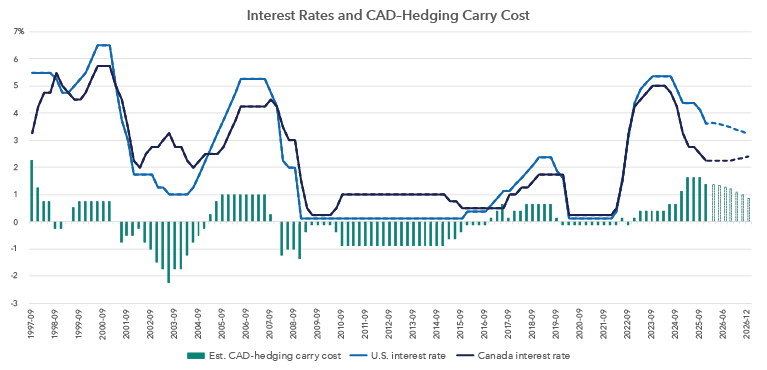

Locking in higher U.S. yields today may be rewarding tomorrow

Historical and forecasted U.S./Canada rate differential and hedging carry costs

Source: Capital Group, Bloomberg. Forecasted rates are based on derivatives markets implied policy rates observed on March 5, 2026.

Through the course of this year (2026), the interest rate differential between the U.S. (blue line) and Canada (black line) is anticipated to narrow, as shown by the dotted forecast segment. The forecast rates are those implied by derivatives markets. This convergence suggests a decline in the estimated hedging carry cost (green bars), reducing the expense of currency-hedging U.S. bond investments for Canadian investors.

According to Tabet, this dynamic creates a window of opportunity: investors can lock in higher U.S. IG yields today while anticipating lower hedging costs in the future.

“Over time, this could result in a cumulative yield advantage of over 100 basis points compared to staying in Canadian IG bonds,” he says.

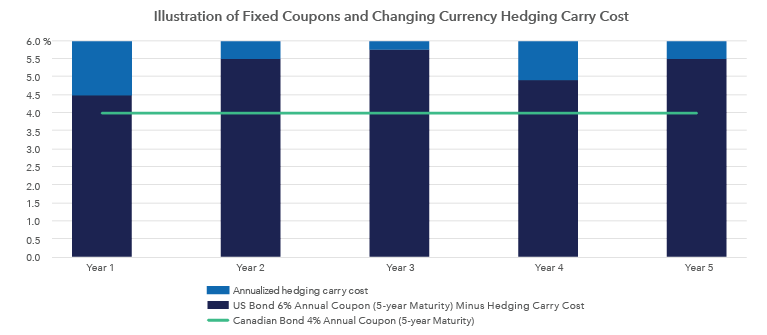

The following illustration is designed to help demonstrate the anticipated, potential yield advantage. The chart compares two hypothetical corporate bonds with the same 5-year maturity. One is a U.S. bond with a 6% annual coupon rate, the other a Canadian bond with 4% annual coupon rate. Importantly, the coupon rates are fixed until maturity, but the cost to hedge currency risk on the U.S. bond is not, as most institutional hedging programs use one-month rolling currency forward contracts.

This means the carry cost of hedging — driven by the aforementioned U.S.-Canada interest rates differential, can change every month. The U.S. bond becomes more attractive relative to the Canadian bond when the carry cost of hedging decreases.

Timing matters

According to Tabet, now may be the best time to act.

“Investors have an opportunity to lock in higher U.S. IG yields today and potentially benefit from favourable rate conditions tomorrow enhancing long-term income and strengthening portfolio resilience.”

Learn more about

Our latest insights

RELATED INSIGHTS

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian investment funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.