Active Management

Categories

Markets & Economy

4 lasting impacts of the Iran war

Tom Cooney

Tom Cooney

April 15, 2026

When I served as a United States diplomat, we often said that war is the failure of diplomacy. The inconclusiveness of last week’s initial negotiations in Islamabad underscores just how fragile diplomacy can be.

Like all wars, however, this war too shall end, and it is clear it will be via a negotiated peace agreement rather than an unconditional surrender. The rocky road to peace only just began in Islamabad, and it was too much to expect full resolution from a single round of talks.

So if we believe that stability will ultimately be restored, what marks on the world will this war leave behind? A conflict-free Middle East after the war appears unlikely, given that deep mistrust and tensions will remain among Iran, Israel, Hezbollah, the Gulf countries, and the still-stateless Palestinians. Even so, my view is the region will eventually achieve a “new normal” that can deliver some stability and allow for the gradual recovery of the world’s economy.

Beyond the region itself, the Iran war has already changed geopolitics in lasting ways. Here, in my view, are four long-term implications of the Iran war:

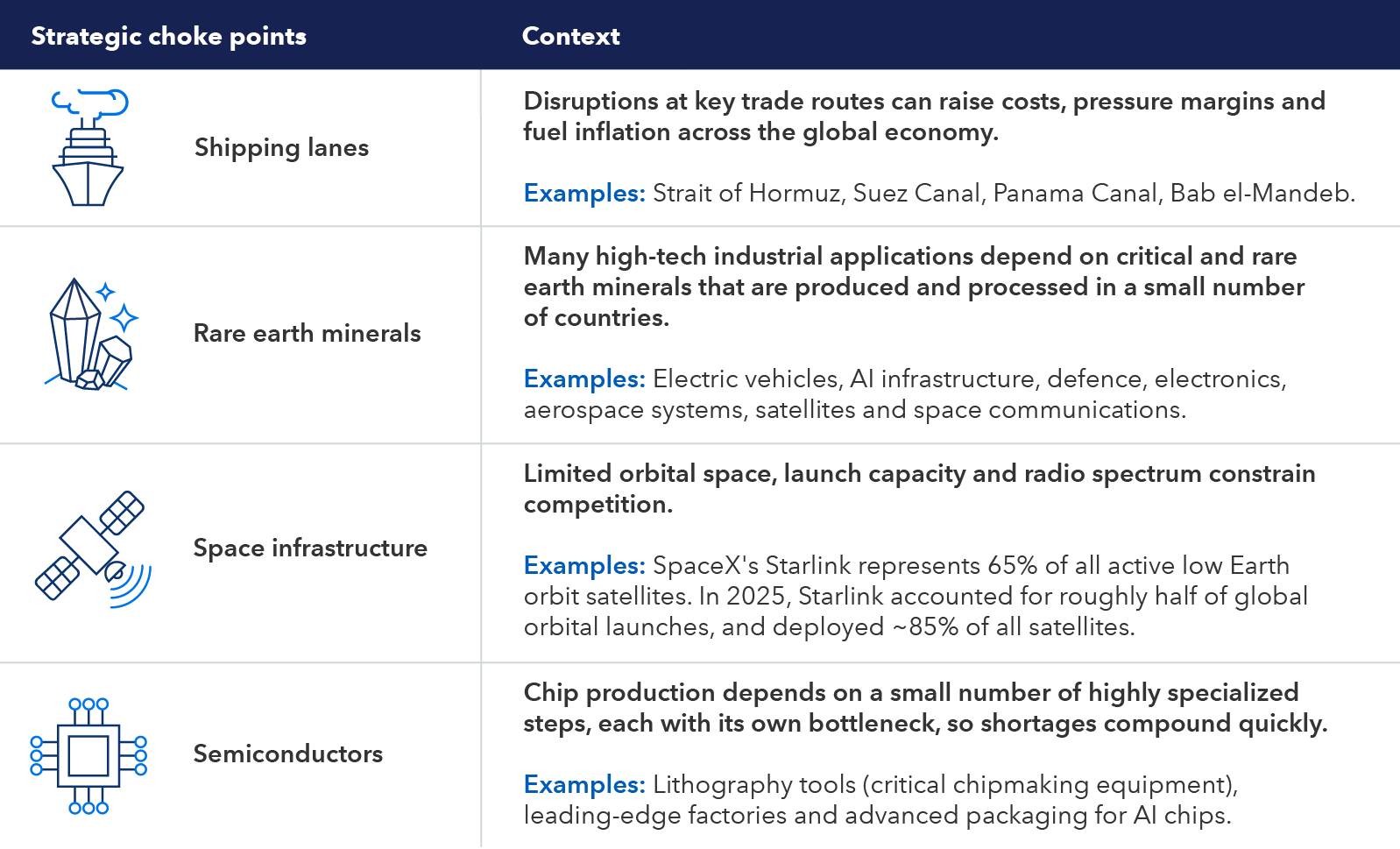

1. Weaponization of economic choke points

Iran’s ability to control the Strait of Hormuz with little more than inexpensive drones, mines and short-range missiles shows how easily narrow waterways can be weaponized. The strait is just one example of a choke point where, by virtue of simple geography and a moderate investment in drones, countries can claim “sovereignty” over a key choke point and effectively cripple supply chains with great harm to the global economy.

Natural waterways such as the Taiwan Strait and Strait of Malacca near Indonesia are shared and protected by international law for good reason. The global economy depends on predictable maritime traffic and open access. Control over any of these waterways effectively translates into control over critical resources. In the case of the Strait of Hormuz, closure caused prices for oil and other commodities such as fertilizers to rise.

The world's choke points

Sources: Capital Group, BryceTech, ElectroIQ, International Energy Agency. As of March 31, 2026. Bab el-Mandeb is a strait with Yemen on one side and Djibouti and Eritrea on the other.

Before the U.S. naval blockade, Iran was reportedly charging ships US$2 million to pass through the Strait of Hormuz despite its long history of being an international waterway free for all to use. After peace is eventually restored, I do not expect such tolls to survive long term because it would set a dangerous global precedent not welcomed by the international community. Granting Iran a form of sovereign control or tolling rights would open the door to countries elsewhere taking steps to do the same in any crucial waterways or islands near them. With the liberal rules-based order already eroding, such a trend would increase the risk of new wars with more consequent harm for the global economy.

The weaponization of other types of choke points is increasingly common. Think back to how China’s ban on exports of critical minerals and rare earth metals raised questions about the potential impacts on defence, automotive, health care and consumer technology. Similarly, restricting China’s access to specialized semiconductor manufacturing equipment provides leverage for the U.S. and its allies.

2. Energy diversification and independence are existential

With oil trapped in the Persian Gulf, several countries particularly in Asia have been forced to ration energy and institute COVID-like restrictions, such as work-from-home requirements. As such, the Iran war is just the latest crisis to highlight that energy security is national security.

Despite the continued rise of renewable energies in China, Europe and elsewhere, oil and liquified natural gas will remain central to energy security for the foreseeable future. I expect a world in which more pipelines like the existing East-West Pipeline in Saudi Arabia are built to transfer oil along alternative pathways out of the Persian Gulf. This may include pipelines across Saudi Arabia, Oman or even Turkey. A network of alternatives will take a few years to build, but with each new route completed, Iran’s choke point power around the Strait of Hormuz will be reduced.

Energy security is pushing the world beyond oil

Sources: Capital Group, U.S. Energy Information Administration (EIA). BTUs = British thermal units. Latest figures available are through 2024, as of March 31, 2026.

The status of the United States as the world’s largest producer of oil and gas and the fact that oil markets are pegged to the dollar remain critical advantages. Still, even with U.S. energy independence, this war confirms that the U.S. is not immune to oil price shocks since oil prices are set in the global market. As a result, energy security in some countries may be reframed to include a broader range of energy sources, such as an increased focus on renewables. Even in places like Japan there is a renewed interest in expanding nuclear.

China’s introduction of the petroyuan in 2018 has caused some concern that the dollar’s dominance as the international reserve currency may fade. I remain skeptical. The renminbi remains constrained by capital controls and limited convertibility, restrictions Beijing is unlikely to loosen meaningfully anytime soon. Central banks are likely to continue the trend of diversifying their foreign currency holdings to reduce dependence on the dollar, but I see no other currency as having the ability to displace the dollar as the single largest reserve currency.

China has been well positioned to absorb the early energy disruption generated by the war. It was able to secure energy deals amid tight supplies with Iran and had for years stockpiled a large strategic petroleum reserve. While China remains the world’s top polluter, the country has also made impressive strides in alternate energy technology. The country has spent hundreds of billions of dollars investing in renewable sources such as wind and solar, as well as nuclear energy and energy storage capacity. It has emerged as a leader in electric vehicles, which now account for nearly half the vehicles sold in China. In the face of scarce energy resources, China can even temporarily turn back to higher levels of domestic coal use.

Worldwide, governments very likely will consider building larger reserves of oil and natural gas to get away from dependence on the spot market. For investors, war underscores that supply disruption tied to geopolitical events can no longer be viewed as rare, and a structurally higher energy risk premium may be warranted. Companies that benefit include energy conglomerates such as ExxonMobil, whose scale and diversification allow them to absorb these shocks.

3. Drones help David stand taller against Goliath

The nature of warfare changes quickly, and one of the worst mistakes a country can make is to be prepared to fight “the last war” instead of potential conflicts ahead. The wars of this decade in Ukraine, Azerbaijan and Iran have shown that drones can be cheap, effective and scalable alternatives to more expensive weapons. The asymmetric power that drones give to smaller, less militarily powerful nations is something with which the great powers will have to contend. Both Ukraine and Iran have substituted drone power for traditional naval power to assert a surprising level of control over key bodies of water (Black Sea and Strait of Hormuz) despite the powerful fleets arrayed against them. I expect the great powers of the U.S., China and Russia to make considerable investments in drone defence innovation going forward.

Cheap drones are redefining the balance of power

Sources: Capital Group, Council on Foreign Relations. Data reflects the upper bound of estimate ranges for range, payload and cost, where applicable. LRASM is long range anti-ship missile, JASSM is a Joint Air-to-Surface Standoff Missile and JASSM-ER is an extended range. A LUCAS drone is a low-cost uncrewed combat attack system. As of March 9, 2026.

New technologies are needed to counter and wage drone warfare, a guerrilla-style method that is decentralized and difficult to degrade. This has implications for defence spending, which I expect to remain elevated in an environment where the old global order is eroding, alliances are weakening, and distrust among nations is growing.

The weakening of NATO also is leading to higher defence spending. While it takes an act of Congress for the U.S. to formally withdraw from NATO, the alliance actually hinges on the conviction that an attack on one is an attack on all. The growing rifts among the U.S. and its NATO allies is well documented, with Greenland and Iran War tensions adding further doubt as to the state of the alliance. As trust in the alliance erodes, European countries along with Japan and Korea may look to be less dependent on U.S. weapons systems. France already has plans to increase its defence spending an additional €36 billion by 2030, directing a large share toward drones, munitions and nuclear weapons. Moreover, if allies begin to doubt the credibility of the U.S. nuclear security umbrella, the risk of nuclear proliferation increases. Countries like South Korea, Japan, Poland, or Turkey may seek independent deterrent capabilities.

For investors, higher defence spending could be a tailwind for U.S. companies such as Northrop Grumman and RTX, a maker of cutting-edge radar and missile defence systems. The effects are likely to extend beyond the U.S. to benefit companies like Britain’s BAE Systems and German firms Rheinmetall and HENSOLDT, a manufacturer of radar and precision optics.

4. U.S. not withdrawing from world; still seeks to shape it

Despite the debate about what the core principles of an “America First” policy are, the war reinforces the reality that the U.S. has not become isolationist and will remain an active player in global affairs. The U.S. National Security Strategy released in 2025 declares aspirations to focus on the Western Hemisphere and de-emphasize involvement in the Middle East, but 2026 has already amply demonstrated that even under the America First administration of President Trump, the U.S. is not reluctant to project power far from home in pursuit of declared policy interests. America’s economic scale, military reach and central role in global financial systems make decoupling difficult.

Under Capital Group’s Night Watch framework, which leans on scenario planning rather than predictions, I judge that we are in the “great powers” quadrant indicated in the corresponding chart, with some elements of “assertive nationalism.”

Global realignment: Scenario planning for a world in transition

Source: Capital Group. Scenarios reflect analysis of Capital Group’s Night Watch team as of April 15, 2026, and are not predictive of future outcomes.

The return of a great powers era akin to the 19th century describes a world where the major powers (U.S., China, Russia) expand their power and influence at each other’s expense without instigating a direct military conflict between them. They cultivate relationships among the middle powers (India, Brazil, Middle East, Southeast Asia, etc.) and support proxies in conflict with their rival great powers. The middle and smaller powers hedge between the great powers seeking to benefit from each while trying to avoid the wrath of all. If we had a true geographic sphere of influence order, then the U.S. would focus on the Western Hemisphere. Of course, Iran is distant from the U.S., and that to me is evidence that the U.S. will never be content to simply have a regional sphere of influence. It would like China and Russia to be contained to their neighbourhoods, but it will accept no such constraints for itself even under an America First administration.

The road ahead for at least the next decade will likely be marked by polarization, uncertainty, and a further breakdown in the liberal world order of multilateral institutions that has largely reigned since the end of World War II. Despite these challenges and the likelihood of additional economic and military crises, I believe the great powers firmly seek to avoid catastrophic military conflict directly among themselves. That is a cause for hope that points to the eventual construction of a new world order and a peaceful, stable new normal over time. Although the path between where we are today and where we will arrive will be treacherous at times, I remain optimistic that the U.S. and the world will find their way through this latest geopolitical cycle of change. With its inherent strengths of globally competitive companies and a culture of innovation, the U.S. will retain a prominent leadership role in the world for a long time to come.

One proof point of this conviction is that even while the war in Iran raged, the successful Artemis II mission to the moon became cause for celebration. Even in times of extraordinary geopolitical strain, the U.S. pushed the boundary of human spaceflight the furthest it has gone. This was a healthy and hopeful reminder that periods of great stress can coincide with moments of extraordinary achievement.

Learn more about

Petroyuan is oil transacted in yuan.

Capital controls are government rules that limit how money moves across borders.

Convertibility refers to currency exchange.

Our latest insights

RELATED INSIGHTS

-

Active Management

-

-

Trade

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian investment funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.